You might also like

- Notes Receivable - Ia 1Document4 pagesNotes Receivable - Ia 1Aldrin CabangbangNo ratings yet

- Premiums and WarrantiesDocument3 pagesPremiums and WarrantiesMicaella Grande50% (2)

- P1-PB. Sample Preboard Exam PDFDocument12 pagesP1-PB. Sample Preboard Exam PDFAj VesquiraNo ratings yet

- Q1Document6 pagesQ1Ray Pop0% (2)

- RevalDocument2 pagesRevalRusselle Therese DaitolNo ratings yet

- Notes Receivable Accounting: Initial Measurement, Subsequent Measurement & Treatment of Dishonored NotesDocument104 pagesNotes Receivable Accounting: Initial Measurement, Subsequent Measurement & Treatment of Dishonored NotesXander Clock50% (2)

- Investment in Bonds / Financial Assets at Amortized CostDocument1 pageInvestment in Bonds / Financial Assets at Amortized CostSteffanie Olivar0% (1)

- Quiz On InvestmentDocument3 pagesQuiz On InvestmentDan Andrei BongoNo ratings yet

- Framework of AccountingDocument11 pagesFramework of AccountingAngelica ManaoisNo ratings yet

- Auditibg Problems Purchase CommitmentDocument1 pageAuditibg Problems Purchase Commitmentnivea gumayagay0% (1)

- A6 Share 221 eDocument2 pagesA6 Share 221 eNika Ella SabinoNo ratings yet

- FAR First Pre BoardDocument18 pagesFAR First Pre BoardKIM RAGANo ratings yet

- Final Exam Fin 2Document3 pagesFinal Exam Fin 2ma. veronica guisihanNo ratings yet

- Business Combination Q4Document2 pagesBusiness Combination Q4Sweet EmmeNo ratings yet

- ExamDocument7 pagesExamKristen WalshNo ratings yet

- Examination About Investment 7Document3 pagesExamination About Investment 7BLACKPINKLisaRoseJisooJennieNo ratings yet

- Intermediate Accounting Prac Mock ExamsDocument72 pagesIntermediate Accounting Prac Mock ExamsIris Claire ClementeNo ratings yet

- Cash BasisDocument4 pagesCash BasisMark DiezNo ratings yet

- AUDProb TEST BANKDocument28 pagesAUDProb TEST BANKFrancine HollerNo ratings yet

- 1909 Gross Profit and Retail MethodDocument3 pages1909 Gross Profit and Retail MethodCykee Hanna Quizo Lumongsod50% (4)

- Standard Costs and Variance Analysis ERDocument19 pagesStandard Costs and Variance Analysis ERElyana SulayNo ratings yet

- 2nd Year QuestionnairesDocument7 pages2nd Year QuestionnaireswivadaNo ratings yet

- Global CompanyDocument1 pageGlobal Companydagohoy kennethNo ratings yet

- FormulaDocument10 pagesFormulaAngel Alejo Acoba100% (1)

- 5 - Discussion - Standard Costing and Variance AnalysisDocument1 page5 - Discussion - Standard Costing and Variance AnalysisCharles TuazonNo ratings yet

- Cash and Cash Equivalents Audit of Papskie CompanyDocument3 pagesCash and Cash Equivalents Audit of Papskie CompanyNicole ReyesNo ratings yet

- Inventory recognition and measurementDocument33 pagesInventory recognition and measurementAJHDALDKJA0% (1)

- Receivable Practice Problem 1Document2 pagesReceivable Practice Problem 1ayeeeNo ratings yet

- Chapter 3 - Seat Work - Assignment #3 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDocument5 pagesChapter 3 - Seat Work - Assignment #3 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDonise Ronadel SantosNo ratings yet

- Short-Term Budgeting: (Problem 1)Document18 pagesShort-Term Budgeting: (Problem 1)princess bubblegumNo ratings yet

- Intermediate Accounting - MidtermsDocument9 pagesIntermediate Accounting - MidtermsKim Cristian MaañoNo ratings yet

- Far 6660Document2 pagesFar 6660Glessy Anne Marie FernandezNo ratings yet

- Acct. 162 - EPS, BVPS, DividendsDocument5 pagesAcct. 162 - EPS, BVPS, DividendsAngelli LamiqueNo ratings yet

- LIABILITIESDocument5 pagesLIABILITIESKate FernandezNo ratings yet

- Janet Wooster Owns A Retail Store That Sells New andDocument2 pagesJanet Wooster Owns A Retail Store That Sells New andAmit PandeyNo ratings yet

- Pract 1 - Exam2Document2 pagesPract 1 - Exam2Sharmaine Rivera MiguelNo ratings yet

- Depreciation Methods and CalculationsDocument5 pagesDepreciation Methods and CalculationsAvox EverdeenNo ratings yet

- Cash Receivables Financial Reporting GuideDocument19 pagesCash Receivables Financial Reporting GuideMiguel Angelo JoseNo ratings yet

- Liabilities QuizDocument13 pagesLiabilities QuizRizia Feh Eustaquio100% (1)

- Tangy Candy Company premium plan journal entries and financial statement analysisDocument4 pagesTangy Candy Company premium plan journal entries and financial statement analysisAlexis KingNo ratings yet

- Cost of Land and Buildings Purchased by Esculent CoDocument7 pagesCost of Land and Buildings Purchased by Esculent Coprey kunNo ratings yet

- Notes ReceivableDocument4 pagesNotes ReceivableJenny MendozaNo ratings yet

- Faye Faye Corp taxable income 20X2Document1 pageFaye Faye Corp taxable income 20X2Kath LeynesNo ratings yet

- Quiz 5Document7 pagesQuiz 5Arjay CarolinoNo ratings yet

- Investment in Equity Securities 2Document2 pagesInvestment in Equity Securities 2miss independentNo ratings yet

- Quiz - M2.5G POST-TEST May SagotDocument17 pagesQuiz - M2.5G POST-TEST May SagotJimbo ManalastasNo ratings yet

- Far 21Document1 pageFar 21memejaneNo ratings yet

- Allowance For Doubtful Accounts ExerciseDocument9 pagesAllowance For Doubtful Accounts ExerciseDeborah Pineda33% (3)

- St. Peter's College Acctg 22 Auditing Final ExamDocument6 pagesSt. Peter's College Acctg 22 Auditing Final Exammarx marolinaNo ratings yet

- This Study Resource Was Shared Via: Solution 23-2 Answer DDocument5 pagesThis Study Resource Was Shared Via: Solution 23-2 Answer DDummy GoogleNo ratings yet

- Sol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aJenny Joy Alcantara0% (1)

- F3 Sunday TestDocument15 pagesF3 Sunday TestAliRazaSattarNo ratings yet

- Liabs 2Document3 pagesLiabs 2Iohc NedmiNo ratings yet

- 3 ACCT 2AB P. DissolutionDocument6 pages3 ACCT 2AB P. DissolutionMary Angeline LopezNo ratings yet

- Notes and Loans Payable ExercisesDocument3 pagesNotes and Loans Payable ExercisesLovenia M. FerrerNo ratings yet

- Notes Payable and Loans PayableDocument3 pagesNotes Payable and Loans PayableLovenia M. FerrerNo ratings yet

- FR ACCA Test FullDocument16 pagesFR ACCA Test Fullduducchi2308No ratings yet

- Answer Key - M1L2 PDFDocument4 pagesAnswer Key - M1L2 PDFEricka Mher IsletaNo ratings yet

- Financial Instruments CASE STUDIES FRDocument5 pagesFinancial Instruments CASE STUDIES FRDaniel AdegboyeNo ratings yet

- Notes Receivables: 1. Present Value IsDocument4 pagesNotes Receivables: 1. Present Value IsZyrene Kei ReyesNo ratings yet

- CV - FormatDocument2 pagesCV - FormatRafidul IslamNo ratings yet

- Consolidated Financial Statement (Part 1)Document32 pagesConsolidated Financial Statement (Part 1)Ruby Amor DoligosaNo ratings yet

- Capital Markets Senior Vice President in New York City Resume David GrossmanDocument3 pagesCapital Markets Senior Vice President in New York City Resume David GrossmanDavidGrossman3No ratings yet

- BiiserDocument7 pagesBiiserFiras FurkanNo ratings yet

- Options Trading (Advanced) ModuleDocument11 pagesOptions Trading (Advanced) ModuleavinashkakarlaNo ratings yet

- A - Baron v. GalassoDocument97 pagesA - Baron v. GalassorichdebtNo ratings yet

- Am Tool 02 v2.2Document15 pagesAm Tool 02 v2.2Jhimmy Quisocala HerreraNo ratings yet

- Tax Invoice: Your Order SummaryDocument2 pagesTax Invoice: Your Order SummaryDaveNo ratings yet

- RDO TRUST Annual Report 2013-2014Document35 pagesRDO TRUST Annual Report 2013-2014Kannan RamaiahNo ratings yet

- Bar 2015 QuestionsDocument27 pagesBar 2015 QuestionsBrent DagbayNo ratings yet

- Harshad Mehta ScamDocument17 pagesHarshad Mehta ScamRupali Manpreet Rana0% (1)

- Earnest Money AgreementDocument2 pagesEarnest Money AgreementAtty. Jefferson B. YapNo ratings yet

- MWSS V DawayDocument1 pageMWSS V DawayAnonymous B4hcMPjqvNo ratings yet

- Corporate Accounting IMP QuestionsDocument6 pagesCorporate Accounting IMP QuestionsMayank RajeNo ratings yet

- Customers' perception of insuranceDocument48 pagesCustomers' perception of insuranceYogendraNo ratings yet

- TAXATION REVIEW: KEY CONCEPTS AND SITUATIONSDocument113 pagesTAXATION REVIEW: KEY CONCEPTS AND SITUATIONSDaryl Mae Mansay100% (1)

- FIC77LIFE - Bene ChangeDocument6 pagesFIC77LIFE - Bene ChangeMary GeorgeNo ratings yet

- Tax Year 2013-14 (As Per Finance Act 2013) : Tax Card For Staff and Clients OnlyDocument1 pageTax Year 2013-14 (As Per Finance Act 2013) : Tax Card For Staff and Clients OnlyMuhammad sarfrazNo ratings yet

- Yanis Varoufakis - A Letter To My Daughter About The Black Magic of BankingDocument8 pagesYanis Varoufakis - A Letter To My Daughter About The Black Magic of BankingSasko MateskiNo ratings yet

- Chapter 12 AnswersDocument3 pagesChapter 12 AnswersMarisa Vetter100% (1)

- IRRBAM Vol2Document100 pagesIRRBAM Vol2GwenNo ratings yet

- Accounting Mcqs 3Document6 pagesAccounting Mcqs 3Mohd AyazNo ratings yet

- FINMAN 103 Module IIIDocument26 pagesFINMAN 103 Module IIIAlma Teresa NipaNo ratings yet

- Auditing Theory: Completing The AuditDocument10 pagesAuditing Theory: Completing The AuditAljur SalamedaNo ratings yet

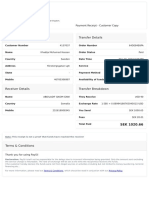

- Sender Details Transfer Details: Payment Receipt - CustomerDocument1 pageSender Details Transfer Details: Payment Receipt - CustomerAbshira Abdi AliNo ratings yet

- A-Level Macroeconomics PLC (AQA)Document11 pagesA-Level Macroeconomics PLC (AQA)Karim El-GawlyNo ratings yet

- EFM2e, CH 04, SlidesDocument16 pagesEFM2e, CH 04, SlidesMaria DevinaNo ratings yet

- SAP Cutover PlanDocument32,767 pagesSAP Cutover PlanMichelle FossNo ratings yet

- A Report On Insurance Industry of NepalDocument7 pagesA Report On Insurance Industry of NepaldeepNo ratings yet

- Account Modification in SAPDocument5 pagesAccount Modification in SAPnetra14520No ratings yet