You might also like

- Manual Micro DNC 2dDocument31 pagesManual Micro DNC 2dDiego GarciaNo ratings yet

- FAR 1st Monthly AssessmentDocument5 pagesFAR 1st Monthly AssessmentCiena Mae AsasNo ratings yet

- Exam 1 - Prelims - Key AnswersDocument16 pagesExam 1 - Prelims - Key AnswersClint AbenojaNo ratings yet

- Term 1 ReviewerDocument11 pagesTerm 1 ReviewerNieryl Mae RivasNo ratings yet

- Financial Reporting I: Key Accounting ConceptsDocument5 pagesFinancial Reporting I: Key Accounting ConceptsKim Cristian Maaño50% (2)

- Multiple ChoiceDocument6 pagesMultiple Choicetough mamaNo ratings yet

- Midterm Reviewer Part 1Document15 pagesMidterm Reviewer Part 1키지아No ratings yet

- CFASDocument5 pagesCFASBunny Kookie100% (1)

- Financial Accounting and Reporting-Preliminary ExamDocument7 pagesFinancial Accounting and Reporting-Preliminary Examromark lopezNo ratings yet

- Xy95lywmi - Midterm Exam FarDocument12 pagesXy95lywmi - Midterm Exam FarLyra Mae De BotonNo ratings yet

- Quiz BowlDocument2 pagesQuiz Bowlaccounting probNo ratings yet

- Practice Problem Jenny Light AccountantDocument17 pagesPractice Problem Jenny Light AccountantFranco James SanpedroNo ratings yet

- CFAS - Final Exam ADocument11 pagesCFAS - Final Exam AKristine Esplana ToraldeNo ratings yet

- Accounting For Merchandising BusinessDocument27 pagesAccounting For Merchandising Businessarnel barawedNo ratings yet

- Cfas Exercise 2Document7 pagesCfas Exercise 2BlueBladeNo ratings yet

- Provisions, Cont. Liability, & Cont. AssetsDocument40 pagesProvisions, Cont. Liability, & Cont. Assetsyonas alemuNo ratings yet

- Ve4psutoy Activity Chapter 8 Adjusting EntriesDocument3 pagesVe4psutoy Activity Chapter 8 Adjusting EntriesLyra Mae De Boton100% (1)

- Far Reviewer 1Document4 pagesFar Reviewer 1MARK JAYSON MANABATNo ratings yet

- Financial Accounting & Reporting First Grading Examination: Name: Date: Professor: Section: ScoreDocument15 pagesFinancial Accounting & Reporting First Grading Examination: Name: Date: Professor: Section: ScoreCUSTODIO, JUSTINE A.No ratings yet

- Polytechnic University College Accountancy ExamDocument14 pagesPolytechnic University College Accountancy ExamEdison San Juan100% (1)

- Mock Examination QuestionnaireDocument9 pagesMock Examination QuestionnaireRenabelle CagaNo ratings yet

- Revised Conceptual Framework Quiz AnswersDocument11 pagesRevised Conceptual Framework Quiz AnswersAlleah Mae Del RosarioNo ratings yet

- Final Exam Enhanced 1 1Document8 pagesFinal Exam Enhanced 1 1Villanueva Rosemarie100% (1)

- Test Bank Notes ReceivableDocument5 pagesTest Bank Notes ReceivableErrold john DulatreNo ratings yet

- Freshmen Orientation PPT AY21 22 For Distribution To StudentsDocument78 pagesFreshmen Orientation PPT AY21 22 For Distribution To StudentsDANIELLE TORRANCE ESPIRITUNo ratings yet

- CFAS.101 - Diagnostic Test Part 2Document2 pagesCFAS.101 - Diagnostic Test Part 2Mika MolinaNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument20 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionFebby Grace Villaceran Sabino0% (2)

- Semi Final Exam (Accounting)Document4 pagesSemi Final Exam (Accounting)MyyMyy JerezNo ratings yet

- Standard, The Conceptual Framework Overrides That StandardDocument6 pagesStandard, The Conceptual Framework Overrides That StandardwivadaNo ratings yet

- Conceptual Framework Guides Financial Reporting StandardsDocument3 pagesConceptual Framework Guides Financial Reporting StandardsJynilou PinoteNo ratings yet

- Far Reviewer For FinalsDocument38 pagesFar Reviewer For Finalsjessamae gundanNo ratings yet

- Type of AccountsDocument4 pagesType of AccountsIgnacio De LunaNo ratings yet

- Quiz-Review CfasDocument5 pagesQuiz-Review CfasMa Louise Ivy RosalesNo ratings yet

- Introduction to Accounting ConceptsDocument10 pagesIntroduction to Accounting ConceptsKysha YnaresNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument31 pagesAccounting Cycle of A Merchandising BusinessAresta, Novie Mae100% (1)

- Toaz - Info Quiz 6 With Solutiondocx PRDocument15 pagesToaz - Info Quiz 6 With Solutiondocx PRReland CastroNo ratings yet

- Polytechnic University Midterm Exam Adjusting EntriesDocument7 pagesPolytechnic University Midterm Exam Adjusting EntriesEdison San JuanNo ratings yet

- Pa48b6epp Prelim ExaminationDocument16 pagesPa48b6epp Prelim ExaminationJames CastañedaNo ratings yet

- Basic Accounting Worksheet ColumnsDocument26 pagesBasic Accounting Worksheet ColumnsApril Joy EspadorNo ratings yet

- Reviewer in PartnershipDocument3 pagesReviewer in PartnershipMeghan Kaye LiwenNo ratings yet

- Quiz - SFP With AnswersDocument4 pagesQuiz - SFP With Answersjanus lopezNo ratings yet

- CFAS ReviewerDocument17 pagesCFAS ReviewerJoshua Vladimir RodriguezNo ratings yet

- Adjusting Entries With AnswersDocument7 pagesAdjusting Entries With AnswersMichael Magdaog100% (1)

- PAS 16 Property Plant and EquipmentDocument22 pagesPAS 16 Property Plant and EquipmentPatawaran, Janelle S.No ratings yet

- Drills on Accounting ConceptsDocument5 pagesDrills on Accounting ConceptsAnne AlagNo ratings yet

- Government Grants: Use The Following Information For The Next Three QuestionsDocument2 pagesGovernment Grants: Use The Following Information For The Next Three QuestionsXienaNo ratings yet

- Study well and don't cheat on examDocument7 pagesStudy well and don't cheat on examchristine anglaNo ratings yet

- PAS 7 Cash FlowsDocument14 pagesPAS 7 Cash FlowsCarlo Lopez CantadaNo ratings yet

- Page 75Document3 pagesPage 75Aya AlayonNo ratings yet

- Accounting Cycle: 4. Preparation of The Trial BalanceDocument8 pagesAccounting Cycle: 4. Preparation of The Trial BalanceAda Janelle Manzano0% (1)

- Name: Date: Score: Course/Year/Section: Professor: Practice Activity 3: Journal Entries Problem 1Document1 pageName: Date: Score: Course/Year/Section: Professor: Practice Activity 3: Journal Entries Problem 1BathalaNo ratings yet

- Bsa Online Quiz 1 - Overview of AccountingDocument9 pagesBsa Online Quiz 1 - Overview of AccountingRyzeNo ratings yet

- Seeds of The Nations Review-MidtermsDocument9 pagesSeeds of The Nations Review-MidtermsMikaela JeanNo ratings yet

- Accounting ReviewerDocument21 pagesAccounting ReviewerAdriya Ley PangilinanNo ratings yet

- Sol. Man. - Chapter 1 - The Accounting Process - Ia Part 1aDocument6 pagesSol. Man. - Chapter 1 - The Accounting Process - Ia Part 1aMiguel AmihanNo ratings yet

- Basic Accounting: Multiple ChoiceDocument38 pagesBasic Accounting: Multiple ChoiceErika GambolNo ratings yet

- This Study Resource Was: SolutionDocument6 pagesThis Study Resource Was: SolutionChris Jay LatibanNo ratings yet

- Adjusting Entries QuizDocument12 pagesAdjusting Entries QuizJuan Dela CruzNo ratings yet

- CPAR TOA Pre-Board FinalDocument10 pagesCPAR TOA Pre-Board FinalJericho Pedragosa100% (1)

- Theory of Accounts - Cpa-ReviewerDocument10 pagesTheory of Accounts - Cpa-ReviewerHeart EspineliNo ratings yet

- Financial Acctg 1 ReviewerDocument9 pagesFinancial Acctg 1 ReviewerAllyza May GasparNo ratings yet

- Activity On Application ControlDocument5 pagesActivity On Application ControlPaupauNo ratings yet

- Activity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)Document1 pageActivity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)PaupauNo ratings yet

- Activity - Derivatives and Hedging Accounting (PFRS 9)Document8 pagesActivity - Derivatives and Hedging Accounting (PFRS 9)PaupauNo ratings yet

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Actvity 4 in Auditing 4 - Biological AssetsDocument3 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Activity 2 Audit On CISDocument4 pagesActivity 2 Audit On CISPaupauNo ratings yet

- Accounting for Cash, Receivables and InventoriesDocument12 pagesAccounting for Cash, Receivables and InventoriesPaupau100% (1)

- Assessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerDocument12 pagesAssessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerPaupauNo ratings yet

- Implement Strategy StructureDocument21 pagesImplement Strategy StructurePaupau100% (1)

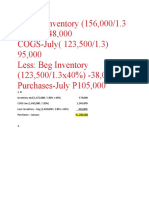

- Ending Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000Document1 pageEnding Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000PaupauNo ratings yet

- Audit 4 - Audit in Specialized IndustryDocument7 pagesAudit 4 - Audit in Specialized IndustryPaupauNo ratings yet

- Activity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Document11 pagesActivity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Paupau100% (1)

- Activity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Document6 pagesActivity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0PaupauNo ratings yet

- Activity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Document12 pagesActivity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Paupau0% (1)

- AFAR ReviewDocument11 pagesAFAR ReviewPaupauNo ratings yet

- Assignment On PCF and Bank ReconDocument2 pagesAssignment On PCF and Bank ReconPaupauNo ratings yet

- Estimated transaction price methods and entries for consignment salesDocument7 pagesEstimated transaction price methods and entries for consignment salesPaupauNo ratings yet

- Answer in Act. 2 For Cash-receivables-InventoriesDocument10 pagesAnswer in Act. 2 For Cash-receivables-InventoriesPaupauNo ratings yet

- Special Purpose Audit Procedures and ReportsDocument6 pagesSpecial Purpose Audit Procedures and ReportsPaupauNo ratings yet

- 6 Business StrategyDocument27 pages6 Business StrategyPaupauNo ratings yet

- Activity 3 - CAATsDocument4 pagesActivity 3 - CAATsPaupauNo ratings yet

- Answers - Partnership AccountingDocument14 pagesAnswers - Partnership AccountingPaupauNo ratings yet

- Management Accounting Techniques CompilationDocument40 pagesManagement Accounting Techniques CompilationGracelle Mae Oraller100% (1)

- Actvity 4 in Auditing 4 - Biological AssetsDocument2 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- MAS-04 Relevant CostingDocument10 pagesMAS-04 Relevant CostingPaupauNo ratings yet

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- PAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesDocument9 pagesPAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesPaupauNo ratings yet

- Assessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerDocument12 pagesAssessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerPaupauNo ratings yet

- Activity - Consolidated Financial Statement Part 1Document10 pagesActivity - Consolidated Financial Statement Part 1PaupauNo ratings yet

- Prison Architect Calculator (V2.0)Document11 pagesPrison Architect Calculator (V2.0)freakman89No ratings yet

- BSW, BS,,AF, BA and Metric Tool SizeDocument4 pagesBSW, BS,,AF, BA and Metric Tool SizeUNES100% (1)

- Fusion Accounting Hub 304046 PDFDocument14 pagesFusion Accounting Hub 304046 PDFrpgudlaNo ratings yet

- Truck-Mounted Cranes: For Applications With Large Vehicles HB-R Series, The Perfect SolutionDocument4 pagesTruck-Mounted Cranes: For Applications With Large Vehicles HB-R Series, The Perfect SolutionRodrigo LealNo ratings yet

- (GUIDE) Advanced Interactive Governor Tweaks Buttery Smooth and Insane Battery Life! - Page 519 - Xda-DevelopersDocument3 pages(GUIDE) Advanced Interactive Governor Tweaks Buttery Smooth and Insane Battery Life! - Page 519 - Xda-Developersdadme010% (2)

- Materials Storage and BuildingDocument3 pagesMaterials Storage and BuildingAmit GoyalNo ratings yet

- Agni Free PDF - 2 For Sbi Clerk Mains 2024Document18 pagesAgni Free PDF - 2 For Sbi Clerk Mains 2024supriyo248650No ratings yet

- TP 6799Document84 pagesTP 6799Roberto Sanchez Zapata100% (1)

- ELEC 121 - Philippine Popular CultureDocument10 pagesELEC 121 - Philippine Popular CultureMARITONI MEDALLANo ratings yet

- Baja2018 Unisa Team3 Design ReportDocument23 pagesBaja2018 Unisa Team3 Design ReportDaniel MabengoNo ratings yet

- Week 2 - Assignment SolutionsDocument2 pagesWeek 2 - Assignment SolutionsSanyamNo ratings yet

- Rolling ResistanceDocument12 pagesRolling Resistancemu_rajesh3415No ratings yet

- Decolonising The FutureDocument20 pagesDecolonising The Futurebybee7207No ratings yet

- J-19-16-III - Bengali - FDocument24 pagesJ-19-16-III - Bengali - FDebayanbasu.juNo ratings yet

- Inspection & Testing of Elastic Rail Clips PDFDocument5 pagesInspection & Testing of Elastic Rail Clips PDFfiemsabyasachi0% (1)

- Penetron Admix FlyerDocument2 pagesPenetron Admix Flyernght7942No ratings yet

- MR Khurram Chakwal 6kw Hybrid - 024627Document6 pagesMR Khurram Chakwal 6kw Hybrid - 024627Shahid HussainNo ratings yet

- Blue Assured Individual Health PlanDocument5 pagesBlue Assured Individual Health PlanahsanNo ratings yet

- S3 Unseen PracticeDocument7 pagesS3 Unseen PracticeTanush GoelNo ratings yet

- Friends or Lovers (A Novel by Rory Ridley-Duff) - View in Full Screen ModeDocument336 pagesFriends or Lovers (A Novel by Rory Ridley-Duff) - View in Full Screen ModeRory Ridley Duff92% (24)

- Cis Bin Haider GRP LTD - HSBC BankDocument5 pagesCis Bin Haider GRP LTD - HSBC BankEllerNo ratings yet

- Indian Standard: Methods For Sampling of Clay Building BricksDocument9 pagesIndian Standard: Methods For Sampling of Clay Building BricksAnonymous i6zgzUvNo ratings yet

- Huawei Tecal RH2288 V2 Server Compatibility List PDFDocument30 pagesHuawei Tecal RH2288 V2 Server Compatibility List PDFMenganoFulanoNo ratings yet

- DNV Casualty Info 2011 #3Document2 pagesDNV Casualty Info 2011 #3Sureen NarangNo ratings yet

- Telecommunications: Office of The Communications Authority (OFCA)Document2 pagesTelecommunications: Office of The Communications Authority (OFCA)ChiWoTangNo ratings yet

- Monographie BtttyrtIPM-5 Tables Vol7Document246 pagesMonographie BtttyrtIPM-5 Tables Vol7arengifoipenNo ratings yet

- 737 Flow and ChecklistDocument7 pages737 Flow and ChecklistarelundhansenNo ratings yet

- Ict OhsDocument26 pagesIct Ohscloyd mark cabusogNo ratings yet

- Bank Account Details and Contact NumbersDocument38 pagesBank Account Details and Contact NumbersD-Blitz StudioNo ratings yet