You might also like

- Financial Reporting I: Key Accounting ConceptsDocument5 pagesFinancial Reporting I: Key Accounting ConceptsKim Cristian Maaño50% (2)

- Final Exam Enhanced 1 1Document8 pagesFinal Exam Enhanced 1 1Villanueva Rosemarie100% (1)

- SGV Cup AccountingDocument13 pagesSGV Cup AccountingMCDABCNo ratings yet

- Midterms Conceptual Framework and Accounting StandardsDocument9 pagesMidterms Conceptual Framework and Accounting StandardsMay Anne MenesesNo ratings yet

- Quiz - SFP With AnswersDocument4 pagesQuiz - SFP With Answersjanus lopezNo ratings yet

- Summary of Ifrs 5Document4 pagesSummary of Ifrs 5Divine Epie Ngol'esuehNo ratings yet

- Statement of Comprehensive IncomeDocument4 pagesStatement of Comprehensive Incomebobo tangaNo ratings yet

- Far Week 6 Investment Properties RevieweesDocument4 pagesFar Week 6 Investment Properties RevieweesAdan NadaNo ratings yet

- 02 Conceptual Framework - RevisedDocument13 pages02 Conceptual Framework - RevisedRazel MhinNo ratings yet

- Far - Mock BoardDocument11 pagesFar - Mock BoardKial PachecoNo ratings yet

- Answer FIN 081 P1 - C1Document4 pagesAnswer FIN 081 P1 - C1marvinNo ratings yet

- Bsa Online Quiz 1 - Overview of AccountingDocument9 pagesBsa Online Quiz 1 - Overview of AccountingRyzeNo ratings yet

- PAS 1 and PFRS 1 Multiple Choice QuestionsDocument4 pagesPAS 1 and PFRS 1 Multiple Choice Questionsjahnhannalei marticioNo ratings yet

- Intermediate Accounting 1amp2 PDF FreeDocument20 pagesIntermediate Accounting 1amp2 PDF FreeShao LiNo ratings yet

- Investment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldDocument7 pagesInvestment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldMark Anthony SivaNo ratings yet

- Ap 06 REO Receivables - PDF 074431Document19 pagesAp 06 REO Receivables - PDF 074431ChristianNo ratings yet

- 1 - Conceptual Framework Old and New QuestionsDocument10 pages1 - Conceptual Framework Old and New Questionsput a maskNo ratings yet

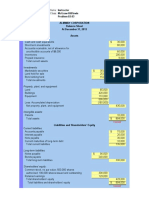

- Intermediate Accounting 3 - Statement of Financial PositionDocument6 pagesIntermediate Accounting 3 - Statement of Financial PositionLuisitoNo ratings yet

- Answer in Prelim Exam E4.Document12 pagesAnswer in Prelim Exam E4.PaupauNo ratings yet

- Quiz 1 P2 FinmanDocument3 pagesQuiz 1 P2 FinmanRochelle Joyce CosmeNo ratings yet

- Examining accounting standards and conceptual frameworkDocument8 pagesExamining accounting standards and conceptual frameworkAmie Jane MirandaNo ratings yet

- 9201 - Partnership FormationDocument4 pages9201 - Partnership FormationBrian Dave OrtizNo ratings yet

- Multiple ChoiceDocument6 pagesMultiple Choicetough mamaNo ratings yet

- CW6 - MaterialityDocument3 pagesCW6 - MaterialityBeybi JayNo ratings yet

- PFRS 14 15 16Document3 pagesPFRS 14 15 16kara mNo ratings yet

- ReSA CPA Review Batch 44 Investment PropertyDocument10 pagesReSA CPA Review Batch 44 Investment PropertyLei PangilinanNo ratings yet

- Afar 2 Module CH 2Document22 pagesAfar 2 Module CH 2Razmen Ramirez PintoNo ratings yet

- Cfas ReviewerDocument10 pagesCfas ReviewershaylieeeNo ratings yet

- Intermediate Accounting 3 Part 1 Statement of Comprehensive Income ProblemsDocument7 pagesIntermediate Accounting 3 Part 1 Statement of Comprehensive Income ProblemsAG VenturesNo ratings yet

- CFAS.101 - Diagnostic Test Part 2Document2 pagesCFAS.101 - Diagnostic Test Part 2Mika MolinaNo ratings yet

- Manage PPE AssetsDocument4 pagesManage PPE AssetsKris Hazel RentonNo ratings yet

- Chapter 6 TBDocument26 pagesChapter 6 TBSophia UnaNo ratings yet

- Bsat 2019Document23 pagesBsat 2019rowena adobasNo ratings yet

- ACC1003 Practice QuestionsDocument6 pagesACC1003 Practice Questionsmeera abdullahNo ratings yet

- Discontinued Operations ProblemsDocument4 pagesDiscontinued Operations ProblemsJeane Mae BooNo ratings yet

- Error Correction MethodsDocument2 pagesError Correction MethodsValentina Tan DuNo ratings yet

- Problem 14-5: Kayla Cruz & Gabriel TekikoDocument7 pagesProblem 14-5: Kayla Cruz & Gabriel TekikoNURHAM SUMLAYNo ratings yet

- Cost Concept, Terminologies and BehaviorDocument8 pagesCost Concept, Terminologies and BehaviorANDREA NICOLE DE LEONNo ratings yet

- 85184767Document9 pages85184767Garp BarrocaNo ratings yet

- Updates to IFRS 3 Definition of a Business and IAS 1 and IAS 8 Definition of Material (39 charactersDocument9 pagesUpdates to IFRS 3 Definition of a Business and IAS 1 and IAS 8 Definition of Material (39 charactersShane CabinganNo ratings yet

- Pure TheoriesDocument5 pagesPure Theorieschristine angla100% (1)

- Modul E: Review of Accounting ProcessDocument23 pagesModul E: Review of Accounting ProcessAlijah MercadoNo ratings yet

- Government Accounting and Auditing Part 1Document7 pagesGovernment Accounting and Auditing Part 1Harley GumaponNo ratings yet

- Quiz 1 Midterm InventoriesDocument6 pagesQuiz 1 Midterm InventoriesSophia TenorioNo ratings yet

- Conceptual Framework and Accounting StandardsDocument15 pagesConceptual Framework and Accounting StandardsPrince Jeffrey FernandoNo ratings yet

- Ia2 Prob 1-32 & 33Document1 pageIa2 Prob 1-32 & 33maryaniNo ratings yet

- Maximizing Income from Two Part-Time Jobs with Simplex MethodDocument21 pagesMaximizing Income from Two Part-Time Jobs with Simplex MethodJohn Rovic GamanaNo ratings yet

- Language of businessDocument3 pagesLanguage of businesslemerleNo ratings yet

- Acc 111 Exam GeleraDocument11 pagesAcc 111 Exam GeleraCheska GeleraNo ratings yet

- Toaz - Info Quiz 6 With Solutiondocx PRDocument15 pagesToaz - Info Quiz 6 With Solutiondocx PRReland CastroNo ratings yet

- PAS 16 Property Plant and EquipmentDocument22 pagesPAS 16 Property Plant and EquipmentPatawaran, Janelle S.No ratings yet

- Regulatory Framework For Business TransactionsDocument13 pagesRegulatory Framework For Business TransactionsNash VelisanoNo ratings yet

- Cash Price Equivalent at The Deferred Beyond Normal CreditDocument5 pagesCash Price Equivalent at The Deferred Beyond Normal CreditSharmin ReulaNo ratings yet

- IA3 Statement of Financial PositionDocument36 pagesIA3 Statement of Financial PositionHello HiNo ratings yet

- Module 06 - PPE, Government Grants and Borrowing CostsDocument24 pagesModule 06 - PPE, Government Grants and Borrowing Costspaula manaloNo ratings yet

- CFAS - Final Exam ADocument11 pagesCFAS - Final Exam AKristine Esplana ToraldeNo ratings yet

- Toaz - Info Quiz 3 PRDocument25 pagesToaz - Info Quiz 3 PRAprille Xay TupasNo ratings yet

- Provisions, Cont. Liability, & Cont. AssetsDocument40 pagesProvisions, Cont. Liability, & Cont. Assetsyonas alemuNo ratings yet

- Financial Asset MILLANDocument6 pagesFinancial Asset MILLANAlelie Joy dela CruzNo ratings yet

- Select The Best Answer From The Choices Given.: TheoryDocument14 pagesSelect The Best Answer From The Choices Given.: TheoryROMAR A. PIGANo ratings yet

- Hamilton (Original Broadway Cast Recording) - Act II Booklet (Hi-Res) - FINALDocument32 pagesHamilton (Original Broadway Cast Recording) - Act II Booklet (Hi-Res) - FINALwolfgrin67% (15)

- Chapter-V - Financial-Aspect - RevisedDocument31 pagesChapter-V - Financial-Aspect - RevisedRenabelle CagaNo ratings yet

- AprilDocument1 pageAprilLenny MangaiNo ratings yet

- Grade 5 - SLM - 1 MELC1 Q3 Describing Motion Converted EditedDocument13 pagesGrade 5 - SLM - 1 MELC1 Q3 Describing Motion Converted EditedRenabelle Caga100% (2)

- A Quantitative Research Paper Submitted ToDocument100 pagesA Quantitative Research Paper Submitted ToRenabelle CagaNo ratings yet

- I Hate Tacos... : Said NobodyDocument1 pageI Hate Tacos... : Said NobodyRenabelle CagaNo ratings yet

- 2021 Quotes 05Document1 page2021 Quotes 05Renabelle CagaNo ratings yet

- 2021 FoodDocument1 page2021 FoodRenabelle CagaNo ratings yet

- Grade 5 SLM Q2 Module 6 Interactions Among Living Things and Non Living EditedDocument21 pagesGrade 5 SLM Q2 Module 6 Interactions Among Living Things and Non Living EditedRenabelle Caga100% (2)

- History of Table TennisDocument4 pagesHistory of Table TennisRenabelle CagaNo ratings yet

- Retained Earnings Lecture NotesDocument2 pagesRetained Earnings Lecture Notesbum_24100% (2)

- 2021 Food 02Document1 page2021 Food 02Renabelle CagaNo ratings yet

- 2021 Food 02Document1 page2021 Food 02Renabelle CagaNo ratings yet

- Module 3 Fundamentals, MD, Docu HandlingDocument21 pagesModule 3 Fundamentals, MD, Docu HandlingRenabelle CagaNo ratings yet

- Accounting For Leases: Chapter Learning ObjectivesDocument48 pagesAccounting For Leases: Chapter Learning ObjectivesRenabelle CagaNo ratings yet

- Cpar Far FpbsDocument4 pagesCpar Far FpbsRenabelle CagaNo ratings yet

- EFM4, CH 09, Slides, 07-02-18Document44 pagesEFM4, CH 09, Slides, 07-02-18Renabelle CagaNo ratings yet

- Consumer Behavior of Adolescents in Bacolod City: A Quantitative Study About Vanity, Materialism and Self-DescripancyDocument112 pagesConsumer Behavior of Adolescents in Bacolod City: A Quantitative Study About Vanity, Materialism and Self-DescripancyRenabelle Caga100% (1)

- Motor Vehicles and Road Traffic Regulation 48.50Document411 pagesMotor Vehicles and Road Traffic Regulation 48.50Clayton AllenNo ratings yet

- 9 Principles of Income Tax LawsDocument82 pages9 Principles of Income Tax LawsVyankatesh GotalkarNo ratings yet

- English For Academic and Professional Purposes: Quarter 1 - Module 3Document9 pagesEnglish For Academic and Professional Purposes: Quarter 1 - Module 3John Vincent Salmasan100% (5)

- Optimize School Distribution With MappingDocument5 pagesOptimize School Distribution With MappingRolyn ManansalaNo ratings yet

- Dual Rectifier Solo HeadDocument11 pagesDual Rectifier Solo HeadВиктор АлимовNo ratings yet

- Superior Drummer 2 ManualDocument38 pagesSuperior Drummer 2 ManualEmmanuel MarcosNo ratings yet

- GLOBAL AMITY INSURANCE QUOTE FOR HONDA CITYDocument1 pageGLOBAL AMITY INSURANCE QUOTE FOR HONDA CITYoniNo ratings yet

- This Study Resource Was: Advanced Accounting Ifrs 15Document6 pagesThis Study Resource Was: Advanced Accounting Ifrs 15YukiNo ratings yet

- Quiz II - Company MissionDocument4 pagesQuiz II - Company MissionSuraj SapkotaNo ratings yet

- Multiculturalism Pros and ConsDocument2 pagesMulticulturalism Pros and ConsInês CastanheiraNo ratings yet

- Performance Appraisal at UFLEX Ltd.Document29 pagesPerformance Appraisal at UFLEX Ltd.Mohit MehraNo ratings yet

- "Hybrid" Light Steel Panel and Modular Systems PDFDocument11 pages"Hybrid" Light Steel Panel and Modular Systems PDFTito MuñozNo ratings yet

- Fasttrack - The Supply Chain Magazine (Apr-Jun 2009)Document5 pagesFasttrack - The Supply Chain Magazine (Apr-Jun 2009)SaheemNo ratings yet

- Lay Up ProcedureDocument21 pagesLay Up ProcedureAmir100% (1)

- Topology Optimization of Automotive Brake PedalDocument5 pagesTopology Optimization of Automotive Brake PedalNizam Sudin Dan KhatijahNo ratings yet

- Revised Circular On Secretariat Meeting Held On 9th July, 2023Document4 pagesRevised Circular On Secretariat Meeting Held On 9th July, 2023Mohit SoniNo ratings yet

- Product Information Flyer: Producto RI-923Document2 pagesProduct Information Flyer: Producto RI-923sobheysaidNo ratings yet

- Chapter 3 - Excel SolutionsDocument8 pagesChapter 3 - Excel SolutionsHalt DougNo ratings yet

- 4 AppleDocument9 pages4 AppleSam Peter GeorgieNo ratings yet

- 4) Transport and InsuranceDocument10 pages4) Transport and InsuranceBianca AlecuNo ratings yet

- Amphenol PV Cable AssembliesDocument1 pageAmphenol PV Cable AssembliesLeonardo CoelhoNo ratings yet

- Power Engineering May 2013Document95 pagesPower Engineering May 2013Portal studentesc - EnergeticaNo ratings yet

- Investingunplugged PDFDocument225 pagesInvestingunplugged PDFWilliam MercerNo ratings yet

- Walmart Drug ListDocument6 pagesWalmart Drug ListShirley Pigott MDNo ratings yet

- Unit 1Document176 pagesUnit 1kassahun meseleNo ratings yet

- Microeconomics Primer 1Document15 pagesMicroeconomics Primer 1md1sabeel1ansariNo ratings yet

- Theories of EntrepreneurshipDocument3 pagesTheories of EntrepreneurshipIla Mehrotra Anand80% (5)

- VLSI Design Course PlanDocument2 pagesVLSI Design Course PlanJunaid RajputNo ratings yet

- Assignment 2 QP MPMC - ITDocument1 pageAssignment 2 QP MPMC - ITProjectsNo ratings yet

- Hello World in FortranDocument43 pagesHello World in Fortranhussein alsaedeNo ratings yet