You might also like

- CRM IMPACT ON CUSTOMER LOYALTY AND RETENTION IN HOTEL INDUSTRYDocument37 pagesCRM IMPACT ON CUSTOMER LOYALTY AND RETENTION IN HOTEL INDUSTRYDba ApsuNo ratings yet

- CRM - Strategies and Practices in Selected Banks of PakistanDocument16 pagesCRM - Strategies and Practices in Selected Banks of PakistanAngelboy23No ratings yet

- CRM in Retailing: A Behavioural PerspectiveDocument14 pagesCRM in Retailing: A Behavioural PerspectiveRitesh SharmaNo ratings yet

- A Study On CRM Effectiveness in Public and Private Sector BanksDocument12 pagesA Study On CRM Effectiveness in Public and Private Sector Banksrukz623No ratings yet

- Final Report - Sub Team - Draft 1Document28 pagesFinal Report - Sub Team - Draft 1Mehedi HasanNo ratings yet

- A Study of Customer Relationship Management in Iranian Banking IndustryDocument7 pagesA Study of Customer Relationship Management in Iranian Banking IndustryonedademaNo ratings yet

- Customer Retention as an Effective CRM Tool in Co-operative BanksDocument20 pagesCustomer Retention as an Effective CRM Tool in Co-operative BanksGaurav LohagaonkarNo ratings yet

- Customer Relationship ManagementDocument30 pagesCustomer Relationship ManagementwhaenockNo ratings yet

- Ijrim Volume 2, Issue 9 (September 2012) (ISSN 2231-4334) Customer Relationship Management (CRM) Programmes in Banks: A Study of HDFC & Icici (India & Uk)Document10 pagesIjrim Volume 2, Issue 9 (September 2012) (ISSN 2231-4334) Customer Relationship Management (CRM) Programmes in Banks: A Study of HDFC & Icici (India & Uk)Divya PadmanabhanNo ratings yet

- Customer Relationship Management Practices in Select Public and Private Sector Banks in Chengalpattu DistrictDocument12 pagesCustomer Relationship Management Practices in Select Public and Private Sector Banks in Chengalpattu Districtindex PubNo ratings yet

- Jurnal Internasional Relationship Marketing Practices and Customer LoyaltyDocument12 pagesJurnal Internasional Relationship Marketing Practices and Customer LoyaltyTITAN_NGANJUKNo ratings yet

- CRM Practices in Bengaluru Shopping MallsDocument11 pagesCRM Practices in Bengaluru Shopping MallsGamers Squad TVNo ratings yet

- Relationship Marketing As An Orientation To Customer Retention: Evidence From Banks of PakistanDocument8 pagesRelationship Marketing As An Orientation To Customer Retention: Evidence From Banks of PakistanAyoade FakeyeNo ratings yet

- 4 5785386467438104023Document19 pages4 5785386467438104023Endris H. EbrahimNo ratings yet

- Background of The StudyDocument14 pagesBackground of The StudyCes SevillaNo ratings yet

- CRM Key to Bank Survival and Customer Loyalty in GhanaDocument11 pagesCRM Key to Bank Survival and Customer Loyalty in GhanaPallavi patilNo ratings yet

- Project Report On CRMDocument18 pagesProject Report On CRMSharan SharukhNo ratings yet

- Relationship Marketing and CustomerDocument12 pagesRelationship Marketing and CustomerSherliana ChannelNo ratings yet

- CRM Initiatives in Indian Retailing: A Study of Customer PerceptionsDocument5 pagesCRM Initiatives in Indian Retailing: A Study of Customer Perceptionsknowledge savvvyyyyyyNo ratings yet

- A Study On Customer Relationship Management Practices in Selected Private Sector Banks With Reference To Coimbatore DistrictDocument7 pagesA Study On Customer Relationship Management Practices in Selected Private Sector Banks With Reference To Coimbatore DistrictarcherselevatorsNo ratings yet

- Chapter 1Document40 pagesChapter 1Andrea AtonducanNo ratings yet

- CRM ProposalDocument15 pagesCRM ProposalMohammad AnisuzzamanNo ratings yet

- Report Impact of CRMDocument22 pagesReport Impact of CRMahsannawaxNo ratings yet

- A Study On Customer Relationship Management Practices in Selected Private Sector Banks With Reference To Coimbatore DistrictDocument6 pagesA Study On Customer Relationship Management Practices in Selected Private Sector Banks With Reference To Coimbatore DistrictthesijNo ratings yet

- A Study On Customer Relationship Management in Banks: Dr.P. AnbuoliDocument10 pagesA Study On Customer Relationship Management in Banks: Dr.P. AnbuoliDheer JangidNo ratings yet

- Customer Relationship Management As A Strategic Tool - Richa Raghuvanshi, Rashmi - MKT024Document21 pagesCustomer Relationship Management As A Strategic Tool - Richa Raghuvanshi, Rashmi - MKT024Pratyush TripathiNo ratings yet

- The Role of Customer Relationship Management in Enhancing Customer Loyalty (Body)Document67 pagesThe Role of Customer Relationship Management in Enhancing Customer Loyalty (Body)Akash MajjiNo ratings yet

- The Role of Customer Relationship Management in Enhancing Customer Loyalty (Body) Without Data InterpretationDocument30 pagesThe Role of Customer Relationship Management in Enhancing Customer Loyalty (Body) Without Data InterpretationAkash MajjiNo ratings yet

- Department of M-WPS OfficeDocument4 pagesDepartment of M-WPS Officeseid negashNo ratings yet

- Icici CRM PaperDocument9 pagesIcici CRM PaperNamita DeyNo ratings yet

- CRM AxisDocument4 pagesCRM AxisMukul KostaNo ratings yet

- The impact of CRM on organizational performanceDocument110 pagesThe impact of CRM on organizational performanceJayagokul SaravananNo ratings yet

- Transformation From Relationship Marketing To Electronic Customer Relationship Management: A Literature StudyDocument9 pagesTransformation From Relationship Marketing To Electronic Customer Relationship Management: A Literature StudyLynda ZemmourNo ratings yet

- A Study On Customer Relationship Management Practices in Banking SectorDocument11 pagesA Study On Customer Relationship Management Practices in Banking SectorFathimaNo ratings yet

- The Role of Customer Relationship Management in Enhancing Customer Loyalty (Body) With Capters 1,2,3Document28 pagesThe Role of Customer Relationship Management in Enhancing Customer Loyalty (Body) With Capters 1,2,3Akash MajjiNo ratings yet

- RM RLDocument13 pagesRM RLKommawar Shiva kumarNo ratings yet

- Review of Literature:: 1: CRM Is The Outcome of The Continuing Evolution and IntegrationDocument3 pagesReview of Literature:: 1: CRM Is The Outcome of The Continuing Evolution and Integrationvivekdubey1989No ratings yet

- The Role of Customer Relationship Management in Enhancing Customer Loyalty (Body)Document63 pagesThe Role of Customer Relationship Management in Enhancing Customer Loyalty (Body)Akash MajjiNo ratings yet

- Chapter 1 Introduction FinalDocument6 pagesChapter 1 Introduction FinalHiren PatelNo ratings yet

- Chapter 1 - Introduction - FinalDocument6 pagesChapter 1 - Introduction - FinalHiren PatelNo ratings yet

- Literature Review On Relationship Marketing PDFDocument5 pagesLiterature Review On Relationship Marketing PDFafmzxpqoizljqo100% (1)

- Literature Review: 2.1. Customer Relationship ManagementDocument78 pagesLiterature Review: 2.1. Customer Relationship ManagementTabish aliNo ratings yet

- Literature Review Customer Relationship Management BankingDocument5 pagesLiterature Review Customer Relationship Management BankingcmaqqsrifNo ratings yet

- Dissertation (1) CRMDocument31 pagesDissertation (1) CRMAniketArewarNo ratings yet

- CRM in Banking SectorDocument17 pagesCRM in Banking Sectorkshiti ahire100% (2)

- CRM Practices in Banking SectorDocument14 pagesCRM Practices in Banking SectorParvathy AdamsNo ratings yet

- Relationship Marketing Comparison of Public and Private BanksDocument10 pagesRelationship Marketing Comparison of Public and Private Banksarvind3041990No ratings yet

- Customer Relationship Management ArticlesDocument5 pagesCustomer Relationship Management ArticlesSanthosh SomaNo ratings yet

- Project ReportDocument69 pagesProject ReportAnonymous K8SKcbLBdr50% (2)

- A Study On Dealership Satisficaion Towards Soft Drinks in IndiaDocument8 pagesA Study On Dealership Satisficaion Towards Soft Drinks in IndiaRK FeaturesNo ratings yet

- Relationship Marketing and Customer Loyalty: Do Customer Satisfaction and Customer Trust Really Serve As Intervening Variables?Document12 pagesRelationship Marketing and Customer Loyalty: Do Customer Satisfaction and Customer Trust Really Serve As Intervening Variables?Anonymous Wo9RWmNo ratings yet

- An Implementation of Customer Relationship Management and Customer Satisfaction in Banking Sector of Quetta, BalochistanDocument12 pagesAn Implementation of Customer Relationship Management and Customer Satisfaction in Banking Sector of Quetta, Balochistankhuram MehmoodNo ratings yet

- 2160 EN The Influence of Costumer Relationship Management Toward Customer Loyalty in PTDocument10 pages2160 EN The Influence of Costumer Relationship Management Toward Customer Loyalty in PTMichel AndrianaNo ratings yet

- Customer Relationship Management in The InternatioDocument13 pagesCustomer Relationship Management in The InternatioAndrea ÁlvarezNo ratings yet

- Chapter - 1Document56 pagesChapter - 1arunjoseph165240No ratings yet

- Customer Relationship Management and Competitiveness of Commercial Banks in KenyaDocument25 pagesCustomer Relationship Management and Competitiveness of Commercial Banks in KenyaAAMIRREHMAN75010No ratings yet

- Crm in Action: Maximizing Value Through Market Segmentation, Product Differentiation & Customer RetentionFrom EverandCrm in Action: Maximizing Value Through Market Segmentation, Product Differentiation & Customer RetentionRating: 5 out of 5 stars5/5 (1)

- Customer Relationship Management: A powerful tool for attracting and retaining customersFrom EverandCustomer Relationship Management: A powerful tool for attracting and retaining customersRating: 3.5 out of 5 stars3.5/5 (3)

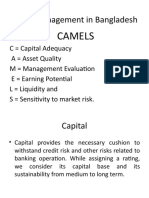

- Capital: Owner About Their Stake Hence More Safeguard Will Be The Borrowed FundsDocument28 pagesCapital: Owner About Their Stake Hence More Safeguard Will Be The Borrowed FundsMdramjanaliNo ratings yet

- Terms in CRMDocument28 pagesTerms in CRMMdramjanaliNo ratings yet

- Credit MonitoringDocument20 pagesCredit MonitoringPrasenjit SahaNo ratings yet

- Credit MonitoringDocument20 pagesCredit MonitoringPrasenjit SahaNo ratings yet

- Terms in CRMDocument28 pagesTerms in CRMMdramjanaliNo ratings yet

- Credit Monitoring.1997-2003Document24 pagesCredit Monitoring.1997-2003Prasenjit SahaNo ratings yet

- Credit Mgt. Loans and AdvanceDocument7 pagesCredit Mgt. Loans and AdvancePrasenjit SahaNo ratings yet

- Theory Used in AccountingDocument37 pagesTheory Used in AccountingPrasenjit SahaNo ratings yet

- Conceptual FrameworkDocument47 pagesConceptual FrameworkPrasenjit SahaNo ratings yet

- Accounting Theory ch10Document42 pagesAccounting Theory ch10Prasenjit SahaNo ratings yet

- Credit Risk Management and Loan Classification in BangladeshDocument13 pagesCredit Risk Management and Loan Classification in BangladeshPrasenjit SahaNo ratings yet

- Chapter 01 (FSA)Document3 pagesChapter 01 (FSA)Prasenjit SahaNo ratings yet

- Positive TheoryDocument70 pagesPositive TheoryPrasenjit SahaNo ratings yet

- Chapter 02Document16 pagesChapter 02Prasenjit SahaNo ratings yet

- Nej Mo A 1311738Document7 pagesNej Mo A 1311738cindy315No ratings yet

- Engine Rear Oil Seal PDFDocument3 pagesEngine Rear Oil Seal PDFDIEGONo ratings yet

- Tepache Kulit Nanas Sebagai Bahan Campuran Minuman 28 37Document10 pagesTepache Kulit Nanas Sebagai Bahan Campuran Minuman 28 37nabila sukmaNo ratings yet

- 00001Document20 pages00001Maggie ZhuNo ratings yet

- Assignement 4Document6 pagesAssignement 4sam khanNo ratings yet

- Inventory Valiuation Raw QueryDocument4 pagesInventory Valiuation Raw Querysatyanarayana NVSNo ratings yet

- Ndeb Bned Reference Texts 2019 PDFDocument11 pagesNdeb Bned Reference Texts 2019 PDFnavroop bajwaNo ratings yet

- Programmer Competency Matrix - Sijin JosephDocument8 pagesProgrammer Competency Matrix - Sijin JosephkikiNo ratings yet

- The Essential Guide To Data in The Cloud:: A Handbook For DbasDocument20 pagesThe Essential Guide To Data in The Cloud:: A Handbook For DbasInes PlantakNo ratings yet

- Chapter Three 3.0 Research MethodologyDocument5 pagesChapter Three 3.0 Research MethodologyBoyi EnebinelsonNo ratings yet

- Concrete Mixer Truck SinotrukDocument2 pagesConcrete Mixer Truck SinotrukTiago AlvesNo ratings yet

- 12 Orpic Safety Rules Managers May 17 RevDocument36 pages12 Orpic Safety Rules Managers May 17 RevGordon Longforgan100% (3)

- Fruit-Gathering by Tagore, Rabindranath, 1861-1941Document46 pagesFruit-Gathering by Tagore, Rabindranath, 1861-1941Gutenberg.orgNo ratings yet

- Insert - Elecsys Anti-HBs II - Ms - 05894816190.V2.EnDocument4 pagesInsert - Elecsys Anti-HBs II - Ms - 05894816190.V2.EnyantuNo ratings yet

- Q3 SolutionDocument5 pagesQ3 SolutionShaina0% (1)

- 2020-Effect of Biopolymers On Permeability of Sand-Bentonite MixturesDocument10 pages2020-Effect of Biopolymers On Permeability of Sand-Bentonite MixturesSaswati DattaNo ratings yet

- DMG48480F021 01WN DataSheetDocument16 pagesDMG48480F021 01WN DataSheeteminkiranNo ratings yet

- RCD-GillesaniaDocument468 pagesRCD-GillesaniaJomarie Alcano100% (2)

- To Quantitative Analysis: To Accompany by Render, Stair, Hanna and Hale Power Point Slides Created by Jeff HeylDocument94 pagesTo Quantitative Analysis: To Accompany by Render, Stair, Hanna and Hale Power Point Slides Created by Jeff HeylNino NatradzeNo ratings yet

- Module 1Document12 pagesModule 1Ajhay Torre100% (1)

- USA Gas TurbineDocument4 pagesUSA Gas TurbineJustin MercadoNo ratings yet

- Aptamers in HIV Research Diagnosis and TherapyDocument11 pagesAptamers in HIV Research Diagnosis and TherapymikiNo ratings yet

- Confidentiality Agreement With Undertaking and WaiverDocument1 pageConfidentiality Agreement With Undertaking and WaiverreddNo ratings yet

- LQRDocument34 pagesLQRkemoNo ratings yet

- "Network Security": Alagappa UniversityDocument1 page"Network Security": Alagappa UniversityPRADEEPRAJANo ratings yet

- 5e3 Like ApproachDocument1 page5e3 Like Approachdisse_detiNo ratings yet

- Synchronous Motor - InstruDocument12 pagesSynchronous Motor - InstruMohit IndurkarNo ratings yet

- Infrastructure Finance Project Design and Appraisal: Professor Robert B.H. Hauswald Kogod School of Business, AUDocument2 pagesInfrastructure Finance Project Design and Appraisal: Professor Robert B.H. Hauswald Kogod School of Business, AUAida0% (1)

- 1967 2013 PDFDocument70 pages1967 2013 PDFAlberto Dorado Martín100% (1)