You might also like

- Turnover Tax Text BookDocument6 pagesTurnover Tax Text BookMulugeta AkaluNo ratings yet

- Contemporary World Midterm ExaminationDocument5 pagesContemporary World Midterm Examinationelie lucido100% (2)

- 1 - Cy 2022-2026 MepDocument19 pages1 - Cy 2022-2026 MepArianne SantosNo ratings yet

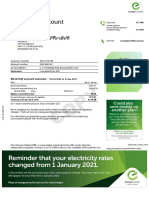

- Electricity Account: Could You Save Money On Another Plan?Document3 pagesElectricity Account: Could You Save Money On Another Plan?ThaiNguyenNo ratings yet

- Equalisation Levy ICAI ModuleDocument37 pagesEqualisation Levy ICAI Modulelekhha bhansaliNo ratings yet

- Equalisation Levy: After Studying This Chapter, You Would Be Able ToDocument29 pagesEqualisation Levy: After Studying This Chapter, You Would Be Able Toyash mehtaNo ratings yet

- K.Vaitheeswaran - UNs Proposed Article 12B-Light at The End of The TunnelDocument4 pagesK.Vaitheeswaran - UNs Proposed Article 12B-Light at The End of The TunnelIshita FarsaiyaNo ratings yet

- Impact of New Tax Regulations On The Indian IT-BPO SectorDocument3 pagesImpact of New Tax Regulations On The Indian IT-BPO SectorPrashant GandhiNo ratings yet

- Dissertation Draft - 1Document15 pagesDissertation Draft - 1Mahima DoshiNo ratings yet

- Saputra (2022)Document24 pagesSaputra (2022)nita_andriyani030413No ratings yet

- Asia Internet Coalition (S.301PublicComment)Document9 pagesAsia Internet Coalition (S.301PublicComment)Suhani ChanchlaniNo ratings yet

- Taxation Law AssignmentDocument8 pagesTaxation Law AssignmentPallavi SharmaNo ratings yet

- Public Benefit Principlein Regulation E-Commerce Tax On Consumers Location in IndonesiaDocument12 pagesPublic Benefit Principlein Regulation E-Commerce Tax On Consumers Location in IndonesiaIndah NovitasariNo ratings yet

- Impact of E-Commerce On Taxation: Kirti and Namrata AgrawalDocument8 pagesImpact of E-Commerce On Taxation: Kirti and Namrata AgrawalseranNo ratings yet

- Public Benefit Principle in Regulating E-Commerce Tax On Consumer's Location in IndonesiaDocument11 pagesPublic Benefit Principle in Regulating E-Commerce Tax On Consumer's Location in IndonesiaArif AfriadyNo ratings yet

- GST ProjectDocument80 pagesGST ProjectBalaram DharaNo ratings yet

- Equalisation Levy Is It A Beginning of A New SagaDocument6 pagesEqualisation Levy Is It A Beginning of A New SagaTaxmann PublicationNo ratings yet

- Indian IT Outlook 2012Document2 pagesIndian IT Outlook 2012SidRoy84No ratings yet

- Digital TaxationDocument3 pagesDigital TaxationVijayant DalalNo ratings yet

- Executive Supplement GSTDocument84 pagesExecutive Supplement GSThkakani1No ratings yet

- Global Minimum TaxDocument3 pagesGlobal Minimum TaxMehar Verma0% (1)

- Ta558909 Fair Taxation Special ReportDocument4 pagesTa558909 Fair Taxation Special ReportsyahrilNo ratings yet

- Impact of GST On Online Marketplaces: WWW - Pwc.inDocument36 pagesImpact of GST On Online Marketplaces: WWW - Pwc.inMiteshNo ratings yet

- Group 6 E-CommerceDocument23 pagesGroup 6 E-CommerceNitinNo ratings yet

- Tax Deduction and Collection at Source: Easing Compliances in IndiaDocument37 pagesTax Deduction and Collection at Source: Easing Compliances in IndiasriangineyamNo ratings yet

- MAP GUIDANCE 7th August 2020Document17 pagesMAP GUIDANCE 7th August 2020Mmmg RaNo ratings yet

- A Month Since Launch, Glitches Continue To Mar Income Tax Portal FunctioningDocument3 pagesA Month Since Launch, Glitches Continue To Mar Income Tax Portal FunctioningTEJASWININo ratings yet

- Cips PB10Document11 pagesCips PB104122220025ineNo ratings yet

- Reaction PaperDocument10 pagesReaction PaperpriyaNo ratings yet

- Technology, Media and Telecom (TMT) : Online Businesses and Disruptive Technologies - Key India Tax and Regulatory AspectsDocument33 pagesTechnology, Media and Telecom (TMT) : Online Businesses and Disruptive Technologies - Key India Tax and Regulatory AspectsSunny KhavleNo ratings yet

- Automation and Tax Compliance Empirical Evidence From Nigeria 2020Document10 pagesAutomation and Tax Compliance Empirical Evidence From Nigeria 2020Stalyn Celi BarreraNo ratings yet

- Unit V - E-Commerce - LawsDocument7 pagesUnit V - E-Commerce - LawsDr. Azhar Ahmed SheikhNo ratings yet

- Vodafone Taxation Case StudyDocument20 pagesVodafone Taxation Case Studygauravtu06No ratings yet

- Seminar in Economics Policy FinalDocument19 pagesSeminar in Economics Policy FinalSyed Taqi HaiderNo ratings yet

- Tax Implications On Cross Border Mergers and Acquisitions-Indian PerspectiveDocument5 pagesTax Implications On Cross Border Mergers and Acquisitions-Indian Perspectivesiddharth pandeyNo ratings yet

- Thesis International TaxationDocument7 pagesThesis International Taxationdeniseenriquezglendale100% (2)

- Thesis On Goods and Service TaxDocument5 pagesThesis On Goods and Service TaxRobin Beregovska100% (1)

- Automation and Tax Compliance in NigeriaDocument10 pagesAutomation and Tax Compliance in NigeriapaulevbadeeseosaNo ratings yet

- TaxationDocument7 pagesTaxationChaitra KNo ratings yet

- T I E L: I U: He Ndian Qualisation Evy Nelegant But Not NexpectedDocument24 pagesT I E L: I U: He Ndian Qualisation Evy Nelegant But Not NexpectedSTQNo ratings yet

- International Taxation 2022Document2 pagesInternational Taxation 2022SS17No ratings yet

- Taxation Thesis PDFDocument6 pagesTaxation Thesis PDFgbvexter100% (1)

- Article - Shefali Goradia - Jul 121341305754Document9 pagesArticle - Shefali Goradia - Jul 121341305754Alok Kumar ShuklaNo ratings yet

- Economic Analysis of India's Double Tax Avoidance AgreementsDocument33 pagesEconomic Analysis of India's Double Tax Avoidance AgreementsSukhdeep RandhawaNo ratings yet

- Obayemi Emmanuel Ayomide ID Number: 20222928 Taxation Theory and PracticeDocument6 pagesObayemi Emmanuel Ayomide ID Number: 20222928 Taxation Theory and PracticeObayemi AyomideNo ratings yet

- Taxjournal July 2020Document60 pagesTaxjournal July 2020Venkatesh PrabhuNo ratings yet

- The Superiority of The Digital Service Tax Over Significant DigitDocument29 pagesThe Superiority of The Digital Service Tax Over Significant DigitFa SyNo ratings yet

- Tax ReformDocument5 pagesTax Reformakky.vns2004No ratings yet

- Taxation Law Assignment by Sushali Shruti 18FLICDDN01144Document10 pagesTaxation Law Assignment by Sushali Shruti 18FLICDDN01144Shreya VermaNo ratings yet

- Ayushi PatraDocument12 pagesAyushi PatraAdithya anilNo ratings yet

- International Taxation in India - Recent Developments & Outlook (Part - Ii)Document6 pagesInternational Taxation in India - Recent Developments & Outlook (Part - Ii)ManishJainNo ratings yet

- Taxing Digital Firms 1708629656Document9 pagesTaxing Digital Firms 1708629656Kagoro TendoNo ratings yet

- Beginners Guide On GSTDocument66 pagesBeginners Guide On GSTajimon100% (2)

- Tax FinalDocument3 pagesTax FinalMohammad AliNo ratings yet

- VAT Road To GSTDocument19 pagesVAT Road To GSTVarun PuriNo ratings yet

- Taxation On The Digital Economy in India An AnalysisDocument16 pagesTaxation On The Digital Economy in India An AnalysisNUPUR MISHRANo ratings yet

- Tax Laws Indirect Taxes For December 2020 ExamDocument53 pagesTax Laws Indirect Taxes For December 2020 ExamprofessorrlakshmikanthNo ratings yet

- Company LawDocument18 pagesCompany LawTanya SinghNo ratings yet

- GST - A Game Changer: 2. Review of LiteratureDocument3 pagesGST - A Game Changer: 2. Review of LiteratureInternational Journal in Management Research and Social ScienceNo ratings yet

- GST - A Game Changer: 2. Review of LiteratureDocument3 pagesGST - A Game Changer: 2. Review of LiteratureMoumita Mishra100% (1)

- EY Tax - Vietnam Implements Taxation of Digital Transactions - 2020Document4 pagesEY Tax - Vietnam Implements Taxation of Digital Transactions - 2020Pham Ha AnNo ratings yet

- Practice Questions: Tax LawsDocument53 pagesPractice Questions: Tax Lawshariom bajpaiNo ratings yet

- Tax and MSMEs in the Digital Age: Why Do We Need To Pay Taxes And What Are The Benefits For Us As MSME Entrepreneurs And How To Build Regulations That Are Empathetic And Proven To Encourage Tax Revenue In The Informal SectorFrom EverandTax and MSMEs in the Digital Age: Why Do We Need To Pay Taxes And What Are The Benefits For Us As MSME Entrepreneurs And How To Build Regulations That Are Empathetic And Proven To Encourage Tax Revenue In The Informal SectorNo ratings yet

- Air Customs Chennai International Airport Welcomes YouDocument26 pagesAir Customs Chennai International Airport Welcomes YousreeramaNo ratings yet

- Ahmedabad Municipal Corporation Mahanagar Sewa SadanDocument1 pageAhmedabad Municipal Corporation Mahanagar Sewa SadanEng SvshahNo ratings yet

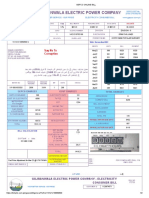

- 553 Units Rs. 9,452.56: Justice Zahirul Hasnain Lari EsqrDocument2 pages553 Units Rs. 9,452.56: Justice Zahirul Hasnain Lari EsqrUroona MalikNo ratings yet

- Custom Shipping and InsuranceDocument302 pagesCustom Shipping and InsuranceJagat PatelNo ratings yet

- VLT - Go MS 90Document2 pagesVLT - Go MS 90Raghu Ram100% (3)

- Apush Review: Henry Clay'S (Part of Key CONCEPT 4.2) : American SystemDocument9 pagesApush Review: Henry Clay'S (Part of Key CONCEPT 4.2) : American SystemNOT Low-brass-exeNo ratings yet

- Calculation of Total Tax Incidence (TTI) For ImportDocument4 pagesCalculation of Total Tax Incidence (TTI) For ImportMd. Mehedi Hasan AnikNo ratings yet

- Solution Manual For International Economics 15th Edition DownloadDocument3 pagesSolution Manual For International Economics 15th Edition DownloadJoshuaLunasago100% (37)

- Uniti 140910105242 Phpapp02Document43 pagesUniti 140910105242 Phpapp02Raj naveenNo ratings yet

- Food Bill 1Document1 pageFood Bill 1Jalaj GuptaNo ratings yet

- Information For Items 21 & 22Document3 pagesInformation For Items 21 & 22Kurt Morin CantorNo ratings yet

- Historical Development of of Taxation Principles and Law in KenyaDocument17 pagesHistorical Development of of Taxation Principles and Law in KenyaJustus AmitoNo ratings yet

- Sopore Law CollegeDocument7 pagesSopore Law Collegelone NasirNo ratings yet

- 400 Billion: Power Distribution in EuropeDocument26 pages400 Billion: Power Distribution in EuropecokavolitangoNo ratings yet

- Gepco Online BillDocument2 pagesGepco Online BillUzair IslamNo ratings yet

- Chapter 3-Intro To Bus. TaxDocument8 pagesChapter 3-Intro To Bus. TaxShiNo ratings yet

- Introduction To Goods and Service Tax (GST) - PART 1Document5 pagesIntroduction To Goods and Service Tax (GST) - PART 1Sakthi MaheswariNo ratings yet

- Formulation of National Trade PoliciesDocument15 pagesFormulation of National Trade Policiesrafid siddiqeNo ratings yet

- SEZ Act 2005Document8 pagesSEZ Act 2005naina saxenaNo ratings yet

- The Billing Mechanism Has Been Revised So That The Benefit of One Previous / Preceeding Slab Is Available To Domestic Consumers (Residential User)Document1 pageThe Billing Mechanism Has Been Revised So That The Benefit of One Previous / Preceeding Slab Is Available To Domestic Consumers (Residential User)Mehtab MalikNo ratings yet

- I. Doctrines in Taxation: I.1. Prospectivity of Tax Laws I. Prescriptions Found in StatutesDocument1 pageI. Doctrines in Taxation: I.1. Prospectivity of Tax Laws I. Prescriptions Found in StatutesAdam CuencaNo ratings yet

- 5 Clase 5 Paper Incentives RE V - FINALDocument40 pages5 Clase 5 Paper Incentives RE V - FINALFranko EncaladaNo ratings yet

- Log in Print Ticket Cancel Ticket: Dear CustomerDocument5 pagesLog in Print Ticket Cancel Ticket: Dear CustomerSUNIL SANGWANNo ratings yet

- TAXATIONDocument3 pagesTAXATIONFhatima Ashra Latip WajaNo ratings yet

- Ac GST Credit NoteDocument1 pageAc GST Credit NoteSudip SinghNo ratings yet

- World Trade Organisation Export ImportDocument2 pagesWorld Trade Organisation Export Importprashantchauhan928No ratings yet

- Import Local Charges (Update 29.12.2023)Document5 pagesImport Local Charges (Update 29.12.2023)Lê Thị Diễm MiNo ratings yet