You might also like

- 100 Business Ideas: Discover Home Business Ideas, Online Business Ideas, Small Business Ideas and Passive Income Ideas That Can Help You Start A Business and Achieve Financial FreedomFrom Everand100 Business Ideas: Discover Home Business Ideas, Online Business Ideas, Small Business Ideas and Passive Income Ideas That Can Help You Start A Business and Achieve Financial FreedomRating: 2.5 out of 5 stars2.5/5 (2)

- 1.what Is Debenture?: AnswersDocument16 pages1.what Is Debenture?: Answerssirisha222No ratings yet

- Financing Options for Small BusinessesDocument6 pagesFinancing Options for Small BusinessesJo Angeli100% (2)

- ABCs of SME financial management: assets, liabilities, equityDocument2 pagesABCs of SME financial management: assets, liabilities, equityPabloNo ratings yet

- Smart CapitalDocument35 pagesSmart Capitalno es anonimousNo ratings yet

- Business Finance TADocument9 pagesBusiness Finance TAOlivier MNo ratings yet

- Capital Structure PlanningDocument5 pagesCapital Structure PlanningAlok Singh100% (1)

- Finance Sources for StartupsDocument6 pagesFinance Sources for StartupskiranaishaNo ratings yet

- ReporDocument7 pagesReporRichard SarominesNo ratings yet

- Sources of FinanceDocument3 pagesSources of Financealok19886No ratings yet

- Bussiness Chapter 6-1Document5 pagesBussiness Chapter 6-1Bethelhem YetwaleNo ratings yet

- Chapter 19,20,21,22 Assesment QuestionsDocument19 pagesChapter 19,20,21,22 Assesment QuestionsSteven Sanderson100% (3)

- What Is Business Financing?: Key TakeawaysDocument4 pagesWhat Is Business Financing?: Key TakeawaysRica RaviaNo ratings yet

- CarsDocument10 pagesCarsMuhammad AwanNo ratings yet

- Bata Debt?Debt FreeDocument3 pagesBata Debt?Debt FreeBilal VaidNo ratings yet

- Complete FinanceDocument5 pagesComplete FinanceKappala AbhishekNo ratings yet

- Raise Financial CapitalDocument11 pagesRaise Financial CapitalkhanNo ratings yet

- The Importance of Cash Flow To A Corporation Khodeja Begum FIN 510 Week 2 Discussion Post Davenport UniversityDocument4 pagesThe Importance of Cash Flow To A Corporation Khodeja Begum FIN 510 Week 2 Discussion Post Davenport Universitybehumk31No ratings yet

- FinanceDocument68 pagesFinanceAngelica CruzNo ratings yet

- CPA Financial AccountingDocument72 pagesCPA Financial AccountingElysé KaregeyaNo ratings yet

- UNIT 4 - Module I 75: Accounting OBJECTIVES: After Studying This Chapter You Should Be Able ToDocument0 pagesUNIT 4 - Module I 75: Accounting OBJECTIVES: After Studying This Chapter You Should Be Able ToLuiza BoleaNo ratings yet

- Axial - CEO Guide To Debt FinancingDocument29 pagesAxial - CEO Guide To Debt FinancingcubanninjaNo ratings yet

- UNIT FOUR - AccountingDocument32 pagesUNIT FOUR - AccountingCristea GianiNo ratings yet

- Finance Viva Final SemesterDocument3 pagesFinance Viva Final SemesterSharfuddin ZishanNo ratings yet

- Transcription+Document +Cash+Flow+StatementDocument8 pagesTranscription+Document +Cash+Flow+StatementShafa IzwanNo ratings yet

- Week 05Document6 pagesWeek 05Mohammad Tahir MehdiNo ratings yet

- Sources of Finance For Startups and SMEsDocument4 pagesSources of Finance For Startups and SMEsTawanda Percy MutsandoNo ratings yet

- What Is Financing?: Business Activities Financial InstitutionsDocument3 pagesWhat Is Financing?: Business Activities Financial InstitutionsRica RaviaNo ratings yet

- COMPANY SHARES CORPORATE CAPITAL PDFDocument30 pagesCOMPANY SHARES CORPORATE CAPITAL PDFprashansha kumudNo ratings yet

- Notes W9.1Document3 pagesNotes W9.1adelemahe137No ratings yet

- Ernest and Young Interview QuestionsDocument57 pagesErnest and Young Interview QuestionsPratyush Raj Benya100% (2)

- 10 Terms You Must Know for Raising Startup CapitalDocument8 pages10 Terms You Must Know for Raising Startup CapitalLeseronNo ratings yet

- Financial Statements ExplainedDocument7 pagesFinancial Statements ExplainedAbdul Basit ChaudhryNo ratings yet

- 3rd Lesson International Business & Contract LawDocument3 pages3rd Lesson International Business & Contract Lawpetrinluca.9No ratings yet

- Glossary of Terms: Equity DilutionDocument9 pagesGlossary of Terms: Equity DilutionAshenafi Belete AlemayehuNo ratings yet

- Choose Between Loan or Shares When Starting a BusinessDocument19 pagesChoose Between Loan or Shares When Starting a BusinessChristian Nicolaus MbiseNo ratings yet

- Financing ConceptsDocument5 pagesFinancing ConceptsSoothing BlendNo ratings yet

- Equity Distribution in StartupsDocument2 pagesEquity Distribution in StartupsscribdanonimoNo ratings yet

- Research Papers On Internal and External Sources of FinanceDocument8 pagesResearch Papers On Internal and External Sources of Financevvjrpsbnd100% (1)

- Corp FinDocument6 pagesCorp FinIryna HoncharukNo ratings yet

- The 3 Key Financial Decisions Facing ManagersDocument6 pagesThe 3 Key Financial Decisions Facing ManagersSaAl-ismailNo ratings yet

- Finance - Html#Ixzz3Su1Owgre Attribution Non-Commercial Share AlikeDocument11 pagesFinance - Html#Ixzz3Su1Owgre Attribution Non-Commercial Share AlikeDeeNo ratings yet

- AssignmentDocument5 pagesAssignmentpankajjaiswal60No ratings yet

- Coperate FinanceDocument17 pagesCoperate Financegift lunguNo ratings yet

- Topic 2.1 - Raising Finance Learning Outcome The Aim of This Section Is For Students To Understand The FollowingDocument8 pagesTopic 2.1 - Raising Finance Learning Outcome The Aim of This Section Is For Students To Understand The FollowinggeorgianaNo ratings yet

- Company: 2. Financial Management in Old CompaniesDocument3 pagesCompany: 2. Financial Management in Old CompaniesVikash SinghNo ratings yet

- Transcription+Document +Introduction+to+Financial+Statements - Docx+Document7 pagesTranscription+Document +Introduction+to+Financial+Statements - Docx+Shafa IzwanNo ratings yet

- Assignment No 1Document9 pagesAssignment No 1Fahad AhmedNo ratings yet

- Corporate Finance Made SimpleDocument7 pagesCorporate Finance Made SimpleRamesh Arivalan100% (7)

- Tugas MK 1 (RETNO NOVIA MALLISA)Document5 pagesTugas MK 1 (RETNO NOVIA MALLISA)Vania OlivineNo ratings yet

- Bessemer Guide To Venture DebtDocument14 pagesBessemer Guide To Venture Debtarnoldlee1No ratings yet

- Financial Analysis TestDocument16 pagesFinancial Analysis TestLewie KhawNo ratings yet

- Technopreneurship 11 PDFDocument17 pagesTechnopreneurship 11 PDFjepongNo ratings yet

- Entrepreneurial Finance ResourcesDocument6 pagesEntrepreneurial Finance Resourcesfernando trinidadNo ratings yet

- Postscripts On The Fundamentals of Corporate FinanceDocument6 pagesPostscripts On The Fundamentals of Corporate FinancebehcetNo ratings yet

- 8 Things You Need To Know About Raising Venture CapitalDocument3 pages8 Things You Need To Know About Raising Venture CapitalJing GaoNo ratings yet

- Introduction To Corporate FinanceDocument5 pagesIntroduction To Corporate FinanceToru KhanNo ratings yet

- Definition of Business FinanceDocument4 pagesDefinition of Business FinanceClovisNo ratings yet

- Textile Industry: Riya Baldewa Manali Jain Shreya Kulkarni Kinnari Sangodkar ShreyaDocument4 pagesTextile Industry: Riya Baldewa Manali Jain Shreya Kulkarni Kinnari Sangodkar ShreyashreyaNo ratings yet

- Mutual Fund DataDocument194 pagesMutual Fund DatashreyaNo ratings yet

- Swot AnalysisDocument1 pageSwot AnalysisshreyaNo ratings yet

- Isr PDFDocument130 pagesIsr PDFGanga SinhaNo ratings yet

- Mutual Fund DataDocument194 pagesMutual Fund DatashreyaNo ratings yet

- Mantra 4 ChangeDocument1 pageMantra 4 ChangeshreyaNo ratings yet

- EPS, RoNW, ROCE Grow for VGL in FY 2019-20Document4 pagesEPS, RoNW, ROCE Grow for VGL in FY 2019-20shreyaNo ratings yet

- Economics AssignmentDocument2 pagesEconomics AssignmentshreyaNo ratings yet

- Accorr 1Document20 pagesAccorr 1shreyaNo ratings yet

- Telecom Industry Analysis - FinalDocument4 pagesTelecom Industry Analysis - FinalshreyaNo ratings yet

- Japan Lost DecadeDocument2 pagesJapan Lost DecadeshreyaNo ratings yet

- Sterlite Technologies Vision and MissionDocument217 pagesSterlite Technologies Vision and MissionshreyaNo ratings yet

- Synopsis FormatDocument2 pagesSynopsis FormatshreyaNo ratings yet

- Book 1Document12 pagesBook 1shreyaNo ratings yet

- Marriot 1Document20 pagesMarriot 1shreyaNo ratings yet

- Accorr 1Document20 pagesAccorr 1shreyaNo ratings yet

- ICE US - Key Financials and Operating Metrics from 2012-LTM 2019Document18 pagesICE US - Key Financials and Operating Metrics from 2012-LTM 2019shreyaNo ratings yet

- Marriot 1Document20 pagesMarriot 1shreyaNo ratings yet

- Hyatt ShreyaDocument4 pagesHyatt ShreyashreyaNo ratings yet

- Accorr 1Document20 pagesAccorr 1shreyaNo ratings yet

- HyattDocument3 pagesHyattshreyaNo ratings yet

- HyattDocument3 pagesHyattshreyaNo ratings yet

- Learning ObjectiveDocument6 pagesLearning ObjectiveJency RebencyNo ratings yet

- CSRDocument2 pagesCSRshreyaNo ratings yet

- Sterlite Technologies Vision and MissionDocument217 pagesSterlite Technologies Vision and MissionshreyaNo ratings yet

- BEC Study NotesDocument4 pagesBEC Study NotesCPA ChessNo ratings yet

- How Credit Influences the Business CycleDocument129 pagesHow Credit Influences the Business CycleKim Ritua - Tabudlo40% (5)

- RFQ Fuel Farm PakistanDocument23 pagesRFQ Fuel Farm PakistanBilel Markos100% (1)

- LLQP Financial Math2015sampleDocument10 pagesLLQP Financial Math2015sampleYat ChiuNo ratings yet

- Because or Due ToDocument9 pagesBecause or Due ToJiab PaodermNo ratings yet

- City Limits Magazine, June/July 1985 IssueDocument32 pagesCity Limits Magazine, June/July 1985 IssueCity Limits (New York)0% (1)

- Business Studies Holiday Homework: Art Integration ProjectDocument13 pagesBusiness Studies Holiday Homework: Art Integration ProjectAayush KapoorNo ratings yet

- Assignment QuestionsDocument5 pagesAssignment QuestionsRAJAT BANSAL0% (1)

- Interest Rate RetailDocument4 pagesInterest Rate RetailManvith B YNo ratings yet

- Darby Sporting Goods Inc Has Been Experiencing Growth in The PDFDocument2 pagesDarby Sporting Goods Inc Has Been Experiencing Growth in The PDFAnbu jaromiaNo ratings yet

- Education Loans For Higher StudiesDocument7 pagesEducation Loans For Higher StudiesSREYANo ratings yet

- Practical Approach of E-Filing Income Tax Return & Wealth StatementDocument1 pagePractical Approach of E-Filing Income Tax Return & Wealth StatementTanzeel Ur Rahman GazdarNo ratings yet

- Solved Carlos Opens A Dry Cleaning Store During The Year He PDFDocument1 pageSolved Carlos Opens A Dry Cleaning Store During The Year He PDFAnbu jaromiaNo ratings yet

- Portfolio Construction at ING VYSYA BankDocument11 pagesPortfolio Construction at ING VYSYA BankMOHAMMED KHAYYUMNo ratings yet

- Sample Resolution Transfer-SignatoriesDocument2 pagesSample Resolution Transfer-SignatoriesJaymart C. EstradaNo ratings yet

- Analysis of Non-fund Business for BanksDocument2 pagesAnalysis of Non-fund Business for BanksUtkarsh PrasadNo ratings yet

- Risk and Rates of ReturnDocument16 pagesRisk and Rates of ReturnSally Goodwill100% (1)

- Corporation Code of The Philippines ReviewerDocument3 pagesCorporation Code of The Philippines ReviewerJohnNo ratings yet

- Legal Validity of Notices Us 148 Post 1st April, 2021Document59 pagesLegal Validity of Notices Us 148 Post 1st April, 2021Kairav BhotiNo ratings yet

- EM5 UNIT 3 INTEREST FORMULAS & RATES Part 2Document7 pagesEM5 UNIT 3 INTEREST FORMULAS & RATES Part 2MOBILEE CANCERERNo ratings yet

- Source of Income Inequality PDFDocument16 pagesSource of Income Inequality PDFBeni GunawanNo ratings yet

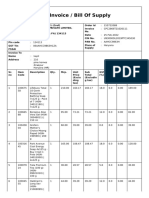

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplyKapil SinglaNo ratings yet

- MCA Proposal For OutsourcingDocument2 pagesMCA Proposal For OutsourcingLazaros KarapouNo ratings yet

- Equities ModuleDocument26 pagesEquities ModuleRahul M. DasNo ratings yet

- IndiaBanks GoldilocksWithAMinorBump20230310 PDFDocument26 pagesIndiaBanks GoldilocksWithAMinorBump20230310 PDFchaingangriteshNo ratings yet

- Advanced Financial Management Course OverviewDocument6 pagesAdvanced Financial Management Course OverviewNishit KalawadiaNo ratings yet

- Charlie Munger and The 2014 Daily Journal Annual MeetingDocument22 pagesCharlie Munger and The 2014 Daily Journal Annual Meetinganahata2014100% (1)

- Aptitude QN Set 4Document3 pagesAptitude QN Set 4priyajenatNo ratings yet

- Accountancy and Auditing 2-2011Document7 pagesAccountancy and Auditing 2-2011Muhammad BilalNo ratings yet

- Real Downstream Internet-Based Supply Chain Management: Hcorrea@Document23 pagesReal Downstream Internet-Based Supply Chain Management: Hcorrea@JeanCassioNo ratings yet