You might also like

- Investments (2023) 1 (01 50)Document50 pagesInvestments (2023) 1 (01 50)farzad naderi50% (6)

- FIM Anthony CH End Solution PDFDocument287 pagesFIM Anthony CH End Solution PDFMosarraf Rased50% (6)

- General Banking Law - Quizzer With AnswersDocument9 pagesGeneral Banking Law - Quizzer With AnswersJust ForNo ratings yet

- Merit Enterprise Corp Case StudyDocument2 pagesMerit Enterprise Corp Case StudyQistina80% (5)

- What Is A Financial Intermediary (Final)Document6 pagesWhat Is A Financial Intermediary (Final)Mark PlancaNo ratings yet

- Financial IntermediaryDocument10 pagesFinancial Intermediaryalajar opticalNo ratings yet

- Functions of Financial IntermediariesDocument3 pagesFunctions of Financial IntermediariesErin SuryandariNo ratings yet

- Untitled 1Document3 pagesUntitled 1cesar_mayonte_montaNo ratings yet

- Introduction To Financial IntermediationDocument10 pagesIntroduction To Financial IntermediationbugmenomoreNo ratings yet

- CFI 321 Lesson 3 June 2023Document3 pagesCFI 321 Lesson 3 June 2023nyambura jacklineNo ratings yet

- FIN24 Financial Markets OverviewDocument4 pagesFIN24 Financial Markets Overview臆倩No ratings yet

- Without Financial InstitutionsDocument2 pagesWithout Financial InstitutionsLevi Emmanuel Veloso BravoNo ratings yet

- Finalcil Market - Bba Unit One &twoDocument79 pagesFinalcil Market - Bba Unit One &twoBhagawat PaudelNo ratings yet

- Financial Intermediaries: Financial Institution Bank Bank Deposits Loans Assets LiabilitiesDocument3 pagesFinancial Intermediaries: Financial Institution Bank Bank Deposits Loans Assets LiabilitiesRishikaysh KaakandikarNo ratings yet

- Financial Markets: Jamille P. Icalina, BSA - 3Document3 pagesFinancial Markets: Jamille P. Icalina, BSA - 3Alex LevithanNo ratings yet

- Financial IntermediationDocument20 pagesFinancial IntermediationFrances Bea Waguis100% (1)

- Selected Tutorial Solutions - Week 2 IntroDocument4 pagesSelected Tutorial Solutions - Week 2 IntroPhuong NguyenNo ratings yet

- Why Are Financial Intermediaries SpecialDocument10 pagesWhy Are Financial Intermediaries SpecialSamra AfzalNo ratings yet

- Financial Intermediaries Transform AssetsDocument3 pagesFinancial Intermediaries Transform AssetsSheanne GuerreroNo ratings yet

- FIN 2024 Overview of the Financial SystemsDocument4 pagesFIN 2024 Overview of the Financial SystemsBee LNo ratings yet

- Financial Intermediaries' Evolving RolesDocument5 pagesFinancial Intermediaries' Evolving RolesSmriti KhannaNo ratings yet

- How financial services help channel fundsDocument2 pagesHow financial services help channel fundsAtul SinghNo ratings yet

- Why Financial Markets MatterDocument26 pagesWhy Financial Markets Mattergeraldine biasongNo ratings yet

- Chapter 2Document11 pagesChapter 2desktopmarsNo ratings yet

- Chapter 2 Financial Intermediaries and Other ParticipantsDocument45 pagesChapter 2 Financial Intermediaries and Other ParticipantsWill De OcampoNo ratings yet

- Saint Mary's University Faculty of Accounting and Finance Financial Market and Institution Assignment OneDocument10 pagesSaint Mary's University Faculty of Accounting and Finance Financial Market and Institution Assignment OneruhamaNo ratings yet

- SAINT MARY’S UNIVERSITY Faculty of Accounting and finance Financial market and institution assignment oneDocument10 pagesSAINT MARY’S UNIVERSITY Faculty of Accounting and finance Financial market and institution assignment oneruhamaNo ratings yet

- Financial MarketDocument8 pagesFinancial MarketDesiree Manaytay100% (1)

- Saunders & Cornnet Solution Chapter 1 Part 1Document5 pagesSaunders & Cornnet Solution Chapter 1 Part 1Mo AlamNo ratings yet

- Bab 1 FRMDocument11 pagesBab 1 FRMartaninditaNo ratings yet

- Depository & Non Depository: Financial IntermediaryDocument136 pagesDepository & Non Depository: Financial IntermediaryMoud KhalfaniNo ratings yet

- Finmar - Chapter 12 - 14Document24 pagesFinmar - Chapter 12 - 14AlexanNo ratings yet

- The Nature of Financial Intermediation: International BankingDocument24 pagesThe Nature of Financial Intermediation: International BankingToàn VănNo ratings yet

- Lesson 1,2,3 - FinmarDocument10 pagesLesson 1,2,3 - FinmarDesiree ManaytayNo ratings yet

- Chapter-2 (Saleh Sir)Document24 pagesChapter-2 (Saleh Sir)MD Rakib MiaNo ratings yet

- Function of Financial Intermediaries PDFDocument29 pagesFunction of Financial Intermediaries PDFOliwaOrdanezaNo ratings yet

- Web Lesson1Document4 pagesWeb Lesson1api-3733468No ratings yet

- Financial Environments Specifically Institutions: Ronil John GarganianDocument11 pagesFinancial Environments Specifically Institutions: Ronil John GarganianSandra LangNo ratings yet

- Capital Markets Overview and ParticipantsDocument52 pagesCapital Markets Overview and ParticipantsChintan JoshiNo ratings yet

- COMPARATIVE BANKING AND FINANCIAL SYSTEMSDocument18 pagesCOMPARATIVE BANKING AND FINANCIAL SYSTEMSibukun akinleye100% (3)

- ACCO 20083: FINANCIAL MARKETS - FINANCIAL INTERMEDIARIES AND OTHER PARTICIPANTSDocument58 pagesACCO 20083: FINANCIAL MARKETS - FINANCIAL INTERMEDIARIES AND OTHER PARTICIPANTSKent CabreraNo ratings yet

- FINANCIAL MARKETS AND INSTITUTIONS - notesDocument32 pagesFINANCIAL MARKETS AND INSTITUTIONS - notessreginatoNo ratings yet

- Finance (Pronounced /fɪ Nænts/ or / Faɪnænts/) Is The Science ofDocument50 pagesFinance (Pronounced /fɪ Nænts/ or / Faɪnænts/) Is The Science ofSonal JainNo ratings yet

- Ayala Commercial BankingDocument8 pagesAyala Commercial BankingFrench D. AyalaNo ratings yet

- Role of Financial Intermediaries in The 21st CenturyDocument36 pagesRole of Financial Intermediaries in The 21st Centuryaman_dia50% (2)

- Role of Financial Institutions in Facilitating Resource AllocationDocument5 pagesRole of Financial Institutions in Facilitating Resource AllocationAnthony FullertonNo ratings yet

- Fiim S02Document45 pagesFiim S02Ali MohammedNo ratings yet

- Financial MarketDocument8 pagesFinancial Marketshahid3454No ratings yet

- Financial Ins & MKTDocument7 pagesFinancial Ins & MKTdkaluale16No ratings yet

- Financial IntermediaryDocument4 pagesFinancial IntermediaryValerie Mae AbuyenNo ratings yet

- Ramiro, Lorren - Money MarketsDocument4 pagesRamiro, Lorren - Money Marketslorren ramiroNo ratings yet

- Finmar NotesDocument5 pagesFinmar NotesariannejonesmNo ratings yet

- FIN111 Spring2015 Tutorials Tutorial 5 Week 6 QuestionsDocument3 pagesFIN111 Spring2015 Tutorials Tutorial 5 Week 6 QuestionshaelstoneNo ratings yet

- Personal Finance-Module 2Document33 pagesPersonal Finance-Module 2Jhaira BarandaNo ratings yet

- 3 - Financial InstitutionsDocument7 pages3 - Financial InstitutionsArmeen KhanNo ratings yet

- Christiene P. Schwandner: Financial Sector DefinedDocument4 pagesChristiene P. Schwandner: Financial Sector DefinedGladys Gaccion OpitzNo ratings yet

- Indian Money MarketDocument8 pagesIndian Money MarketRey ArNo ratings yet

- Activity On Application ControlDocument5 pagesActivity On Application ControlPaupauNo ratings yet

- Activity - Derivatives and Hedging Accounting (PFRS 9)Document8 pagesActivity - Derivatives and Hedging Accounting (PFRS 9)PaupauNo ratings yet

- Activity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)Document1 pageActivity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)PaupauNo ratings yet

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Assessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerDocument12 pagesAssessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerPaupauNo ratings yet

- Accounting for Cash, Receivables and InventoriesDocument12 pagesAccounting for Cash, Receivables and InventoriesPaupau100% (1)

- Activity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Document11 pagesActivity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Paupau100% (1)

- Audit 4 - Audit in Specialized IndustryDocument7 pagesAudit 4 - Audit in Specialized IndustryPaupauNo ratings yet

- Actvity 4 in Auditing 4 - Biological AssetsDocument3 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Activity 2 Audit On CISDocument4 pagesActivity 2 Audit On CISPaupauNo ratings yet

- Activity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Document12 pagesActivity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Paupau0% (1)

- Implement Strategy StructureDocument21 pagesImplement Strategy StructurePaupau100% (1)

- Answer in Prelim Exam E4.Document12 pagesAnswer in Prelim Exam E4.PaupauNo ratings yet

- Activity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Document6 pagesActivity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0PaupauNo ratings yet

- AFAR ReviewDocument11 pagesAFAR ReviewPaupauNo ratings yet

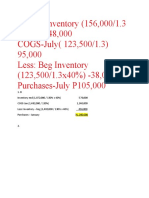

- Ending Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000Document1 pageEnding Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000PaupauNo ratings yet

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- Assignment On PCF and Bank ReconDocument2 pagesAssignment On PCF and Bank ReconPaupauNo ratings yet

- Special Purpose Audit Procedures and ReportsDocument6 pagesSpecial Purpose Audit Procedures and ReportsPaupauNo ratings yet

- Answers - Partnership AccountingDocument14 pagesAnswers - Partnership AccountingPaupauNo ratings yet

- Estimated transaction price methods and entries for consignment salesDocument7 pagesEstimated transaction price methods and entries for consignment salesPaupauNo ratings yet

- Answer in Act. 2 For Cash-receivables-InventoriesDocument10 pagesAnswer in Act. 2 For Cash-receivables-InventoriesPaupauNo ratings yet

- 6 Business StrategyDocument27 pages6 Business StrategyPaupauNo ratings yet

- Management Accounting Techniques CompilationDocument40 pagesManagement Accounting Techniques CompilationGracelle Mae Oraller100% (1)

- Assessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerDocument12 pagesAssessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerPaupauNo ratings yet

- Actvity 4 in Auditing 4 - Biological AssetsDocument2 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Activity 3 - CAATsDocument4 pagesActivity 3 - CAATsPaupauNo ratings yet

- MAS-04 Relevant CostingDocument10 pagesMAS-04 Relevant CostingPaupauNo ratings yet

- PAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesDocument9 pagesPAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesPaupauNo ratings yet

- Activity - Consolidated Financial Statement Part 1Document10 pagesActivity - Consolidated Financial Statement Part 1PaupauNo ratings yet

- Springfield City Council Minutes May 2021Document2 pagesSpringfield City Council Minutes May 2021inforumdocsNo ratings yet

- Imu600 Final July 2022Document3 pagesImu600 Final July 2022fathul dzarifNo ratings yet

- Jasper and Anneka Rehnquist Case StudyDocument2 pagesJasper and Anneka Rehnquist Case StudyChintu WatwaniNo ratings yet

- Financial ServicesDocument182 pagesFinancial ServicesVivek KuchhalNo ratings yet

- FNMNGT 3 Chapter 9 Credit ApplicationDocument18 pagesFNMNGT 3 Chapter 9 Credit ApplicationArlyn BautistaNo ratings yet

- Corporation Law Cases and DigestsDocument12 pagesCorporation Law Cases and DigestsJoshua LanzonNo ratings yet

- Debt FinancingDocument52 pagesDebt FinancingJean Ashley Napoles AbarcaNo ratings yet

- Pre Spanish Philippines1Document8 pagesPre Spanish Philippines1Mark WatneyNo ratings yet

- Corp Fin. WSUV Assignment-1Document2 pagesCorp Fin. WSUV Assignment-1nguyenngockhaihoan811No ratings yet

- Banks Policy On Covid Related Reschedulement of Dues PDFDocument6 pagesBanks Policy On Covid Related Reschedulement of Dues PDFYuva KonapalliNo ratings yet

- 24.2 The Banking System and Money Creation: Search in BookDocument16 pages24.2 The Banking System and Money Creation: Search in BookBeheaded King of HeartNo ratings yet

- Home loan EMI calculator featured articlesDocument2 pagesHome loan EMI calculator featured articlesSushmita SwainNo ratings yet

- June 2017 Past Papers BusinessDocument20 pagesJune 2017 Past Papers BusinessjsyusdjaqNo ratings yet

- FFIEC031 202212 FDocument91 pagesFFIEC031 202212 FBatmanNo ratings yet

- Modern Treasury - Accounting For Developers Parts I-IIIDocument32 pagesModern Treasury - Accounting For Developers Parts I-IIIfelipeap92No ratings yet

- Role of Mutual Funds in Growth of Financial Market" With Special Reference To ICICI .CDocument90 pagesRole of Mutual Funds in Growth of Financial Market" With Special Reference To ICICI .C2014rajpointNo ratings yet

- Finmar Final Quiz Answer KeysDocument15 pagesFinmar Final Quiz Answer KeysGailee VinNo ratings yet

- Fin Ca2 FinalDocument6 pagesFin Ca2 FinalVaishali SonareNo ratings yet

- Bodie Investments PPT CH01Document35 pagesBodie Investments PPT CH01rafat.jalladNo ratings yet

- Your Credit Report SummaryDocument30 pagesYour Credit Report SummaryJosue BonillaNo ratings yet

- Atp Case DigestsDocument7 pagesAtp Case DigestsVenus Jane FinuliarNo ratings yet

- Calculate simple and compound interestDocument9 pagesCalculate simple and compound interestEi HmmmNo ratings yet

- Anshul-Project Report - 111Document81 pagesAnshul-Project Report - 111Abhishek GuptaNo ratings yet

- ACFDocument9 pagesACFduaa fatimaNo ratings yet

- Dokumen - Tips Commodatum Vs Mutuum Vs DepositDocument8 pagesDokumen - Tips Commodatum Vs Mutuum Vs DepositShazna SendicoNo ratings yet

- How RBI Controls Money Supply and Credit Through Various ToolsDocument4 pagesHow RBI Controls Money Supply and Credit Through Various ToolsAkrutNo ratings yet

- MurabahaDocument11 pagesMurabahaOGETO WESLEYNo ratings yet