You might also like

- National Interest Waiver Software EngineerDocument15 pagesNational Interest Waiver Software EngineerFaha JavedNo ratings yet

- Kieso10eChp09 MidtermDocument30 pagesKieso10eChp09 MidtermJohn FinneyNo ratings yet

- Marking Scheme For Term 2 Trial Exam, STPM 2019 (Gbs Melaka) Section A (45 Marks)Document7 pagesMarking Scheme For Term 2 Trial Exam, STPM 2019 (Gbs Melaka) Section A (45 Marks)Michelles JimNo ratings yet

- E7d61 139.new Directions in Race Ethnicity and CrimeDocument208 pagesE7d61 139.new Directions in Race Ethnicity and CrimeFlia Rincon Garcia SoyGabyNo ratings yet

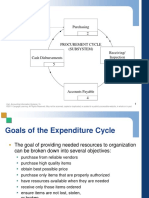

- Expenditure Cycle Part 1 - Purchases and Cash DisbDocument33 pagesExpenditure Cycle Part 1 - Purchases and Cash DisbgoeswidsNo ratings yet

- The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument38 pagesThe Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresontykerlsNo ratings yet

- The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument38 pagesThe Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresontykerlsNo ratings yet

- CH 2Document54 pagesCH 2ali alhussainNo ratings yet

- JAMES-AIS - Slides, Ch1, 7e.1Document62 pagesJAMES-AIS - Slides, Ch1, 7e.1Damien LeeNo ratings yet

- AIS Hall Chapter 1Document55 pagesAIS Hall Chapter 1walsondevNo ratings yet

- The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument41 pagesThe Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresFathan MubinaNo ratings yet

- The Information System: An Accountant's Perspective: Accounting Information Systems, 8eDocument33 pagesThe Information System: An Accountant's Perspective: Accounting Information Systems, 8eAini JannahNo ratings yet

- Chapter 1 The Information System: An Accountant's PerspectiveDocument41 pagesChapter 1 The Information System: An Accountant's PerspectiveDhanylane Phole Librea SeraficaNo ratings yet

- Chapter 1Document47 pagesChapter 1TERRIUS AceNo ratings yet

- CH 05Document27 pagesCH 05Zac VanessaNo ratings yet

- Chapter 5Document41 pagesChapter 5TERRIUS AceNo ratings yet

- The Revenue Cycle: Introduction To Accounting Information Systems, 7eDocument47 pagesThe Revenue Cycle: Introduction To Accounting Information Systems, 7eontykerlsNo ratings yet

- Financial Reporting and Management Reporting Systems: Introduction To Accounting Information Systems, 7eDocument14 pagesFinancial Reporting and Management Reporting Systems: Introduction To Accounting Information Systems, 7eontykerlsNo ratings yet

- Chapter One An Accounting PerspectiveDocument41 pagesChapter One An Accounting PerspectiveEka Septiana AnisaNo ratings yet

- IT Controls Part III: Systems Development, Program Changes, and Application ControlsDocument41 pagesIT Controls Part III: Systems Development, Program Changes, and Application Controlsich ichNo ratings yet

- The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument26 pagesThe Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresJNo ratings yet

- 14 Construct Deliver and Maintain Systems ProjectsDocument53 pages14 Construct Deliver and Maintain Systems Projectscrissille100% (1)

- Hall - AIS 7e PP - ch15Document47 pagesHall - AIS 7e PP - ch15ontykerlsNo ratings yet

- Chapter 3 Ethics, Fraud and Internal ControlDocument44 pagesChapter 3 Ethics, Fraud and Internal ControlFarah ByunNo ratings yet

- Chapter 2 Transaction ProcessingDocument27 pagesChapter 2 Transaction ProcessingABStract001100% (1)

- CHAP1 - Overview of AuditDocument79 pagesCHAP1 - Overview of AuditZen OnaNo ratings yet

- IT Controls Part II: Security and Access: Accounting Information Systems, 7eDocument41 pagesIT Controls Part II: Security and Access: Accounting Information Systems, 7eEllie YsonNo ratings yet

- The Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresDocument33 pagesThe Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresontykerlsNo ratings yet

- Construct, Deliver and Maintain Systems Projects WfaDocument53 pagesConstruct, Deliver and Maintain Systems Projects WfaRiviera MehsNo ratings yet

- The Conversion Cycle: Introduction To Accounting Information Systems, 7eDocument44 pagesThe Conversion Cycle: Introduction To Accounting Information Systems, 7eontykerlsNo ratings yet

- Ethics, Fraud, and Internal Control: Introduction To Accounting Information Systems, 7eDocument57 pagesEthics, Fraud, and Internal Control: Introduction To Accounting Information Systems, 7eAsh imoNo ratings yet

- Lesson 6 Handout PDFDocument21 pagesLesson 6 Handout PDFKurt OrfanelNo ratings yet

- The Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresDocument27 pagesThe Expenditure Cycle Part II: Payroll Processing and Fixed Asset Procedureshassan nassereddineNo ratings yet

- The Revenue Cycle: James A. HallDocument91 pagesThe Revenue Cycle: James A. HallAira Rhialyn MangubatNo ratings yet

- Ethics, Fraud, and Internal Control: Accounting Information Systems, 7eDocument44 pagesEthics, Fraud, and Internal Control: Accounting Information Systems, 7eZac VanessaNo ratings yet

- The Revenue Cycle: Introduction To Accounting Information Systems, 8eDocument30 pagesThe Revenue Cycle: Introduction To Accounting Information Systems, 8ehassan nassereddineNo ratings yet

- Chapter 3 Ethics, Fraud, and Internal Control: Accounting Information Systems, 7eDocument44 pagesChapter 3 Ethics, Fraud, and Internal Control: Accounting Information Systems, 7eDhanylane Phole Librea SeraficaNo ratings yet

- Lesson 1 Handout PDFDocument14 pagesLesson 1 Handout PDFKurt OrfanelNo ratings yet

- Enterprise Resource Planning Systems: Accounting Information Systems, 7eDocument32 pagesEnterprise Resource Planning Systems: Accounting Information Systems, 7eCholifah Husti LailaNo ratings yet

- Auditing in Computer Environment System, Chapter 5 by James HallDocument44 pagesAuditing in Computer Environment System, Chapter 5 by James HallRobert Castillo0% (1)

- CIS REVIEWER Chapter 7 and 8Document94 pagesCIS REVIEWER Chapter 7 and 8Lalaine De JesusNo ratings yet

- Managing The Systems Development Life Cycle: Accounting Information Systems, 7eDocument45 pagesManaging The Systems Development Life Cycle: Accounting Information Systems, 7eMA LimboNo ratings yet

- Hall Asia Edition PP - ch01Document41 pagesHall Asia Edition PP - ch01Vince Paolo Alicaya AcidoNo ratings yet

- The Revenue Cycle: Accounting Information Systems, 7eDocument40 pagesThe Revenue Cycle: Accounting Information Systems, 7esandhyaNo ratings yet

- BIS309 Lecture 1 - The Information System An Accountant's PerspectiveDocument21 pagesBIS309 Lecture 1 - The Information System An Accountant's PerspectiveCOLLET GAOLEBENo ratings yet

- The Conversion Cycle: Introduction To Accounting Information Systems, 8eDocument51 pagesThe Conversion Cycle: Introduction To Accounting Information Systems, 8eDea Gheby YolandaNo ratings yet

- Lesson 3 Handout PDFDocument16 pagesLesson 3 Handout PDFKurt OrfanelNo ratings yet

- Daft 11 OtDocument23 pagesDaft 11 OtHasan Gürkan BozkırNo ratings yet

- Lesson 5 HandoutDocument20 pagesLesson 5 HandoutIan De DiosNo ratings yet

- Chapter 13 - Data WarehouseDocument46 pagesChapter 13 - Data WarehouseAida GdNo ratings yet

- Information and Control ProcessesDocument38 pagesInformation and Control ProcessesFun Toosh345No ratings yet

- The Conversion Cycle: Principles of Accounting Information Systems, Asia EditionDocument43 pagesThe Conversion Cycle: Principles of Accounting Information Systems, Asia EditionCelestia StevenNo ratings yet

- 1 The Is An Accountants Perspective (Pertemuan I) James HallDocument33 pages1 The Is An Accountants Perspective (Pertemuan I) James HallAgandri Sar Marsahala Sihaloho0% (1)

- The Conversion Cycle: Principles of Accounting Information Systems, Asia EditionDocument31 pagesThe Conversion Cycle: Principles of Accounting Information Systems, Asia EditionKurt OrfanelNo ratings yet

- Accounting Information Systems - Hall - 9edDocument419 pagesAccounting Information Systems - Hall - 9edapple treeNo ratings yet

- The Information System: An Accountant's Perspective: Accounting Information Systems 9e James A. HallDocument29 pagesThe Information System: An Accountant's Perspective: Accounting Information Systems 9e James A. HallshierylNo ratings yet

- Chapter 5 Worsheet 2Document89 pagesChapter 5 Worsheet 2kakaoNo ratings yet

- PP 15 NewDocument49 pagesPP 15 NewStevan PknNo ratings yet

- The Revenue Cycle: Accounting Information Systems, 7eDocument46 pagesThe Revenue Cycle: Accounting Information Systems, 7ekevin nagacNo ratings yet

- Everything you want to know about Agile: How to get Agile results in a less-than-agile organizationFrom EverandEverything you want to know about Agile: How to get Agile results in a less-than-agile organizationRating: 3.5 out of 5 stars3.5/5 (4)

- Cloud Computing: The Untold Origins of Cloud Computing (Manipulation, Configuring and Accessing the Applications Online)From EverandCloud Computing: The Untold Origins of Cloud Computing (Manipulation, Configuring and Accessing the Applications Online)No ratings yet

- Kinney 9e Im CH 04Document17 pagesKinney 9e Im CH 04DIGNA HERNANDEZNo ratings yet

- D. All of The Above Are True.: AMIS 3300 Pop Quiz - Chapter 17Document5 pagesD. All of The Above Are True.: AMIS 3300 Pop Quiz - Chapter 17DIGNA HERNANDEZNo ratings yet

- Poems and Correspondence PDFDocument44 pagesPoems and Correspondence PDFDIGNA HERNANDEZNo ratings yet

- Heacock vs. NLUDocument4 pagesHeacock vs. NLUDIGNA HERNANDEZNo ratings yet

- PECO vs. CIRDocument3 pagesPECO vs. CIRDIGNA HERNANDEZNo ratings yet

- Data SheetDocument56 pagesData SheetfaycelNo ratings yet

- My BaboogDocument1 pageMy BaboogMaral Habeshian VieiraNo ratings yet

- Functions of Theory in ResearchDocument2 pagesFunctions of Theory in ResearchJomariMolejonNo ratings yet

- English For Academic and Professional Purposes - ExamDocument3 pagesEnglish For Academic and Professional Purposes - ExamEddie Padilla LugoNo ratings yet

- Construction Project - Life Cycle PhasesDocument4 pagesConstruction Project - Life Cycle Phasesaymanmomani2111No ratings yet

- Topic: Grammatical Issues: What Are Parts of Speech?Document122 pagesTopic: Grammatical Issues: What Are Parts of Speech?AK AKASHNo ratings yet

- The Bio-Based Economy in The NetherlandsDocument12 pagesThe Bio-Based Economy in The NetherlandsIrving Toloache FloresNo ratings yet

- Electronic Diversity Visa ProgrambDocument1 pageElectronic Diversity Visa Programbsamkimari5No ratings yet

- Transfert de Chaleur AngDocument10 pagesTransfert de Chaleur Angsouhir gritliNo ratings yet

- Tribes Without RulersDocument25 pagesTribes Without Rulersgulistan.alpaslan8134100% (1)

- Governance Operating Model: Structure Oversight Responsibilities Talent and Culture Infrastructu REDocument6 pagesGovernance Operating Model: Structure Oversight Responsibilities Talent and Culture Infrastructu REBob SolísNo ratings yet

- Service Quality Dimensions of A Philippine State UDocument10 pagesService Quality Dimensions of A Philippine State UVilma SottoNo ratings yet

- Chapter 2 Short-Term SchedulingDocument49 pagesChapter 2 Short-Term SchedulingBOUAZIZ LINANo ratings yet

- SievesDocument3 pagesSievesVann AnthonyNo ratings yet

- Agma MachineDocument6 pagesAgma Machinemurali036No ratings yet

- TM Mic Opmaint EngDocument186 pagesTM Mic Opmaint Engkisedi2001100% (2)

- Industrial ReportDocument52 pagesIndustrial ReportSiddharthNo ratings yet

- IJRHAL - Exploring The Journey of Steel Authority of India (SAIL) As A Maharatna CompanyDocument12 pagesIJRHAL - Exploring The Journey of Steel Authority of India (SAIL) As A Maharatna CompanyImpact JournalsNo ratings yet

- Understanding The Contribution of HRM Bundles For Employee Outcomes Across The Life-SpanDocument15 pagesUnderstanding The Contribution of HRM Bundles For Employee Outcomes Across The Life-SpanPhuong NgoNo ratings yet

- CIPD L5 EML LOL Wk3 v1.1Document19 pagesCIPD L5 EML LOL Wk3 v1.1JulianNo ratings yet

- BSS Troubleshooting Manual PDFDocument220 pagesBSS Troubleshooting Manual PDFleonardomarinNo ratings yet

- CE162P MODULE 2 LECTURE 4 Analysis & Design of Mat FoundationDocument32 pagesCE162P MODULE 2 LECTURE 4 Analysis & Design of Mat FoundationPROSPEROUS LUCKILYNo ratings yet

- Resume - James MathewsDocument2 pagesResume - James Mathewsapi-610738092No ratings yet

- Topic One ProcurementDocument35 pagesTopic One ProcurementSaid Sabri KibwanaNo ratings yet

- JO 20221109 NationalDocument244 pagesJO 20221109 NationalMark Leo BejeminoNo ratings yet

- Categorical SyllogismDocument3 pagesCategorical SyllogismYan Lean DollisonNo ratings yet

- Approvals Management Responsibilities and Setups in AME.B PDFDocument20 pagesApprovals Management Responsibilities and Setups in AME.B PDFAli LoganNo ratings yet