You might also like

- General ExceptionsDocument11 pagesGeneral ExceptionsHarsh RanaNo ratings yet

- Criminal Law Project On Topic: "Mischief"Document12 pagesCriminal Law Project On Topic: "Mischief"Satwant Singh100% (1)

- LCAR Unit 13 - The Real Estate Business - 14th EditionDocument63 pagesLCAR Unit 13 - The Real Estate Business - 14th EditionTom BlefkoNo ratings yet

- Transfer of Property PrnjalDocument20 pagesTransfer of Property PrnjalShashiRai100% (1)

- Movable & Immovable Property Under Indian LawDocument7 pagesMovable & Immovable Property Under Indian LawSoumya Srijan DasguptaNo ratings yet

- National Law University Odisha: Transfer of Property ActDocument33 pagesNational Law University Odisha: Transfer of Property ActIshwar MeenaNo ratings yet

- Concept and Meaning of Property by Roohika SehgalDocument13 pagesConcept and Meaning of Property by Roohika SehgalRoohika SehgalNo ratings yet

- I.P.R ProjectDocument15 pagesI.P.R ProjectSadhvi SinghNo ratings yet

- GiftDocument29 pagesGiftAnkitTiwari100% (1)

- 1367 Family Law ProjectDocument14 pages1367 Family Law ProjectSuvigya TripathiNo ratings yet

- Project of Environmental LawDocument24 pagesProject of Environmental LawRahul GuptaNo ratings yet

- Jamia Millia Islamia: Project TitleDocument19 pagesJamia Millia Islamia: Project TitlePranavNo ratings yet

- Critical Study on Land Reforms in IndiaDocument14 pagesCritical Study on Land Reforms in Indiagaurav singhNo ratings yet

- Property Law PRODocument14 pagesProperty Law PROgowthamNo ratings yet

- Hindu AssignmentDocument23 pagesHindu Assignmentamaan ahmedNo ratings yet

- Citizenship Methods in IndiaDocument5 pagesCitizenship Methods in IndiaRiya RoyNo ratings yet

- Constitutional Provisions and Legislations For Empowering The Weaker SectionsDocument10 pagesConstitutional Provisions and Legislations For Empowering The Weaker Sectionssarnat100% (1)

- Delegated legislation in India explainedDocument22 pagesDelegated legislation in India explainedAditya RautNo ratings yet

- Transfer of PropertyDocument11 pagesTransfer of PropertyShubham Githala100% (1)

- Advisory Jurisdiction of the Supreme CourtDocument17 pagesAdvisory Jurisdiction of the Supreme CourtAshish RanjanNo ratings yet

- Dr. Ram Manohar Lohiya National Law University, LucknowDocument17 pagesDr. Ram Manohar Lohiya National Law University, LucknowAkAsh prAkhAr vErmANo ratings yet

- Property Law Final DraftDocument18 pagesProperty Law Final DraftPratik ShendeNo ratings yet

- 19LLB072 - Transfer of Property - IvDocument25 pages19LLB072 - Transfer of Property - IvMeghana Rani pNo ratings yet

- Hindu Laws LakshayDocument63 pagesHindu Laws Lakshaymaira mujawarNo ratings yet

- Research Assignment: Topic: Gift Under Muslim LawDocument23 pagesResearch Assignment: Topic: Gift Under Muslim LawfaarehaNo ratings yet

- Section 34Document5 pagesSection 34Zeesahn100% (1)

- The National Law Institute University Bhopal-1Document21 pagesThe National Law Institute University Bhopal-1Vikas Jadhav100% (1)

- Viability of Class Division While Accessing Tax - An Appraisal Dr. Ram Manohar Lohia National Law UniversityDocument16 pagesViability of Class Division While Accessing Tax - An Appraisal Dr. Ram Manohar Lohia National Law UniversityHimanshumalikNo ratings yet

- Immovable Property PDFDocument6 pagesImmovable Property PDFmanoj ktm100% (1)

- The Indian Penal Code 5Document21 pagesThe Indian Penal Code 5Mandira PrakashNo ratings yet

- Analysis of Partial Restraint On Transfer of PropertyDocument14 pagesAnalysis of Partial Restraint On Transfer of PropertyPayoja GandhiNo ratings yet

- Res Judicata Under Civil Procedure Code, 1908Document15 pagesRes Judicata Under Civil Procedure Code, 1908MR VIDEOSNo ratings yet

- Interpretation of Statutes AssignmentDocument32 pagesInterpretation of Statutes AssignmentHimanish ChakrabortyNo ratings yet

- Ndore Nstitute of Law (Affiliated To D.A.V.V. & BCI) : Asst. Prof. Mr. Shubham SolankiDocument18 pagesNdore Nstitute of Law (Affiliated To D.A.V.V. & BCI) : Asst. Prof. Mr. Shubham SolankiSwatiVermaNo ratings yet

- Rights of Women in Coparcenary PropertyDocument18 pagesRights of Women in Coparcenary Propertyashish kumarNo ratings yet

- CRPC PROJECT: CRIMINAL COURTS IN INDIADocument10 pagesCRPC PROJECT: CRIMINAL COURTS IN INDIAAditya DassaurNo ratings yet

- PILDocument34 pagesPILMahebub GhanteNo ratings yet

- Law and Poverty Justice Is Expensive, Evasive Dream For Poor Legal FrameworkDocument25 pagesLaw and Poverty Justice Is Expensive, Evasive Dream For Poor Legal FrameworkMARLENE RANDIFIEDNo ratings yet

- Types of Punishment Under IPCDocument19 pagesTypes of Punishment Under IPCAdarsh GuptaNo ratings yet

- Interpretation of StatuteDocument15 pagesInterpretation of Statutevijendra sableNo ratings yet

- Submitted by Rishabh Sen Gupta UID: SM0116036: The Unnatural' in Section 377 of The Indian Penal CodeDocument25 pagesSubmitted by Rishabh Sen Gupta UID: SM0116036: The Unnatural' in Section 377 of The Indian Penal CodeRishabh Sen GuptaNo ratings yet

- Guardianship Under Muslim Family LawDocument44 pagesGuardianship Under Muslim Family LawTaiyabaNo ratings yet

- The Evolution of Coparcenary Rights in Hindu LawDocument10 pagesThe Evolution of Coparcenary Rights in Hindu LawLoki HangalNo ratings yet

- Constitutional Law-I Assignment Semester 3Document16 pagesConstitutional Law-I Assignment Semester 3AnonymousNo ratings yet

- List of Abbreviations: IT Information TechnologyDocument19 pagesList of Abbreviations: IT Information TechnologyaishwaryaNo ratings yet

- International and Municipal LawDocument18 pagesInternational and Municipal LawAman RajNo ratings yet

- Ipc 2Document25 pagesIpc 2Nasir AlamNo ratings yet

- Condition Restraining Alienation under TPADocument9 pagesCondition Restraining Alienation under TPADaniyal SirajNo ratings yet

- Vested Interest: Section 19 of Transfer of Property Act Deals With Vested Interests It Deals With SituationsDocument13 pagesVested Interest: Section 19 of Transfer of Property Act Deals With Vested Interests It Deals With SituationssandliNo ratings yet

- Privity of ContractDocument19 pagesPrivity of ContractBharti MishraNo ratings yet

- Gift Under Muslim LawDocument17 pagesGift Under Muslim LawAmit Srivastava0% (1)

- Sports and ConstitutionDocument24 pagesSports and Constitutionchotu singhNo ratings yet

- The Trade Marks Act, 1999Document13 pagesThe Trade Marks Act, 1999karthik kpNo ratings yet

- Project On Sources of International Law - Simran Khurana (6061)Document13 pagesProject On Sources of International Law - Simran Khurana (6061)Simran Kaur KhuranaNo ratings yet

- Amity UniversityDocument10 pagesAmity Universityvipin jaiswalNo ratings yet

- Succession Act ExplainedDocument14 pagesSuccession Act Explainedस्वर्णीम घलेNo ratings yet

- Common Intention' and Common Object - PDFDocument3 pagesCommon Intention' and Common Object - PDFabc100% (1)

- 382what Is The Order of Succession Among Agnates and Cognates As Per Indian LawDocument3 pages382what Is The Order of Succession Among Agnates and Cognates As Per Indian LawAman RoyNo ratings yet

- Interpretation of StatuteDocument11 pagesInterpretation of StatuteAmit RawlaniNo ratings yet

- T J U CPC: Project Submitted ToDocument19 pagesT J U CPC: Project Submitted ToAnkit Singh ChauhanNo ratings yet

- Section 3 Movable and Immovable PropertyDocument15 pagesSection 3 Movable and Immovable PropertySatwant SinghNo ratings yet

- Property Law Exam NotesDocument30 pagesProperty Law Exam NotesRitesh AroraNo ratings yet

- Markets Around Us.: Pupils Teacher Roll No. 269 Subject-Social StudiesDocument14 pagesMarkets Around Us.: Pupils Teacher Roll No. 269 Subject-Social StudiesSatwant Singh100% (1)

- Review of Masks for Airborne ProtectionDocument46 pagesReview of Masks for Airborne ProtectionSatwant SinghNo ratings yet

- Football Physical TaskDocument7 pagesFootball Physical TaskSatwant SinghNo ratings yet

- SUBMITTED TO: MR. Ajitabh Mishra SUBMITTED BY: Navjot Singh 15162 B.a.ll.b (B)Document23 pagesSUBMITTED TO: MR. Ajitabh Mishra SUBMITTED BY: Navjot Singh 15162 B.a.ll.b (B)Satwant SinghNo ratings yet

- vArUn CPC sEmEsTeR-8Document17 pagesvArUn CPC sEmEsTeR-8Satwant SinghNo ratings yet

- Criminology, Penology and VictimologyDocument15 pagesCriminology, Penology and VictimologySatwant SinghNo ratings yet

- Intellectual Property Laws Project On The Topic: Submitted ToDocument12 pagesIntellectual Property Laws Project On The Topic: Submitted ToSatwant SinghNo ratings yet

- Synapses HistologyDocument6 pagesSynapses HistologySatwant SinghNo ratings yet

- E CommereceDocument15 pagesE CommereceSatwant SinghNo ratings yet

- Courts Which May Execute DecreesDocument8 pagesCourts Which May Execute DecreesSatwant SinghNo ratings yet

- Nerve Cells: Structure and FunctionDocument5 pagesNerve Cells: Structure and FunctionSatwant SinghNo ratings yet

- ILO AND LABOUR LAW: Sexual Harassment at WorkplaceDocument21 pagesILO AND LABOUR LAW: Sexual Harassment at WorkplaceSatwant SinghNo ratings yet

- Section 151Document9 pagesSection 151Satwant SinghNo ratings yet

- E CommereceDocument15 pagesE CommereceSatwant SinghNo ratings yet

- CPC Semester 8Document20 pagesCPC Semester 8Ankit GargNo ratings yet

- CPC Semester 8Document20 pagesCPC Semester 8Ankit GargNo ratings yet

- DocumentDocument6 pagesDocumentSatwant SinghNo ratings yet

- Confession Relevancy During InvestigationDocument34 pagesConfession Relevancy During InvestigationSatwant SinghNo ratings yet

- University Institute of Legal Studies: Project Report On Topic:-Confession and Evidentiary Value (Section 24-30)Document45 pagesUniversity Institute of Legal Studies: Project Report On Topic:-Confession and Evidentiary Value (Section 24-30)RajivSmith100% (1)

- Joinder, Non Joinder and Mis JoinderDocument8 pagesJoinder, Non Joinder and Mis JoinderParnami KrishnaNo ratings yet

- CPC PPT 8th SemDocument15 pagesCPC PPT 8th SemSatwant SinghNo ratings yet

- University Institute of Legal Studies: Project Report On Topic:-Confession and Evidentiary Value (Section 24-30)Document45 pagesUniversity Institute of Legal Studies: Project Report On Topic:-Confession and Evidentiary Value (Section 24-30)RajivSmith100% (1)

- Confessions and Admissions Under Indian Evidence ActDocument9 pagesConfessions and Admissions Under Indian Evidence ActSatwant SinghNo ratings yet

- Courts' Inherent Power to Achieve JusticeDocument9 pagesCourts' Inherent Power to Achieve JusticeSatwant SinghNo ratings yet

- CH 4Document24 pagesCH 4Yosef KetemaNo ratings yet

- Diversified Credit v. Rosado 26 SCRA 470Document2 pagesDiversified Credit v. Rosado 26 SCRA 470Tryzz dela MercedNo ratings yet

- iBex Home Warranty Invoice for 645 East 6910 South Midvale, UT 84047Document2 pagesiBex Home Warranty Invoice for 645 East 6910 South Midvale, UT 84047Laura MayNo ratings yet

- Leads ListDocument33 pagesLeads ListSadd Rahman100% (1)

- Worksheet - Income Sheet and Form Series 18 AICPA, AICPA Risk of Material Misstatement WorksheetsDocument20 pagesWorksheet - Income Sheet and Form Series 18 AICPA, AICPA Risk of Material Misstatement WorksheetswellawalalasithNo ratings yet

- LSR Checklist-Garima Maan & UtkarshDocument2 pagesLSR Checklist-Garima Maan & UtkarshavaneeshNo ratings yet

- Underwriting Collateral ReviewDocument60 pagesUnderwriting Collateral ReviewHimani SachdevNo ratings yet

- Midterm ExaminationDocument2 pagesMidterm Examinationchuyub ni hudasNo ratings yet

- Property 2 Outline Keyed To Dukeminier/Krier 6 Ed. UMKC, June Carbone Spring 2010Document40 pagesProperty 2 Outline Keyed To Dukeminier/Krier 6 Ed. UMKC, June Carbone Spring 2010mrspice100% (3)

- Philippines laws and regulations on land use, housing, real estateDocument5 pagesPhilippines laws and regulations on land use, housing, real estateJoshua Ardie Mesina100% (1)

- Measurement and accounting for changes in a lease termDocument3 pagesMeasurement and accounting for changes in a lease termJhon SudiarmanNo ratings yet

- Real Estate Assistant ResumeDocument5 pagesReal Estate Assistant Resumeafdmjphtj100% (1)

- Acknowledgment and JuratDocument5 pagesAcknowledgment and JuratJezza MarieNo ratings yet

- Exclusive Authorisation To AssignDocument2 pagesExclusive Authorisation To Assignardique100% (1)

- Need For A Trust: Wealth Management Commitment Is Never CasualDocument12 pagesNeed For A Trust: Wealth Management Commitment Is Never CasualVishal MishraNo ratings yet

- Sta. Fe Realty vs. SisonDocument9 pagesSta. Fe Realty vs. SisonKristine KristineeeNo ratings yet

- Land law - Key concepts and principlesDocument70 pagesLand law - Key concepts and principlesMaame Baidoo100% (2)

- Real Estate EssayDocument3 pagesReal Estate Essayapi-560714114No ratings yet

- Laws Relating to Housing (Part 1Document48 pagesLaws Relating to Housing (Part 1Chan LHgNo ratings yet

- Work Flow & StatusDocument3 pagesWork Flow & StatusmbNo ratings yet

- Sale of Immovable Property AssignmentDocument12 pagesSale of Immovable Property AssignmentNusrat ShatyNo ratings yet

- 2021 Assessment Summary Report - Final - April 21, 2021Document19 pages2021 Assessment Summary Report - Final - April 21, 2021Duluth News TribuneNo ratings yet

- Estate Calculation for Carlos, Peter, and LhinagDocument1 pageEstate Calculation for Carlos, Peter, and Lhinagchasing bluesNo ratings yet

- DEED OF SALE BernardinoDocument3 pagesDEED OF SALE BernardinoLegal Office BulacanNo ratings yet

- South MumbaiDocument16 pagesSouth MumbaiSumit Bhong50% (2)

- Revision Test (Home Test) Dated 27.07.2023Document2 pagesRevision Test (Home Test) Dated 27.07.2023Ashik.A Ashik.ANo ratings yet

- Fundamentals of Property OwnershipDocument62 pagesFundamentals of Property OwnershipJheovane Sevillejo LapureNo ratings yet

- Workbook Ansawer Key Unid 3Document1 pageWorkbook Ansawer Key Unid 3Miguel Mendez OeraNo ratings yet

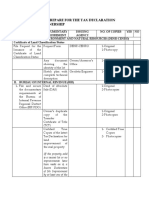

- Draft Requirements For Tax Declaration TranferDocument4 pagesDraft Requirements For Tax Declaration TranfercarmanvernonNo ratings yet