You might also like

- Milton Friedman 50 Years Later EbookDocument147 pagesMilton Friedman 50 Years Later EbookVitor Hazin100% (2)

- Q1 2022 - Real Estate Knowledge Report - VNDocument45 pagesQ1 2022 - Real Estate Knowledge Report - VNHoàng MinhNo ratings yet

- TESCO 2020.2 报告 PDFDocument176 pagesTESCO 2020.2 报告 PDFHongxian JiNo ratings yet

- July Net Profit Improved: FlashnoteDocument5 pagesJuly Net Profit Improved: FlashnoteSergio FibonacciNo ratings yet

- TCB 1Q23 ResultsDocument4 pagesTCB 1Q23 ResultsLinh NguyenNo ratings yet

- Vinhomes 1H20 Earnings PresentationDocument32 pagesVinhomes 1H20 Earnings PresentationPhan DuyNo ratings yet

- Vinhomes JSC: Maintaining Leadership PositionDocument10 pagesVinhomes JSC: Maintaining Leadership PositionTam NguyenNo ratings yet

- Id 23062020 PDFDocument11 pagesId 23062020 PDFbala gamerNo ratings yet

- Viet Capital CTD@VN CTD-20221130-MPDocument13 pagesViet Capital CTD@VN CTD-20221130-MPĐức Anh NguyễnNo ratings yet

- Third Quarter Results: Philippine Stock Exchange Ticker: CHPDocument8 pagesThird Quarter Results: Philippine Stock Exchange Ticker: CHPJep TangNo ratings yet

- UNTR - Strong 1Q17 But in LineDocument3 pagesUNTR - Strong 1Q17 But in LineCut Farisa MachmudNo ratings yet

- STB 2023 AgmDocument4 pagesSTB 2023 AgmLinh NguyenNo ratings yet

- VJC AviationDocument9 pagesVJC AviationTony ZhangNo ratings yet

- A Challenging Outlook - Cut To Hold: Company FocusDocument14 pagesA Challenging Outlook - Cut To Hold: Company FocusDuc BuiNo ratings yet

- CTD-20211125-MP VietcapDocument15 pagesCTD-20211125-MP VietcapĐức Anh NguyễnNo ratings yet

- ICICI Prudential Life - 2QFY20 - HDFC Sec-201910231337147517634Document15 pagesICICI Prudential Life - 2QFY20 - HDFC Sec-201910231337147517634sandeeptirukotiNo ratings yet

- ICICI Direct Balkrishna IndustriesDocument9 pagesICICI Direct Balkrishna Industriesshankar alkotiNo ratings yet

- Prabhudas DmartDocument8 pagesPrabhudas DmartGOUTAMNo ratings yet

- Centel Oppday 2q2021Document43 pagesCentel Oppday 2q2021Teravut SuwansawaipholNo ratings yet

- Solid Growth Momentum Maintains in 2H21: Bamboo Capital JSC (BCG) UpdateDocument15 pagesSolid Growth Momentum Maintains in 2H21: Bamboo Capital JSC (BCG) UpdateHoàng Tuấn AnhNo ratings yet

- Sun Pharma - EQuity Reserch ReportDocument6 pagesSun Pharma - EQuity Reserch ReportsmitNo ratings yet

- Earnings Release 3Q22 1Document12 pagesEarnings Release 3Q22 1Yousif Zaki 3No ratings yet

- Japfa Comfeed Indonesia: Equity ResearchDocument7 pagesJapfa Comfeed Indonesia: Equity Researchroy95121No ratings yet

- Flash - HM. Sampoerna: 2Q20 Volume and Key Forward-Looking StatementDocument3 pagesFlash - HM. Sampoerna: 2Q20 Volume and Key Forward-Looking Statementjnn sNo ratings yet

- Blue Star (BLSTR In) 2QFY20 Result Update - RsecDocument9 pagesBlue Star (BLSTR In) 2QFY20 Result Update - RsecHardik ShahNo ratings yet

- Chap14: Regulator of Central BankDocument92 pagesChap14: Regulator of Central BankShifat SardarNo ratings yet

- 1692674556155-VNGMD Updated Hold MAS 20230826EN Ed SDocument6 pages1692674556155-VNGMD Updated Hold MAS 20230826EN Ed Snguyennauy25042003No ratings yet

- Investor Digest: Equity Research - 28 March 2019Document9 pagesInvestor Digest: Equity Research - 28 March 2019Rising PKN STANNo ratings yet

- Please Click On The Link For The Report:: cm09MjgDocument2 pagesPlease Click On The Link For The Report:: cm09Mjgneil5mNo ratings yet

- Ultratech Cement Limited: Outlook Remains ChallengingDocument5 pagesUltratech Cement Limited: Outlook Remains ChallengingamitNo ratings yet

- PNJ Update 20201207Document7 pagesPNJ Update 20201207Khoa PhamNo ratings yet

- SHri FY21Document25 pagesSHri FY2153crx1fnocNo ratings yet

- Ciptadana Results Update 1H22 UNTR 29 Jul 2022 Reiterate Buy UpgradeDocument7 pagesCiptadana Results Update 1H22 UNTR 29 Jul 2022 Reiterate Buy UpgradeOnggo iMamNo ratings yet

- Infosys 140422 MotiDocument10 pagesInfosys 140422 MotiGrace StylesNo ratings yet

- Mondo TV InformeDocument12 pagesMondo TV InformeAntonio Perez CastilloNo ratings yet

- DNL 1Q21 Earnings Grow 35% Y/y, Ahead of Estimates: D&L Industries, IncDocument9 pagesDNL 1Q21 Earnings Grow 35% Y/y, Ahead of Estimates: D&L Industries, IncJajahinaNo ratings yet

- Cash Market Transaction Survey 2020: April 2022Document14 pagesCash Market Transaction Survey 2020: April 2022mtcyhcNo ratings yet

- DRC 20230717 EarningsFlashDocument5 pagesDRC 20230717 EarningsFlashnguyenlonghaihcmutNo ratings yet

- JS Com. Bank For Foreign Trade of Vietnam: Hold On The ThroneDocument7 pagesJS Com. Bank For Foreign Trade of Vietnam: Hold On The ThroneDinh Minh TriNo ratings yet

- Dialog Group: Company ReportDocument5 pagesDialog Group: Company ReportBrian StanleyNo ratings yet

- VSC Flash Note June 2020Document5 pagesVSC Flash Note June 2020Van Luong LuuNo ratings yet

- Trent - Q4FY22 Result - DAMDocument6 pagesTrent - Q4FY22 Result - DAMRajiv BharatiNo ratings yet

- DBS Group Holdings LTD: Allowances Dent Record Operating ResultDocument7 pagesDBS Group Holdings LTD: Allowances Dent Record Operating ResultCalebNo ratings yet

- 1683626985785-EN CTD Update 2Q23 Ed SDocument7 pages1683626985785-EN CTD Update 2Q23 Ed Snguyennauy25042003No ratings yet

- Gemadept Corporation: Maintain The RecoveryDocument7 pagesGemadept Corporation: Maintain The RecoveryDinh Minh TriNo ratings yet

- Environmental Support: BYD (1211 HK)Document9 pagesEnvironmental Support: BYD (1211 HK)Man Ho LiNo ratings yet

- Investor Digest: Equity Research - 25 November 2020Document18 pagesInvestor Digest: Equity Research - 25 November 2020Ciprut 2205No ratings yet

- Ssi Securities Corporation 1Q2020 Performance Updates: April 2020Document20 pagesSsi Securities Corporation 1Q2020 Performance Updates: April 2020Hoàng HiệpNo ratings yet

- Emlak Konut REIC: Price Target RevisionDocument6 pagesEmlak Konut REIC: Price Target RevisionCbpNo ratings yet

- Hero Motocorp: (Herhon)Document9 pagesHero Motocorp: (Herhon)ayushNo ratings yet

- BUY TP: IDR1,700: Bank Tabungan NegaraDocument6 pagesBUY TP: IDR1,700: Bank Tabungan NegaraAl VengerNo ratings yet

- HAG-2Q23 BriefDocument3 pagesHAG-2Q23 Briefnguyennauy25042003No ratings yet

- Maruti Suzuki (MSIL IN) : Q1FY20 Result UpdateDocument6 pagesMaruti Suzuki (MSIL IN) : Q1FY20 Result UpdateHitesh JainNo ratings yet

- ITC Limited: Wait For Cigarette Double Digit Ebit Growth Get ElongatedDocument8 pagesITC Limited: Wait For Cigarette Double Digit Ebit Growth Get ElongatedAshis Kumar MuduliNo ratings yet

- Bank Rakyat Indonesia: 4Q20 Review: Better-Than-Expected EarningsDocument7 pagesBank Rakyat Indonesia: 4Q20 Review: Better-Than-Expected EarningsPutri CandraNo ratings yet

- Nickel StudyDocument7 pagesNickel StudyILSEN N. DAETNo ratings yet

- IIFL - Power Grid Corporation of India Ltd. (PGCIL) - Exploring New Juncture! (1QFY22 RU & Analyst Meet Update) (BUY)Document11 pagesIIFL - Power Grid Corporation of India Ltd. (PGCIL) - Exploring New Juncture! (1QFY22 RU & Analyst Meet Update) (BUY)jitendra76No ratings yet

- London Sumatra Indonesia TBK: Still Positive But Below ExpectationDocument7 pagesLondon Sumatra Indonesia TBK: Still Positive But Below ExpectationHamba AllahNo ratings yet

- Infosys Limited: Financial HighlightsDocument3 pagesInfosys Limited: Financial HighlightsJayant KiniNo ratings yet

- Axia Corporation FY21 Earnings UpdateDocument3 pagesAxia Corporation FY21 Earnings UpdateMalcolm ChitenderuNo ratings yet

- World Bank East Asia and Pacific Economic Update, Spring 2022: Risks and OpportunitiesFrom EverandWorld Bank East Asia and Pacific Economic Update, Spring 2022: Risks and OpportunitiesNo ratings yet

- Iron Ore Commodity Research: BI Commodities, Global DashboardDocument9 pagesIron Ore Commodity Research: BI Commodities, Global DashboardVan Luong LuuNo ratings yet

- Bloomberg: Vale Output Guidance Misses Estimates in Boost To Iron PriceDocument2 pagesBloomberg: Vale Output Guidance Misses Estimates in Boost To Iron PriceVan Luong LuuNo ratings yet

- Vale: Itabira Ramifications: Andrew Cosgrove BI Steel Raw Material Suppliers, Global DashboardDocument2 pagesVale: Itabira Ramifications: Andrew Cosgrove BI Steel Raw Material Suppliers, Global DashboardVan Luong LuuNo ratings yet

- Bloomberg: Vale Trims Full-Year Iron Ore Production Outlook Capital Spending To Rise Next YearDocument1 pageBloomberg: Vale Trims Full-Year Iron Ore Production Outlook Capital Spending To Rise Next YearVan Luong LuuNo ratings yet

- China's Iron Ore Output To Rise in JuneDocument2 pagesChina's Iron Ore Output To Rise in JuneVan Luong LuuNo ratings yet

- Iron Ore Holds Above As ValeDocument1 pageIron Ore Holds Above As ValeVan Luong LuuNo ratings yet

- Iron Ore Surges As Chinas SteeDocument1 pageIron Ore Surges As Chinas SteeVan Luong LuuNo ratings yet

- VSC Flash Note June 2020Document5 pagesVSC Flash Note June 2020Van Luong LuuNo ratings yet

- Factories of The FutureDocument3 pagesFactories of The FutureKonstantina DumitruNo ratings yet

- Chapter 6 Incremental AnalysisDocument28 pagesChapter 6 Incremental AnalysisMaria JosefaNo ratings yet

- Kayitesi Claudine Final ThesisDocument90 pagesKayitesi Claudine Final ThesisAlfonso Joel GonzalesNo ratings yet

- Nefas Silk Poly Technic College: Learning GuideDocument43 pagesNefas Silk Poly Technic College: Learning GuideNigussie BerhanuNo ratings yet

- KSB LCC MDocument126 pagesKSB LCC MAlexander Alonso FernándezNo ratings yet

- Chapter 2: Demand & SupplyDocument4 pagesChapter 2: Demand & SupplyRujean Salar AltejarNo ratings yet

- Accounting Exams - 1Document2 pagesAccounting Exams - 1MachelMDotAlexanderNo ratings yet

- Lot Size Price 1-499 500-699 700-999 1000-2499 2500 and AboveDocument2 pagesLot Size Price 1-499 500-699 700-999 1000-2499 2500 and AboveHatim Kasara WalaNo ratings yet

- Business Studies Books Shree Radhey Publication Business Studies (Hinglish) Part-A Foundations of BusinessDocument71 pagesBusiness Studies Books Shree Radhey Publication Business Studies (Hinglish) Part-A Foundations of BusinessVishal DhakarNo ratings yet

- (Reaffirmed!2011) !Document10 pages(Reaffirmed!2011) !Devesh Kumar PandeyNo ratings yet

- 37 Practice+Questions+ (Working+Capital+Management)Document4 pages37 Practice+Questions+ (Working+Capital+Management)bahaa madiNo ratings yet

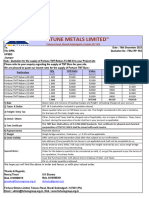

- "Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301Document1 page"Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301S K SharmaNo ratings yet

- 11 & 12 Economics Split-UpDocument9 pages11 & 12 Economics Split-UpMadhuryaNo ratings yet

- Vikas Provisional ComputationDocument6 pagesVikas Provisional ComputationAmit TyagiNo ratings yet

- 1) Week 2 - Statement of Financial Position v3 - TaggedDocument51 pages1) Week 2 - Statement of Financial Position v3 - TaggedNabilNo ratings yet

- APISWA Report 280923 DigitalDocument31 pagesAPISWA Report 280923 DigitaldashaNo ratings yet

- Eefc Account1Document15 pagesEefc Account1navneet bagriNo ratings yet

- Dimensioni Tenute SKF: SKF Fork Seals SizesDocument2 pagesDimensioni Tenute SKF: SKF Fork Seals SizesGaetano GiordanoNo ratings yet

- Intertrade Automation Solutions: - 24143355 27AFRPR5889L1Z5 State: Msme NoDocument2 pagesIntertrade Automation Solutions: - 24143355 27AFRPR5889L1Z5 State: Msme NoAnsariMohdIrfanNo ratings yet

- Flipkart Labels 27 Jun 2021 06 53Document1 pageFlipkart Labels 27 Jun 2021 06 53h4ckerNo ratings yet

- The Profitable Producer Rate SheetDocument4 pagesThe Profitable Producer Rate SheetAnonymous fH6s0ZbhMNo ratings yet

- San Mateo Municipal College: Accounting Information System Midterms Activity Understanding A Relational DatabaseDocument2 pagesSan Mateo Municipal College: Accounting Information System Midterms Activity Understanding A Relational Database버니 모지코No ratings yet

- VARUN ProjectDocument58 pagesVARUN ProjectYASHWANTH PATIL G JNo ratings yet

- Agencies That Facilitate International FlowsDocument2 pagesAgencies That Facilitate International FlowsLê Thị Ngọc DiễmNo ratings yet

- Sodium Sulphate Manufacturing Feasibility Study Project Proposal Business Plan in Ethiopia Pdf. - Haqiqa Investment Consultant in EthiopiaDocument1 pageSodium Sulphate Manufacturing Feasibility Study Project Proposal Business Plan in Ethiopia Pdf. - Haqiqa Investment Consultant in EthiopiaSulemanNo ratings yet

- Debit Cards in VietnamDocument8 pagesDebit Cards in VietnamVinh NguyenNo ratings yet

- Part - 2 - Dashboard - Foreign Exchange FluctuationsDocument5 pagesPart - 2 - Dashboard - Foreign Exchange FluctuationsJaquelyn JacquesNo ratings yet

- Property Relations TableDocument7 pagesProperty Relations TableEvita IgotNo ratings yet

- Digital Marketing Assignment 2Document15 pagesDigital Marketing Assignment 2Bright MuzaNo ratings yet