You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- RIAM Piano Album Elementary, Primary & Preliminary 2024Document1 pageRIAM Piano Album Elementary, Primary & Preliminary 2024jessicaaalexanderNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- IBM Payslip April 2012 PDFDocument1 pageIBM Payslip April 2012 PDFtaraivanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Ind 60644 Nat13471Document6 pagesInd 60644 Nat13471Matthew SorrensenNo ratings yet

- 14 Tocao Vs CA 342 SCRA 20 2001 PDFDocument3 pages14 Tocao Vs CA 342 SCRA 20 2001 PDFMarlon Louie ManaloNo ratings yet

- 13 Heirs of Tang Eng Kee Vs CA 341 SCRA 740 2000 PDFDocument10 pages13 Heirs of Tang Eng Kee Vs CA 341 SCRA 740 2000 PDFMarlon Louie ManaloNo ratings yet

- 12 Bastida Vs Menzi PDFDocument19 pages12 Bastida Vs Menzi PDFMarlon Louie ManaloNo ratings yet

- 02 Vicente Sy Vs Ca PDFDocument7 pages02 Vicente Sy Vs Ca PDFMarlon Louie ManaloNo ratings yet

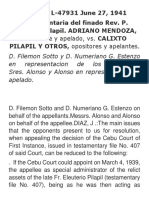

- In Re Pilapil2Document20 pagesIn Re Pilapil2Marlon Louie ManaloNo ratings yet

- Inter Paper11Document553 pagesInter Paper11PANDUNo ratings yet

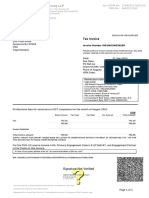

- EY Invoice - DUP - IN91MH3M030289Document1 pageEY Invoice - DUP - IN91MH3M030289AltafNo ratings yet

- PDFDocument7 pagesPDFwww_hari786No ratings yet

- Manthan Aug NewDocument1 pageManthan Aug NewManthan ShahNo ratings yet

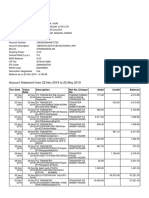

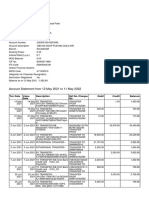

- Bank MuscatDocument3 pagesBank Muscatziadx.8.1998No ratings yet

- XUIHq MJ Ev Yr BN VFuDocument7 pagesXUIHq MJ Ev Yr BN VFuAbhijit SahaNo ratings yet

- Printed by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsDocument1 pagePrinted by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsLearning WebsiteNo ratings yet

- Final Payslip of Circle For 7-17Document11 pagesFinal Payslip of Circle For 7-17Manas Kumar SahooNo ratings yet

- Visa Prepaid Card ProgramDocument24 pagesVisa Prepaid Card ProgramAhmedFAbdeenNo ratings yet

- South Eastern Railway South Eastern Railway Sini Workshop/ WSH Sini Workshop/ WSHDocument1 pageSouth Eastern Railway South Eastern Railway Sini Workshop/ WSH Sini Workshop/ WSHShyamal NandiNo ratings yet

- Following Your Retirement As Senior Vice President of Finance ForDocument1 pageFollowing Your Retirement As Senior Vice President of Finance Fortrilocksp SinghNo ratings yet

- TX NotesDocument157 pagesTX Notessahalacca123No ratings yet

- NNCDocument7 pagesNNCHARRY THE GREATNo ratings yet

- Dispute Form - SERVICE and ERROR RELATED - Jofre Recososa For Ref 1-13404588837 or Ref 1-1340458840Document1 pageDispute Form - SERVICE and ERROR RELATED - Jofre Recososa For Ref 1-13404588837 or Ref 1-1340458840Ariel BajelotNo ratings yet

- Previous Balance Rs. Current Bill Rs. Payments/ Adjustment Rs. Total Payable RsDocument25 pagesPrevious Balance Rs. Current Bill Rs. Payments/ Adjustment Rs. Total Payable RsMuhammad ShehbazNo ratings yet

- Ip CameraDocument2 pagesIp CameraRaghavendar Reddy BobbalaNo ratings yet

- Billing 2 EW Additional WorksDocument1 pageBilling 2 EW Additional WorksJohn Nathaniel CafeeNo ratings yet

- TDS Ready ReckonerDocument29 pagesTDS Ready ReckonerShivani Singh ChandelNo ratings yet

- Suggested Answer On Tax Planning and Compliance Nov-Dec, 2023Document18 pagesSuggested Answer On Tax Planning and Compliance Nov-Dec, 2023Erfan KhanNo ratings yet

- Rohan AkritiDocument2 pagesRohan AkritikadasaliNo ratings yet

- UnpaidDocument2 pagesUnpaidMike PattisonNo ratings yet

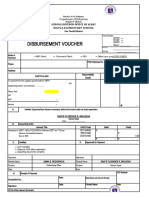

- Disbursement Voucher: Department of EducationDocument15 pagesDisbursement Voucher: Department of EducationMargel Airon TheoNo ratings yet

- NotingDocument160 pagesNotingdpkonnetNo ratings yet

- Taxpayer Identification Number - WikipediaDocument1 pageTaxpayer Identification Number - WikipediaBadhon Chandra SarkarNo ratings yet

- طرق قياس النشاط الاقتصادي 1Document7 pagesطرق قياس النشاط الاقتصادي 1MassilNo ratings yet

- PROBLEM EXERCISES IN TAXATION (Series 2019 - Part II) Prepared by Dr. Jeannie P. LimDocument16 pagesPROBLEM EXERCISES IN TAXATION (Series 2019 - Part II) Prepared by Dr. Jeannie P. LimXerjiah YuagaNo ratings yet

- SW 2Document2 pagesSW 2Miss IstiNo ratings yet