You might also like

- Total 42Document1 pageTotal 42Lovely LeninNo ratings yet

- April To July 2019 April To July 2018 Name of State/UTDocument3 pagesApril To July 2019 April To July 2018 Name of State/UTrahulggn4_588180004No ratings yet

- Annual Report English 2018-19-107 PDFDocument1 pageAnnual Report English 2018-19-107 PDFQ C ShamlajiNo ratings yet

- Annual Report English 2018-19-107 PDFDocument1 pageAnnual Report English 2018-19-107 PDFQ C ShamlajiNo ratings yet

- Statistical Information On Rainfed AreaDocument9 pagesStatistical Information On Rainfed AreamkbsbnbjhgjNo ratings yet

- Bio Fertilizer IndiaDocument3 pagesBio Fertilizer IndiaveerabahuNo ratings yet

- 1rice Proc. Last 10 Yrs - 5Document1 page1rice Proc. Last 10 Yrs - 5Rubal ChandraNo ratings yet

- Seizure Report As On 24.05.2019Document2 pagesSeizure Report As On 24.05.2019Niharika ChoudharyNo ratings yet

- Turmeric: Area, Production and Productivity in IndiaDocument1 pageTurmeric: Area, Production and Productivity in IndiaSweta PriyadarshiniNo ratings yet

- Distribution Density of NHDocument1 pageDistribution Density of NHRajaNo ratings yet

- Allocation of Funds (Disb) PageDocument15 pagesAllocation of Funds (Disb) PageShashikant MeenaNo ratings yet

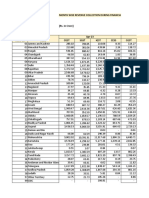

- Month Wise Revenue Collection During Financial Year 2021-2022Document4 pagesMonth Wise Revenue Collection During Financial Year 2021-2022Ali NadafNo ratings yet

- Tax Collection On GST Portal 2019 2020Document16 pagesTax Collection On GST Portal 2019 2020Disha MohantyNo ratings yet

- Millets ProductionDocument2 pagesMillets ProductionSonam RanaNo ratings yet

- Tables Chapter 1Document9 pagesTables Chapter 1Akhilesh KushwahaNo ratings yet

- Aarohan - 3.0Document22 pagesAarohan - 3.0Bddirectorate DoPNo ratings yet

- Tax Collection On GST Portal 2023 2024Document4 pagesTax Collection On GST Portal 2023 2024akhil4every1No ratings yet

- Statement Showing State-Wise Distribution of Net Proceeds of Union Taxes and Duties For Be 2021-22Document1 pageStatement Showing State-Wise Distribution of Net Proceeds of Union Taxes and Duties For Be 2021-22Manish RajNo ratings yet

- Rajya Sabha Unstarred Question No. 2358 Initiatives For Promotion of Renewable Energy SourcesDocument2 pagesRajya Sabha Unstarred Question No. 2358 Initiatives For Promotion of Renewable Energy SourcesdsoNo ratings yet

- Annual Report 2018-19 Chapter-3: 3.1.3.5.2 Establishment of Multipurpose Ai Technicians in Rural India (Maitris)Document2 pagesAnnual Report 2018-19 Chapter-3: 3.1.3.5.2 Establishment of Multipurpose Ai Technicians in Rural India (Maitris)siva kumarNo ratings yet

- State Wise Release & ExpenDocument2 pagesState Wise Release & ExpenLalit Mohan PantNo ratings yet

- Final PPT 2011 - 11Document1 pageFinal PPT 2011 - 11Manojit GhatakNo ratings yet

- Union Tax and DutiesDocument1 pageUnion Tax and DutiesahyaanNo ratings yet

- File 2925Document1 pageFile 2925Saim AnsariNo ratings yet

- GST Collection June 2023Document7 pagesGST Collection June 2023Tech GAMINGNo ratings yet

- GSTR 1 2023 2024Document20 pagesGSTR 1 2023 2024S M SHEKAR AND CONo ratings yet

- Annex 256 AU1117Document3 pagesAnnex 256 AU1117canikhilNo ratings yet

- Annex 4Document1 pageAnnex 4samjaaon1998No ratings yet

- L Sample Survey OrganizationDocument2 pagesL Sample Survey Organizationapi-19729864No ratings yet

- Milk Availability ProductionDocument3 pagesMilk Availability ProductionBala SampathNo ratings yet

- Interregional Fiscal FlowsDocument49 pagesInterregional Fiscal FlowsAishwarya RaoNo ratings yet

- Export Oriented Units in IndiaDocument3 pagesExport Oriented Units in IndiaJot K BajwaNo ratings yet

- Tax Collection On GST Portal 2019 2020Document9 pagesTax Collection On GST Portal 2019 2020Atiq PunjabiNo ratings yet

- Statewise Millet ProductionDocument4 pagesStatewise Millet ProductionHarsh MishraNo ratings yet

- Total Expenditure NHDocument4 pagesTotal Expenditure NHSaikatDebNo ratings yet

- Allocation of Funds (Disbursement)Document1 pageAllocation of Funds (Disbursement)Shashikant MeenaNo ratings yet

- Return SummaryDocument28 pagesReturn SummaryTapan PatelNo ratings yet

- Settlement of IGST To State 2023 2024Document1 pageSettlement of IGST To State 2023 2024akhil4every1No ratings yet

- Transport Systems For Slum Dwellers: Dr. Sewa Ram, Dr. Sanjay Gupta, Bhaskar Gowd Sudagani Spa DelhiDocument45 pagesTransport Systems For Slum Dwellers: Dr. Sewa Ram, Dr. Sanjay Gupta, Bhaskar Gowd Sudagani Spa DelhiShailja SinglaNo ratings yet

- GSTR 3B 2023 2024Document6 pagesGSTR 3B 2023 2024akhil4every1No ratings yet

- UntitledDocument12 pagesUntitledVenkata JayanthNo ratings yet

- Production Estimates of Milk, Egg, Meat and Wool of The Year 2004-05Document10 pagesProduction Estimates of Milk, Egg, Meat and Wool of The Year 2004-05smitasirohiNo ratings yet

- Statement Showing State-Wise Distribution of Net Proceeds of Union Taxes and Duties For Be 2018-19Document1 pageStatement Showing State-Wise Distribution of Net Proceeds of Union Taxes and Duties For Be 2018-19Nivedh VijayakrishnanNo ratings yet

- 3G Auction Results Table 1Document4 pages3G Auction Results Table 1just4u_mangeshNo ratings yet

- Allocation 2018-19 RevisedDocument67 pagesAllocation 2018-19 Revisedmahe pitchaiNo ratings yet

- GSTR 3B 2023 2024Document18 pagesGSTR 3B 2023 2024S M SHEKAR AND CONo ratings yet

- GSTR 1 2022 2023Document32 pagesGSTR 1 2022 2023bsbanjareNo ratings yet

- State-Wise Expenditure On Various Family Planning Activities Under Reproductive and Child Health (RCH) Flexi Pool of National Health Mission (NHM) in India (2018-2019) View Sample Data FormatDocument4 pagesState-Wise Expenditure On Various Family Planning Activities Under Reproductive and Child Health (RCH) Flexi Pool of National Health Mission (NHM) in India (2018-2019) View Sample Data Formatsaurav guptaNo ratings yet

- May 2019 A 1Document1 pageMay 2019 A 1felix florentinoNo ratings yet

- PUC Provisional Consolidated StateWiseDocument2 pagesPUC Provisional Consolidated StateWiseAmogh BhatnagarNo ratings yet

- All Size Classes Sl. No. States/Uts 2010-11 2005-06 % Variation Number Area Number Area Number AreaDocument6 pagesAll Size Classes Sl. No. States/Uts 2010-11 2005-06 % Variation Number Area Number Area Number Arearavi kumarNo ratings yet

- Legy 2 A 1Document13 pagesLegy 2 A 1Shiva PaddamNo ratings yet

- Loksabhaquestions Annex 16 AU2983Document4 pagesLoksabhaquestions Annex 16 AU2983himanshu.mishra.law1No ratings yet

- Current AffairsDocument2 pagesCurrent AffairsSachin TodurNo ratings yet

- Table 5: Statewise Percentage Distribution of Number of Operational Holdings For All Social GroupsDocument2 pagesTable 5: Statewise Percentage Distribution of Number of Operational Holdings For All Social Groupsravi kumarNo ratings yet

- Number of BPL Households 2012Document5 pagesNumber of BPL Households 2012saurav guptaNo ratings yet

- National ParksDocument8 pagesNational Parksmdrifaz98No ratings yet

- GSTR 1 2023 2024Document6 pagesGSTR 1 2023 2024akhil4every1No ratings yet

- RegistrationDocument10 pagesRegistrationDisha MohantyNo ratings yet

- Making Sense of Data II: A Practical Guide to Data Visualization, Advanced Data Mining Methods, and ApplicationsFrom EverandMaking Sense of Data II: A Practical Guide to Data Visualization, Advanced Data Mining Methods, and ApplicationsNo ratings yet

- Cma Synopsis PDFDocument2 pagesCma Synopsis PDFLovely LeninNo ratings yet

- Famly Law Project 23479Document1 pageFamly Law Project 23479Lovely LeninNo ratings yet

- Famly Law Project 23479Document1 pageFamly Law Project 23479Lovely LeninNo ratings yet

- Whether The Office of Governor Is Really Necessary?Document1 pageWhether The Office of Governor Is Really Necessary?Lovely LeninNo ratings yet

- Company Law ProjctDocument17 pagesCompany Law ProjctLovely LeninNo ratings yet

- Labour Law BSWWDocument1 pageLabour Law BSWWLovely LeninNo ratings yet

- Pandian BiggbossDocument1 pagePandian BiggbossLovely LeninNo ratings yet

- HariDocument2 pagesHariLovely LeninNo ratings yet

- Pandian BiggbossDocument1 pagePandian BiggbossLovely LeninNo ratings yet

- Season 4 Can Be Found Below. This Will Be The Fourth Year For Bigg BossDocument1 pageSeason 4 Can Be Found Below. This Will Be The Fourth Year For Bigg BossLovely LeninNo ratings yet

- Taxation bc36765 FinishedDocument1 pageTaxation bc36765 FinishedLovely LeninNo ratings yet

- GunamaniDocument9 pagesGunamaniLovely LeninNo ratings yet

- Aviation Law Project 2347Document2 pagesAviation Law Project 2347Lovely LeninNo ratings yet

- Nts PapuDocument1 pageNts PapuLovely LeninNo ratings yet

- Nts PapuDocument1 pageNts PapuLovely LeninNo ratings yet

- And RemainsDocument1 pageAnd RemainsLovely LeninNo ratings yet

- VvacineDocument1 pageVvacineLovely LeninNo ratings yet

- Antoer PDFDocument1 pageAntoer PDFLovely LeninNo ratings yet

- Course - Cost & Management Accounting: ProblemDocument2 pagesCourse - Cost & Management Accounting: ProblemLovely LeninNo ratings yet

- VRXDocument1 pageVRXLovely LeninNo ratings yet

- Which of The Following Statements About Company Income Taxes Is Most CorrectDocument4 pagesWhich of The Following Statements About Company Income Taxes Is Most CorrectLovely LeninNo ratings yet

- HURFOHRIDocument1 pageHURFOHRILovely LeninNo ratings yet

- SectorDocument1 pageSectorLovely LeninNo ratings yet

- And RemainsDocument1 pageAnd RemainsLovely LeninNo ratings yet

- 66Document1 page66Lovely LeninNo ratings yet

- CHRNVDocument1 pageCHRNVLovely LeninNo ratings yet

- The Board of Studies Cancelled SamtaDocument2 pagesThe Board of Studies Cancelled SamtaLovely LeninNo ratings yet

- Governments Should Make Full Disclosure of ExtraDocument1 pageGovernments Should Make Full Disclosure of ExtraLovely LeninNo ratings yet

- Congratulations PDFDocument10 pagesCongratulations PDFLovely LeninNo ratings yet

- Key Features: A Oke9Wjwm36Onlmr&Redirect Signup A Oke9Wjwm36OnlmrDocument5 pagesKey Features: A Oke9Wjwm36Onlmr&Redirect Signup A Oke9Wjwm36OnlmrVicard GibbingsNo ratings yet

- In Uencing Factors On The Lending Intention of Online Peer-to-Peer LendingDocument33 pagesIn Uencing Factors On The Lending Intention of Online Peer-to-Peer LendinggitaNo ratings yet

- 74841bos60509 cp14Document80 pages74841bos60509 cp14Satish BhorNo ratings yet

- NOTES FOR MARKETING DYNAMICS (All Credits To Pearson Education)Document9 pagesNOTES FOR MARKETING DYNAMICS (All Credits To Pearson Education)Jamie Mariele DiazNo ratings yet

- XYZ Health FoundationDocument7 pagesXYZ Health FoundationAKINREMI AYODEJINo ratings yet

- Chapter - 3 Prospectus & Allotment of SecuritiesDocument15 pagesChapter - 3 Prospectus & Allotment of SecuritiesShoayebNo ratings yet

- Al Kafalah Assignment Ctu 351 PDFDocument16 pagesAl Kafalah Assignment Ctu 351 PDFPiqsamNo ratings yet

- Ia Eco121Document10 pagesIa Eco121Quach Hai My (K17 CT)No ratings yet

- RIPARODocument1 pageRIPAROPEA CHRISTINE AZURIASNo ratings yet

- Illustrative Problem - Share Capital TransactionsDocument12 pagesIllustrative Problem - Share Capital TransactionsJulienne DivadNo ratings yet

- Delivery Hero SE Q2 2019 Presentation VFFFDocument26 pagesDelivery Hero SE Q2 2019 Presentation VFFFGiang NguyenNo ratings yet

- FNSACC513 Rattanawadee PholsanDocument29 pagesFNSACC513 Rattanawadee PholsanChaleamkwan NatungkhumNo ratings yet

- EJMCM Volume 8 Issue 3 Pages 3129-3136Document8 pagesEJMCM Volume 8 Issue 3 Pages 3129-3136shanmithaNo ratings yet

- CMT Tutorial Level 2Document114 pagesCMT Tutorial Level 2stuartb4u100% (2)

- Aptitude Part ThreeDocument3 pagesAptitude Part ThreeAddisu Zeleke100% (1)

- 2000 Oxfam Tax Havens Releasing Hidden Billions To Poverty EradicationDocument26 pages2000 Oxfam Tax Havens Releasing Hidden Billions To Poverty EradicationJuan Enrique ValerdiNo ratings yet

- Audit of Shareholders' Equity - July 22, 2021Document35 pagesAudit of Shareholders' Equity - July 22, 2021Kathrina RoxasNo ratings yet

- Chapter 1 Concept of Entrepreneurship - Meaning, Elements, EDDocument23 pagesChapter 1 Concept of Entrepreneurship - Meaning, Elements, EDPrincess Galicia Tres ReyesNo ratings yet

- 1 Nature of Sport MarketingDocument28 pages1 Nature of Sport MarketingSuhel KararaNo ratings yet

- Indian Public Finance Statistics 2017-18Document101 pagesIndian Public Finance Statistics 2017-18Priyansh ShrivastavNo ratings yet

- ADD MATHS Project 2018 Index NumberDocument25 pagesADD MATHS Project 2018 Index NumberLoh Chee WeiNo ratings yet

- Vanning ReportDocument4 pagesVanning ReportAhmadmasrokanNo ratings yet

- ReplacedDocument4 pagesReplacedLuno coin100% (1)

- Ghana Investment Promotion Centre (Gipc) Act 865Document19 pagesGhana Investment Promotion Centre (Gipc) Act 865JeffreyNo ratings yet

- Name: DEC. 17, 2020 Buscom ScoreDocument4 pagesName: DEC. 17, 2020 Buscom ScoreErica DaprosaNo ratings yet

- Lec 1 2 3 International AccDocument38 pagesLec 1 2 3 International AccMariam AbdelalimNo ratings yet

- Bicycle Inventory Product Category Product Name Purchase Cost Selling PriceDocument2 pagesBicycle Inventory Product Category Product Name Purchase Cost Selling PriceKaran RawatNo ratings yet

- Diokno vs. Rehabilitation Finance Corp.Document1 pageDiokno vs. Rehabilitation Finance Corp.Romela B. ParamiNo ratings yet

- Preliminary PagesDocument328 pagesPreliminary PagesCyber VirginNo ratings yet

- Fort St. John - RCMP Building Construction Letters of IntentDocument9 pagesFort St. John - RCMP Building Construction Letters of IntentAlaskaHighwayNewsNo ratings yet