You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Upload A Document 1. Click Upload 2. Select File 3. Wait. File Uploaded.Document1 pageUpload A Document 1. Click Upload 2. Select File 3. Wait. File Uploaded.Anantdeep Singh PuriNo ratings yet

- Litreture ReviewDocument17 pagesLitreture Review8866708515No ratings yet

- Stocks Shares Securities Stock Exchange: Notional ValuesDocument1 pageStocks Shares Securities Stock Exchange: Notional ValuesAnantdeep Singh PuriNo ratings yet

- Exploring The Volatility of Stock Markets: Indian ExperienceDocument19 pagesExploring The Volatility of Stock Markets: Indian ExperienceAnantdeep Singh PuriNo ratings yet

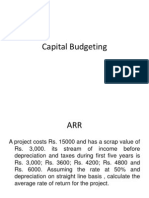

- Capital Budgeting ProblemsDocument8 pagesCapital Budgeting ProblemsAnantdeep Singh Puri100% (1)

- Product: The Marketing Mix Is A Business Tool Used inDocument2 pagesProduct: The Marketing Mix Is A Business Tool Used inAnantdeep Singh PuriNo ratings yet

- Banking: For Other Uses, See - "Banker" and "Bankers" Redirect Here. For Other Uses, SeeDocument20 pagesBanking: For Other Uses, See - "Banker" and "Bankers" Redirect Here. For Other Uses, SeeAnantdeep Singh PuriNo ratings yet

- Matty Vs ChatGPTDocument17 pagesMatty Vs ChatGPTfqwaszx43No ratings yet

- President Uhuru Kenyatta's Speech During The National Youth Service Recruits at National Youth Service College, GilgilDocument3 pagesPresident Uhuru Kenyatta's Speech During The National Youth Service Recruits at National Youth Service College, GilgilState House KenyaNo ratings yet

- Human RightsDocument200 pagesHuman RightsPat EspinozaNo ratings yet

- IB PPT On IMFDocument22 pagesIB PPT On IMFAtul YadavNo ratings yet

- Fuerte Vs EstomoDocument2 pagesFuerte Vs EstomoBea Vanessa AbellaNo ratings yet

- Fernandez v. Dimagiba Mercado v. Santos FactsDocument13 pagesFernandez v. Dimagiba Mercado v. Santos FactsTajNo ratings yet

- Comments On Draft Rules As Prevention of Cruelty To Animals (Animal Husbandry Practices and Procedures) Rules, 2021 by Sukanya BerwalDocument24 pagesComments On Draft Rules As Prevention of Cruelty To Animals (Animal Husbandry Practices and Procedures) Rules, 2021 by Sukanya BerwalNaresh KadyanNo ratings yet

- Roy v. Herbosa 2017Document1 pageRoy v. Herbosa 2017kimoymoy7No ratings yet

- Gad Workplan 2018Document8 pagesGad Workplan 2018Riza GaquitNo ratings yet

- Padmanabha Swamy Temple: Facts of The CaseDocument4 pagesPadmanabha Swamy Temple: Facts of The CaseKartikey PurohitNo ratings yet

- Practicum V Project (Admin Law) - Jerwin C. Tiamson-OldDocument5 pagesPracticum V Project (Admin Law) - Jerwin C. Tiamson-OldJerwin TiamsonNo ratings yet

- Chemline 784 32Document4 pagesChemline 784 32Abdul SabirNo ratings yet

- 45 PHIL Vs CHINADocument3 pages45 PHIL Vs CHINAdextlabNo ratings yet

- That A Writ Petition Was Filed by The Respondents/writ-Petitioners ClaimingDocument4 pagesThat A Writ Petition Was Filed by The Respondents/writ-Petitioners ClaimingShubham Jain ModiNo ratings yet

- RPH ResearchDocument10 pagesRPH ResearchMr. DADANo ratings yet

- Professional Teachers 09-2018 Room Assignment - Laoag (Secondary)Document44 pagesProfessional Teachers 09-2018 Room Assignment - Laoag (Secondary)PRC BaguioNo ratings yet

- Current Electricity: One Mark Questions With AnswersDocument35 pagesCurrent Electricity: One Mark Questions With AnswersMiftha Mallauling100% (1)

- Garasi Drift Rate CardDocument17 pagesGarasi Drift Rate CardDesi Rahmi DianaNo ratings yet

- Gurpal Singh Ahluwalia, J.: Equiv Alent Citation: 2019 (3) MPLJ62Document13 pagesGurpal Singh Ahluwalia, J.: Equiv Alent Citation: 2019 (3) MPLJ62TSA LEGALNo ratings yet

- Test Bank For Advanced Accounting, 1st Edition HamlenDocument43 pagesTest Bank For Advanced Accounting, 1st Edition HamlenJanine NazNo ratings yet

- People vs. PosadaDocument26 pagesPeople vs. PosadaErwin SabornidoNo ratings yet

- AMH 2020 Worksheet Chapter 20Document5 pagesAMH 2020 Worksheet Chapter 20Imani AlvaradoNo ratings yet

- Fla100h Fireset Completion CertDocument1 pageFla100h Fireset Completion CertsureshNo ratings yet

- Inigo - Rule 117 Motion To QuashDocument19 pagesInigo - Rule 117 Motion To QuashRobert Manto100% (1)

- Cambridge International AS & A Level: PHYSICS 9702/33Document8 pagesCambridge International AS & A Level: PHYSICS 9702/33Jean-Michel RatnaNo ratings yet

- DARAB v. Lubrica: Prayer For The Issuance of Temporary Restraining Order/Preliminary InjunctionDocument3 pagesDARAB v. Lubrica: Prayer For The Issuance of Temporary Restraining Order/Preliminary InjunctionSGOD HRDNo ratings yet

- 2018 Grade 12 RE NotesDocument67 pages2018 Grade 12 RE NotesKalenga AlexNo ratings yet

- Camarines - Norte - Electric - Cooperative - Inc. - v.20210424-14-gx8zw6Document13 pagesCamarines - Norte - Electric - Cooperative - Inc. - v.20210424-14-gx8zw6Danny QuioyoNo ratings yet

- Approved Training Organisation Certificate Training Course ApprovalDocument2 pagesApproved Training Organisation Certificate Training Course ApprovalAhmed Oumar KadergueliNo ratings yet

- Dokumen EksporDocument4 pagesDokumen EksporDicky AditiyaNo ratings yet