You might also like

- 1 - 10x10 Job Search Formula - ©2018 MilewalkDocument7 pages1 - 10x10 Job Search Formula - ©2018 Milewalksujaycj3614No ratings yet

- Property Name: Important CalculationsDocument2 pagesProperty Name: Important Calculationsapi-28625429No ratings yet

- Citi BankDocument6 pagesCiti Bankben tenNo ratings yet

- HR Health Check: Demo ReportDocument25 pagesHR Health Check: Demo ReportPuqti100% (1)

- Organisational Study in MBA INTERNSHIP PROJECTDocument61 pagesOrganisational Study in MBA INTERNSHIP PROJECTrangupadma83% (18)

- Offer LetterDocument9 pagesOffer LetterPrathamesh JabareNo ratings yet

- HR Analytics - Module AnswersDocument23 pagesHR Analytics - Module AnswersSiddhant Singh100% (5)

- Toronto Police - 2014 Sunshine List (Released March 16, 2015)Document121 pagesToronto Police - 2014 Sunshine List (Released March 16, 2015)TorontoSunNo ratings yet

- Accounts Receivable Factoring Guide: Expedite & Improve Your Cash FlowsFrom EverandAccounts Receivable Factoring Guide: Expedite & Improve Your Cash FlowsRating: 1 out of 5 stars1/5 (1)

- Progjyoti Joining LetterDocument6 pagesProgjyoti Joining LetterPorag Jyoti Neog75% (4)

- Business Ethics SLM 1 Marjonel B. Vargas 1Document25 pagesBusiness Ethics SLM 1 Marjonel B. Vargas 1Mariel RiveraNo ratings yet

- Foreclosure Letter 13-51-59Document3 pagesForeclosure Letter 13-51-59Kavipriyan MagudeeswaranNo ratings yet

- Employment Agreement Template 2020Document5 pagesEmployment Agreement Template 2020Mary gil AurelioNo ratings yet

- Small Business Enterprise Loan: Ermel O. TagardaDocument18 pagesSmall Business Enterprise Loan: Ermel O. Tagardaboa1315No ratings yet

- Paytail Credit ParametersDocument2 pagesPaytail Credit ParametersAmit SinghNo ratings yet

- Business - Account Services: Minimum Average Credit BalanceDocument6 pagesBusiness - Account Services: Minimum Average Credit BalanceSameer NooraniNo ratings yet

- 5BDF Orientation DeckDocument25 pages5BDF Orientation DeckEralyn OloresNo ratings yet

- Kotak Advance Fee-OnlineDocument1 pageKotak Advance Fee-Onlinejay.kumNo ratings yet

- Motorcycle LoanDocument10 pagesMotorcycle Loanrowilson reyNo ratings yet

- Purpose of Loan & Amount Information of ApplicantDocument5 pagesPurpose of Loan & Amount Information of ApplicantNecky SairahNo ratings yet

- BajajFinservStatement 47773424Document4 pagesBajajFinservStatement 47773424upesddn2010No ratings yet

- Green Veh OnepagerDocument2 pagesGreen Veh OnepagerRohith RaoNo ratings yet

- JD Nri RMDocument3 pagesJD Nri RMswarangiprabhu01No ratings yet

- Í) Qmwèââ Univ - Âofâtheâphil Âââ Â Ç+Â&05Jî Univ. of The Phils. - Manila/Diliman/Los BañosDocument3 pagesÍ) Qmwèââ Univ - Âofâtheâphil Âââ Â Ç+Â&05Jî Univ. of The Phils. - Manila/Diliman/Los BañospattsNo ratings yet

- Rate Schedule - American Airlines Credit UnionDocument2 pagesRate Schedule - American Airlines Credit UnionJonathan Seagull LivingstonNo ratings yet

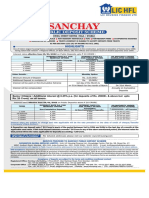

- Sanchay Public Deposit FormDocument6 pagesSanchay Public Deposit Formmanoj barokaNo ratings yet

- S. S. Prasad - Tax Planning & Financial Management, M. Com. Semester IV, Corporate Tax Planning & ManagementDocument9 pagesS. S. Prasad - Tax Planning & Financial Management, M. Com. Semester IV, Corporate Tax Planning & ManagementAmisha Singh VishenNo ratings yet

- JD PB RMDocument3 pagesJD PB RMVinayrajNo ratings yet

- Termsheet VelocityDocument4 pagesTermsheet VelocitysanjayNo ratings yet

- Sanction DlaDocument17 pagesSanction Dlampriya_rajesh1435No ratings yet

- Í E D, È Raquit Ramilâââââââââ M Çrâ) - 4?Î Mr. Ramil Misterio RaquitDocument4 pagesÍ E D, È Raquit Ramilâââââââââ M Çrâ) - 4?Î Mr. Ramil Misterio RaquitRamil RaquitNo ratings yet

- Financial Model v1.0 - 20210105Document5 pagesFinancial Model v1.0 - 20210105Tu CanNo ratings yet

- Vamsi Krishna KavatiDocument22 pagesVamsi Krishna KavatiRohit JNo ratings yet

- Project Report: OF Luxus InnDocument28 pagesProject Report: OF Luxus InnTanmay RakshitNo ratings yet

- Refunding Analysis Lecture 10112022 014637pmDocument11 pagesRefunding Analysis Lecture 10112022 014637pmdua nadeemNo ratings yet

- Statement of Principal Interest Rates and Service Charges For Domestic OperationsDocument12 pagesStatement of Principal Interest Rates and Service Charges For Domestic Operationsanon_431276397No ratings yet

- Partnership OperationsDocument20 pagesPartnership OperationsRujean Salar AltejarNo ratings yet

- Pre AgreementDocument3 pagesPre AgreementGcobisaAdonisNo ratings yet

- Team 10Document2 pagesTeam 10api-314570886No ratings yet

- 1 Investment Options To Retirement MoneyDocument3 pages1 Investment Options To Retirement MoneyAMIT SHARMANo ratings yet

- Service Charges: An Easy Guide To Banking FeesDocument24 pagesService Charges: An Easy Guide To Banking FeesolimNo ratings yet

- تمويل الشركات الناشئةDocument3 pagesتمويل الشركات الناشئةFARAH FZENo ratings yet

- Practical Evaluation of Financial ManagementDocument6 pagesPractical Evaluation of Financial ManagementScribdTranslationsNo ratings yet

- Group Assignment - March 2020Document10 pagesGroup Assignment - March 2020Dylan Rabin PereiraNo ratings yet

- Sankar R: Loan Account Statement For 6R2Cdd88708078Document3 pagesSankar R: Loan Account Statement For 6R2Cdd88708078Suresh ManiNo ratings yet

- COVID Incentives As at 30 March 2020Document2 pagesCOVID Incentives As at 30 March 2020Michael Armstrong100% (4)

- Orca Share Media1681431711029 7052435751300456049Document2 pagesOrca Share Media1681431711029 7052435751300456049JESSELNo ratings yet

- ForeclosureDocument3 pagesForeclosuremohammadafreed223No ratings yet

- Arpit Tyagi - 313733Document22 pagesArpit Tyagi - 313733arpit tyagiNo ratings yet

- FinMan Chapter 16 and 17 ProblemsDocument3 pagesFinMan Chapter 16 and 17 ProblemsJufel Ramirez100% (1)

- Smart Statement: Home Loan Cards ServiceDocument4 pagesSmart Statement: Home Loan Cards ServiceLakshmi MuvvalaNo ratings yet

- Í Wpicè Villanueva Carlâgeneâ S Ç/VUHî Engr. Carl Gene Saludar VillanuevaDocument2 pagesÍ Wpicè Villanueva Carlâgeneâ S Ç/VUHî Engr. Carl Gene Saludar Villanuevaceegee14No ratings yet

- USA Citibank BankDocument6 pagesUSA Citibank BanktravisdemitriusNo ratings yet

- Sanchay: Public Deposit SchemeDocument1 pageSanchay: Public Deposit SchemeShrikant MasulkerNo ratings yet

- Solutions Quiz 1 and Quiz 2Document9 pagesSolutions Quiz 1 and Quiz 2BatrisyiaNo ratings yet

- Business Loan PolicyDocument7 pagesBusiness Loan Policyniteshparewa372No ratings yet

- Flujo de EfectivoDocument5 pagesFlujo de EfectivoLuis OleaNo ratings yet

- BUCIO Assignment1 FINM6Document3 pagesBUCIO Assignment1 FINM6John McwayneNo ratings yet

- Calculation of Rebate: Particular Dr. CRDocument12 pagesCalculation of Rebate: Particular Dr. CRDennis BijuNo ratings yet

- CCPL MidDocument7 pagesCCPL MidMuhammad AliNo ratings yet

- MR Qinjian Jian Yan Jin 1527 Brookhaven DR Mclean Va 22101-4128Document4 pagesMR Qinjian Jian Yan Jin 1527 Brookhaven DR Mclean Va 22101-4128qjian100% (2)

- QC For Biz PowerPoint PresentationDocument7 pagesQC For Biz PowerPoint PresentationSamuel BeekaNo ratings yet

- Product Disclosure SheetDocument10 pagesProduct Disclosure SheetIzzudin Nur Syahmie Shahrol AffendiNo ratings yet

- Page 1 of 23: AddressDocument23 pagesPage 1 of 23: AddressSanjayNo ratings yet

- UNSECURED Technical Seminar On Finance Bill 2018 - Presentation (10 June 2018) Fin...Document90 pagesUNSECURED Technical Seminar On Finance Bill 2018 - Presentation (10 June 2018) Fin...Sabbir IsmailNo ratings yet

- Retail Credit Risk Management: Retail Banking and Business Development Division NRBC Bank LTDDocument28 pagesRetail Credit Risk Management: Retail Banking and Business Development Division NRBC Bank LTDkazi zamanNo ratings yet

- What Is SANFDocument17 pagesWhat Is SANFAbizawinnerNo ratings yet

- Vakrangee Franchisee Presentation Phase 1 IOCL v2Document15 pagesVakrangee Franchisee Presentation Phase 1 IOCL v2testengine701921No ratings yet

- SEV Handbook - Lite Version - English So TayDocument48 pagesSEV Handbook - Lite Version - English So TaytrietNo ratings yet

- Employer Responsibilities and Employee RightsDocument12 pagesEmployer Responsibilities and Employee RightsJhazielle DolleteNo ratings yet

- LP Gas - June 2016Document68 pagesLP Gas - June 2016Orlando BarriosNo ratings yet

- Human Resources Management Group AssignmentDocument13 pagesHuman Resources Management Group AssignmentTki NeweNo ratings yet

- Workers' Organization: Platon Labor RelationsDocument17 pagesWorkers' Organization: Platon Labor RelationsAngela Louise SabaoanNo ratings yet

- Campos CoffeeDocument6 pagesCampos Coffee劉宗霖No ratings yet

- Taxation Review June 16Document8 pagesTaxation Review June 16Shaiful Alam FCANo ratings yet

- English Phrases For A Job Interview: GreetingsDocument8 pagesEnglish Phrases For A Job Interview: GreetingsYasmin SchikorraNo ratings yet

- Salaries and Side Hustles British English StudentDocument7 pagesSalaries and Side Hustles British English StudentAnca StanNo ratings yet

- Current Liabilities & PayrollDocument12 pagesCurrent Liabilities & PayrollMesele AdemeNo ratings yet

- Overall Management Practice of Alita Bangladesh LimitedDocument36 pagesOverall Management Practice of Alita Bangladesh LimitedTushar All RounderNo ratings yet

- Katharos Company PDFDocument105 pagesKatharos Company PDFRich DesulocNo ratings yet

- G.R. No. L-58870 December 18, 1987 Cebu Institute of Technology (Cit), Petitioner, vs. Hon. Blas Ople FactsDocument12 pagesG.R. No. L-58870 December 18, 1987 Cebu Institute of Technology (Cit), Petitioner, vs. Hon. Blas Ople FactsAlyza Montilla BurdeosNo ratings yet

- Sales Management - Final Report - Group 2Document22 pagesSales Management - Final Report - Group 2Duy Nguyễn Lê NhậtNo ratings yet

- RBSDocument66 pagesRBSankit_sinha1990No ratings yet

- Standard Chartered BankDocument22 pagesStandard Chartered Bank12ekNo ratings yet

- Module 10 Compensation Income.1Document22 pagesModule 10 Compensation Income.1Jeon KookieNo ratings yet

- PHL-Kuwait MOUDocument8 pagesPHL-Kuwait MOUgmanewsNo ratings yet

- The Maharashtra State Tax On Professions, Trade, Callings and Employments Act, 1975Document34 pagesThe Maharashtra State Tax On Professions, Trade, Callings and Employments Act, 1975sam.verma1612No ratings yet

- Human Resource Management: Assignment-2Document12 pagesHuman Resource Management: Assignment-2Deepak R Gorad100% (1)

- Sta - Maria vs. LopezDocument53 pagesSta - Maria vs. LopezAnonymous 8liWSgmINo ratings yet