You might also like

- Cash Flow StatementDocument23 pagesCash Flow StatementJayci LeiNo ratings yet

- Installment Sales ReviewerDocument5 pagesInstallment Sales ReviewerJymldy EnclnNo ratings yet

- Accounting 2Document3 pagesAccounting 2cherryannNo ratings yet

- Statement of Cash FlowsDocument16 pagesStatement of Cash FlowsBrian Reyes GangcaNo ratings yet

- Chapter 13Document9 pagesChapter 13RBNo ratings yet

- May 2016 c1 RegularDocument10 pagesMay 2016 c1 RegularKenneth Bryan Tegerero TegioNo ratings yet

- ACP - Quiz-On-Cash-Flow - For-PostingDocument3 pagesACP - Quiz-On-Cash-Flow - For-PostingJunel PlanosNo ratings yet

- MIDTERM ReviewerDocument12 pagesMIDTERM ReviewerKathrina RoxasNo ratings yet

- Acctg4a 02042017 Exam Quiz1aDocument5 pagesAcctg4a 02042017 Exam Quiz1aPatOcampoNo ratings yet

- FINALS Cash FlowDocument4 pagesFINALS Cash FlowLucille Gacutan AramburoNo ratings yet

- ACCT 101 QUIZ 11 Section ReviewDocument5 pagesACCT 101 QUIZ 11 Section ReviewhappystoneNo ratings yet

- Review Problems AnswersDocument4 pagesReview Problems AnswersFranchette Yvonne JulianNo ratings yet

- Merchandise Business Class PerformanceDocument5 pagesMerchandise Business Class PerformanceGrace GamillaNo ratings yet

- Accy 517 HW PB Set 1Document30 pagesAccy 517 HW PB Set 1YonghoChoNo ratings yet

- Zamboanga net income accrual basisDocument5 pagesZamboanga net income accrual basisBabylyn NavarroNo ratings yet

- Cashflow AssignmentDocument4 pagesCashflow AssignmentSrujana GantaNo ratings yet

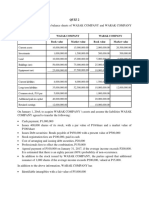

- Wasak and Warak balance sheets acquisition quizDocument3 pagesWasak and Warak balance sheets acquisition quiznaddieNo ratings yet

- Quiz 2 Statement of Comprehensive Income Cash Vs Accrual BasisDocument11 pagesQuiz 2 Statement of Comprehensive Income Cash Vs Accrual BasisHaidee Flavier SabidoNo ratings yet

- AdvaccDocument3 pagesAdvaccAlyssa CamposNo ratings yet

- Advanced Accounting Drill ProblemsDocument6 pagesAdvanced Accounting Drill ProblemsiajycNo ratings yet

- Installment SalesDocument4 pagesInstallment SaleskathNo ratings yet

- Merchandising ConcernDocument27 pagesMerchandising ConcernCATUGAL, LANCE ALECNo ratings yet

- Accounting For Business CombinationDocument17 pagesAccounting For Business CombinationTrace ReyesNo ratings yet

- Cash Flow Statement PreparationDocument6 pagesCash Flow Statement PreparationKrystal Guile DagatanNo ratings yet

- Understanding the Statement of Cash FlowsDocument26 pagesUnderstanding the Statement of Cash FlowsSouvik DeNo ratings yet

- Cash flow statement problemsDocument12 pagesCash flow statement problemsAnjali Mehta100% (1)

- Cash to Accrual ConversionDocument24 pagesCash to Accrual ConversionSteffany RoqueNo ratings yet

- Financial Accounting ProjectDocument9 pagesFinancial Accounting ProjectL.a. LadoresNo ratings yet

- MCQs Problems For Merchandising Business - For UploadDocument8 pagesMCQs Problems For Merchandising Business - For UploadIrish Trisha PerezNo ratings yet

- Accounting Cycle of A Merchandising Business Part 2Document7 pagesAccounting Cycle of A Merchandising Business Part 2Amie Jane MirandaNo ratings yet

- CFS Exercises 1Document4 pagesCFS Exercises 1richkeaneNo ratings yet

- CH 16 Practice SolutionsDocument9 pagesCH 16 Practice SolutionsaaaNo ratings yet

- Topic 2 - Af09101 - Financial StatementsDocument42 pagesTopic 2 - Af09101 - Financial Statementsarusha afroNo ratings yet

- Practical Accounting 1Document11 pagesPractical Accounting 1Jomar VillenaNo ratings yet

- 01.correction of Errors - 245038322 PDFDocument4 pages01.correction of Errors - 245038322 PDFMaan CabolesNo ratings yet

- Cash and Accrual BasisDocument24 pagesCash and Accrual BasisAlexa LeeNo ratings yet

- Father Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #4)Document10 pagesFather Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #4)marygraceomacNo ratings yet

- ACCTG-206B-FIRST-PREBOARD Without AnswerDocument16 pagesACCTG-206B-FIRST-PREBOARD Without AnswerRheu ReyesNo ratings yet

- Cash To Accrual ProblemsDocument10 pagesCash To Accrual ProblemsAmethystNo ratings yet

- This Is RealDocument17 pagesThis Is RealCheemee LiuNo ratings yet

- Icandocumentsnovemebr 2017 Pathfinder Skills PDFDocument179 pagesIcandocumentsnovemebr 2017 Pathfinder Skills PDFDaniel AdegboyeNo ratings yet

- 1Document13 pages1DesireeNo ratings yet

- Far 101 - Financial Accounting Process PDFDocument4 pagesFar 101 - Financial Accounting Process PDFReyn Saplad Perales100% (1)

- TASK SHEET 9.3. WPS OfficeDocument10 pagesTASK SHEET 9.3. WPS OfficeHanaNo ratings yet

- Finman 108 (Quiz 4) ...Document6 pagesFinman 108 (Quiz 4) ...CHARRYSAH TABAOSARESNo ratings yet

- This Is RealDocument17 pagesThis Is RealCheemee LiuNo ratings yet

- This Is RealDocument17 pagesThis Is RealCheemee LiuNo ratings yet

- Statement of Cash Flows: Like An Income StatementDocument27 pagesStatement of Cash Flows: Like An Income StatementbecalmNo ratings yet

- Holding Co. QuestionsDocument77 pagesHolding Co. Questionsअक्षय गोयलNo ratings yet

- A1 Installment SalesDocument3 pagesA1 Installment SalesMae0% (1)

- Act FinalDocument6 pagesAct Finalabu.sakibNo ratings yet

- Working CapitalDocument61 pagesWorking CapitalSharmistha Banerjee100% (1)

- Homework On Statement of Cash FlowsDocument2 pagesHomework On Statement of Cash FlowsAmy SpencerNo ratings yet

- Abm WK6 ActDocument1 pageAbm WK6 ActRovic TipanNo ratings yet

- Taxation-Company Tax and VatDocument3 pagesTaxation-Company Tax and VatGARUIS MELINo ratings yet

- ACCT ProblemsDocument3 pagesACCT ProblemsNanya BisnestNo ratings yet

- Compare Direct and Indirect Cash Flow MethodsDocument8 pagesCompare Direct and Indirect Cash Flow MethodsKhayNo ratings yet

- Financial Accounting P 1 Quiz 3 KeyDocument6 pagesFinancial Accounting P 1 Quiz 3 KeyJei CincoNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- Case Study The Mechanical Engineer Turned Abattoir OwnerDocument8 pagesCase Study The Mechanical Engineer Turned Abattoir OwnerJb De GuzmanNo ratings yet

- Sales Type Lease (Lessor's Books)Document1 pageSales Type Lease (Lessor's Books)Jb De GuzmanNo ratings yet

- Earnings Per ShareDocument10 pagesEarnings Per ShareJb De GuzmanNo ratings yet

- Sales Leaseback (Lessor)Document3 pagesSales Leaseback (Lessor)Jb De GuzmanNo ratings yet

- Direct Finance Lease (Lessor's Books)Document1 pageDirect Finance Lease (Lessor's Books)Jb De GuzmanNo ratings yet

- Direct Finance Lease (Lessor's Books)Document1 pageDirect Finance Lease (Lessor's Books)Jb De GuzmanNo ratings yet

- Accounting For AppropriationDocument1 pageAccounting For AppropriationJb De GuzmanNo ratings yet

- Appropriation of Retained Earnings: Voluntary Appropriation Is A Matter of Discretion On The Part of Management. ThisDocument2 pagesAppropriation of Retained Earnings: Voluntary Appropriation Is A Matter of Discretion On The Part of Management. ThisJb De GuzmanNo ratings yet

- Accounting For Defined Benefit PlanDocument2 pagesAccounting For Defined Benefit PlanJb De GuzmanNo ratings yet

- Accounting For Defined Contribution PlanDocument1 pageAccounting For Defined Contribution PlanJb De GuzmanNo ratings yet

- Customer Satisfaction Towards Investing Chits in KsfeDocument41 pagesCustomer Satisfaction Towards Investing Chits in Ksfehariprasad kuloorNo ratings yet

- Personal Details: Customer Information RecordDocument2 pagesPersonal Details: Customer Information RecordLeslie Ann Cabasi TenioNo ratings yet

- Approved Guidelines On Operations of Electronic Payment Channels in NigeriaDocument48 pagesApproved Guidelines On Operations of Electronic Payment Channels in NigeriaBrute1989No ratings yet

- INTERMEDIATE ACCOUNTING-Unit02Document38 pagesINTERMEDIATE ACCOUNTING-Unit02Rattanaporn TechaprapasratNo ratings yet

- RTP Gr1 Nov2022Document129 pagesRTP Gr1 Nov2022bakchodikarnekliyeNo ratings yet

- Conceptual Framework: Dr. Nafis Rahman Intermediate Accounting 1 Spring 2020Document39 pagesConceptual Framework: Dr. Nafis Rahman Intermediate Accounting 1 Spring 2020Cheuk Ying NicoleNo ratings yet

- Sr No Roll No Topic Name Financial TopicsDocument2 pagesSr No Roll No Topic Name Financial Topicssharique khan53% (19)

- Romanian bank codes and SWIFT codesDocument1 pageRomanian bank codes and SWIFT codesflorin74No ratings yet

- M&T Residences - Income & Expence Document DHT ZNDocument2 pagesM&T Residences - Income & Expence Document DHT ZNZuko NdodanaNo ratings yet

- Financial Statements and Ratio AnalysisDocument2 pagesFinancial Statements and Ratio AnalysisRyan MiguelNo ratings yet

- PM Quiz 4Document3 pagesPM Quiz 4Daniyal NasirNo ratings yet

- Roi AnalysisDocument13 pagesRoi AnalysisManuel ValleNo ratings yet

- A Comparative Study of Mutual Fund Schemes of State Bank of India and Unit Trust of IndiaDocument9 pagesA Comparative Study of Mutual Fund Schemes of State Bank of India and Unit Trust of IndiaAman WadhwaNo ratings yet

- Sanchay Maximizer.Document2 pagesSanchay Maximizer.AvinashNo ratings yet

- Ateneo de Zamboanga University Advanced Accounting FINAL EXAMINATION solutionsDocument7 pagesAteneo de Zamboanga University Advanced Accounting FINAL EXAMINATION solutionsRIZLE SOGRADIELNo ratings yet

- Aparna CYBERHEIGHTSDocument1 pageAparna CYBERHEIGHTSKamlesh UGNo ratings yet

- 2021 Kiva Report PROOF - The Company LabDocument9 pages2021 Kiva Report PROOF - The Company LabChloeNo ratings yet

- ACC111 Final ExamDocument10 pagesACC111 Final ExamGayle Montecillo Pantonial OndoyNo ratings yet

- Research Title: Simple MortgageDocument9 pagesResearch Title: Simple MortgageAnand SinghNo ratings yet

- Intermediate Accounting 2 Second Grading Examination: Name: Date: Professor: Section: ScoreDocument25 pagesIntermediate Accounting 2 Second Grading Examination: Name: Date: Professor: Section: ScoreNah Hamza100% (1)

- APPS Rating and ReviewsDocument83 pagesAPPS Rating and ReviewsApurbh Singh KashyapNo ratings yet

- 3.bank Reconciliation Statement by NavkarDocument10 pages3.bank Reconciliation Statement by Navkarwnabi20No ratings yet

- EC - MODULE 3-NBFC - PPT - Procedure NBFCDocument10 pagesEC - MODULE 3-NBFC - PPT - Procedure NBFCAnanya ChaudharyNo ratings yet

- Advanced Accounting - Dayag 2015 - Chapter 15 - Multiple Choice Solution (14-18)Document1 pageAdvanced Accounting - Dayag 2015 - Chapter 15 - Multiple Choice Solution (14-18)John Carlos DoringoNo ratings yet

- 08 Bank of America vs. CADocument2 pages08 Bank of America vs. CALouise Bolivar DadivasNo ratings yet

- Banking Awareness Hand Book by Er. G C Nayak PDFDocument86 pagesBanking Awareness Hand Book by Er. G C Nayak PDFhames75% (4)

- PDFFile5b2780d4bf42a8 02107843Document338 pagesPDFFile5b2780d4bf42a8 02107843Vinit MNo ratings yet

- Call Centre Manual 04052007Document27 pagesCall Centre Manual 04052007shaharhr1No ratings yet

- Jethro S. Cortado BSA 1B Goverment Grants and BorrowingDocument5 pagesJethro S. Cortado BSA 1B Goverment Grants and BorrowingJi Eun VinceNo ratings yet

- The Ultimate Accountants Reference 3rd Edition - 2012 - Bragg - The Chart of AccountsDocument6 pagesThe Ultimate Accountants Reference 3rd Edition - 2012 - Bragg - The Chart of AccountsSamer SayedNo ratings yet