You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Quick Administrative Process Plus Court Enforcement ProcessDocument53 pagesQuick Administrative Process Plus Court Enforcement ProcessBrad100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Investment BankingDocument27 pagesInvestment BankingAkshatha UpadhyayNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 3 Months Statement. SAUDA 18Document2 pages3 Months Statement. SAUDA 18Fikile Eem100% (1)

- Fixed Deposit Receipt FormatDocument9 pagesFixed Deposit Receipt Formatशुभ चिंतकNo ratings yet

- Currency SwapsDocument33 pagesCurrency SwapsManasvi ShahNo ratings yet

- Real Estate COO VP Operations in NYC Resume Barrett EinauglerDocument2 pagesReal Estate COO VP Operations in NYC Resume Barrett EinauglerBarrettEinauglerNo ratings yet

- CH 5Document83 pagesCH 5Von BerjaNo ratings yet

- Session 4 - DisbursementsDocument80 pagesSession 4 - DisbursementsChris WongNo ratings yet

- Nov 2018 RTP PDFDocument21 pagesNov 2018 RTP PDFManasa SureshNo ratings yet

- Mock Test Q2 PDFDocument5 pagesMock Test Q2 PDFManasa SureshNo ratings yet

- Mock Test Q1 PDFDocument4 pagesMock Test Q1 PDFManasa SureshNo ratings yet

- May 2018 Actual A Paper PDFDocument17 pagesMay 2018 Actual A Paper PDFManasa SureshNo ratings yet

- Synopsis-BBA Project - KIRAN NAINWAR 1Document10 pagesSynopsis-BBA Project - KIRAN NAINWAR 1Kiran NainwarNo ratings yet

- Daring DerivativesDocument3 pagesDaring DerivativesSakha SabkaNo ratings yet

- Gateway of Tally-Accounts Info-Ledger-CreateDocument6 pagesGateway of Tally-Accounts Info-Ledger-CreatebhagathnagarNo ratings yet

- All Alerts For 19 Jan - ChartinkDocument20 pagesAll Alerts For 19 Jan - Chartinkkashinath09No ratings yet

- Indian Institute of Management BangaloreDocument4 pagesIndian Institute of Management BangaloreAkshayNo ratings yet

- Project Report On Selection and Recruitment Procedure of Axis BankDocument12 pagesProject Report On Selection and Recruitment Procedure of Axis BankBryan Parker0% (1)

- Islamic Trade Finance Group-7 FinalDocument11 pagesIslamic Trade Finance Group-7 FinalKaushik HazarikaNo ratings yet

- FraudDocument10 pagesFraudbeboo khanNo ratings yet

- JAI Web Catalogue August 2021Document143 pagesJAI Web Catalogue August 2021DCGBNo ratings yet

- Origin, History and Types of Banking SystemDocument44 pagesOrigin, History and Types of Banking Systemriajul islam jamiNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancesamarth agrawalNo ratings yet

- Financial Analysis of Kumari Bank Limited 2022Document41 pagesFinancial Analysis of Kumari Bank Limited 2022Prajwola Gajurel100% (3)

- ChallanDocument1 pageChallansharoz khanNo ratings yet

- Maha Super Housing LoanDocument4 pagesMaha Super Housing Loansakshishree09No ratings yet

- Currency System in India RBI RoleDocument11 pagesCurrency System in India RBI RoleSharon NunesNo ratings yet

- Director International Business Finance in NYC Resume Stephen SohnDocument4 pagesDirector International Business Finance in NYC Resume Stephen SohnStephenSohnNo ratings yet

- The Mint Power Parity TheoryDocument1 pageThe Mint Power Parity Theoryvivek2270834No ratings yet

- Canada's Top 50 FinTech CompaniesDocument16 pagesCanada's Top 50 FinTech CompaniesTina SmithNo ratings yet

- Vartana Final PresentationDocument14 pagesVartana Final PresentationsuryakantbhaiNo ratings yet

- US Hits Out at China Business ClimateDocument8 pagesUS Hits Out at China Business ClimateJayce LimNo ratings yet

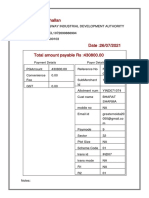

- NEFT/RTGS Challan: Yamuna Expressway Industrial Development Authority ICL1072699866994 ICIC0000103Document2 pagesNEFT/RTGS Challan: Yamuna Expressway Industrial Development Authority ICL1072699866994 ICIC0000103Bharat SharmaNo ratings yet

- Audit of Cash and Cash EquivalentDocument5 pagesAudit of Cash and Cash EquivalentGONZALES, MICA ANGEL A.No ratings yet