You might also like

- B Exercises: E3-1B (Transaction Analysis-Service Company)Document8 pagesB Exercises: E3-1B (Transaction Analysis-Service Company)Saleh RaoufNo ratings yet

- Chapter 1 - Introduction To Information Resource ManagementDocument29 pagesChapter 1 - Introduction To Information Resource ManagementJake Tamayo0% (1)

- Adjusted Trial Balance - P3-2A - Neosho River Resort - StudentDocument1 pageAdjusted Trial Balance - P3-2A - Neosho River Resort - StudentalnawasrehNo ratings yet

- ICT-Information and Communication TechnologyDocument18 pagesICT-Information and Communication TechnologySasika Pamuditha0% (1)

- Accounting CH 1 - HomeworkDocument6 pagesAccounting CH 1 - HomeworkAxel OngNo ratings yet

- Payroll: EMPL Name Gross Pay S.S Tax Net Pay Empl Number Hourly Rate Hours WorkedDocument5 pagesPayroll: EMPL Name Gross Pay S.S Tax Net Pay Empl Number Hourly Rate Hours WorkedNatoya RichardsNo ratings yet

- ACC 200 Tutorial QuestionsDocument72 pagesACC 200 Tutorial Questionsherueux67% (3)

- 86. Lotte's first influences at universityDocument4 pages86. Lotte's first influences at universityThao NguyenNo ratings yet

- P3 2A AnswerDocument2 pagesP3 2A AnswerMinh NhậtNo ratings yet

- Chapter - 6 Data RepresentationDocument8 pagesChapter - 6 Data RepresentationAshish SharmaNo ratings yet

- Excel DATE and TIME FunctionsDocument3 pagesExcel DATE and TIME FunctionsArslan SaleemNo ratings yet

- MYOB Sample QuestionsDocument10 pagesMYOB Sample QuestionsKay BMNo ratings yet

- CH 01Document2 pagesCH 01vivien0% (1)

- General Journal EntriesDocument35 pagesGeneral Journal EntriesUyên Nguyễn Hoàng ThanhNo ratings yet

- CH 4 - HomeworkDocument5 pagesCH 4 - HomeworkAxel OngNo ratings yet

- Principles of Accounting Lecture 3Document30 pagesPrinciples of Accounting Lecture 3Masum HossainNo ratings yet

- Solved ProblemsDocument74 pagesSolved Problemssmitha_gururaj100% (2)

- Writing: J1 Date Account Titles and Explanation Ref. Debit CreditDocument3 pagesWriting: J1 Date Account Titles and Explanation Ref. Debit Creditahmad Fauzani Muslim100% (1)

- 11 Com Pre-ExamDocument4 pages11 Com Pre-ExamObaid Khan50% (2)

- Haramaya University: Collage of Computing and Informatics Department of Information TechnologyDocument36 pagesHaramaya University: Collage of Computing and Informatics Department of Information Technologyamsalu alemuNo ratings yet

- Math 111 Lecture Notes: Chicken NameDocument10 pagesMath 111 Lecture Notes: Chicken Nameabu amos omamuzoNo ratings yet

- Bad Debt Provision: Accounting for Uncollectible Accounts ReceivableDocument4 pagesBad Debt Provision: Accounting for Uncollectible Accounts ReceivableHopeNo ratings yet

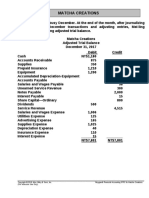

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- Modern Advanced Accounting Group AssignmentDocument1 pageModern Advanced Accounting Group Assignmentmohamed dahir Abdirahmaan100% (1)

- Ch1 Problems Acc2Document2 pagesCh1 Problems Acc2Fares EL DeenNo ratings yet

- Homework Chapter 8Document10 pagesHomework Chapter 8Trung Kiên Nguyễn0% (1)

- 2017 AnswerDocument4 pages2017 AnswerAbraham AlemsegedNo ratings yet

- Lab Activity 4Document3 pagesLab Activity 4student wwNo ratings yet

- Use Perpetual Inventory System For P6.3Document15 pagesUse Perpetual Inventory System For P6.3Giang LinhNo ratings yet

- Best-Fit Topology - LO2 Part IIDocument118 pagesBest-Fit Topology - LO2 Part IIabenezerNo ratings yet

- SQL D3 P003 Emp MGNTDocument3 pagesSQL D3 P003 Emp MGNTNguyen Quang HuyNo ratings yet

- Unit 1introduction To Report WritingDocument34 pagesUnit 1introduction To Report WritingNguyễN HoànG BảO MuNNo ratings yet

- De Bai-Dn Binh Minh-Dn Thuong MaiDocument4 pagesDe Bai-Dn Binh Minh-Dn Thuong MaiĐức TiếnNo ratings yet

- Classify The Following Into Assets or LiabilitiesDocument2 pagesClassify The Following Into Assets or LiabilitiesSandraMarie JamesNo ratings yet

- Advanced Cases For Cfs - Testbank Case 1: 905,410 Tax Paid (Cash Payment) Interest Paid (Cash Payments)Document21 pagesAdvanced Cases For Cfs - Testbank Case 1: 905,410 Tax Paid (Cash Payment) Interest Paid (Cash Payments)Uyên Nguyễn Hoàng ThanhNo ratings yet

- Accounting PracticeDocument14 pagesAccounting PracticeHamza RaufNo ratings yet

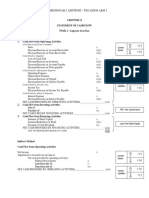

- Materi Chapter 23 Cash FlowDocument2 pagesMateri Chapter 23 Cash FlowM Reza andriantoNo ratings yet

- Business Studies - Work Book Activity Chapter 1Document16 pagesBusiness Studies - Work Book Activity Chapter 1gaiyun209No ratings yet

- 7 Cs of Communication QuizDocument4 pages7 Cs of Communication QuizLUCINO JR VALMORESNo ratings yet

- Homework Week 5 TreesDocument6 pagesHomework Week 5 TreesLe Thi Cam Nhung100% (1)

- KuratsisisisisDocument7 pagesKuratsisisisisEloPoPoNo ratings yet

- Excel Skills - Exercises - Pivot Tables: Step TaskDocument12 pagesExcel Skills - Exercises - Pivot Tables: Step Taskchkhurram0% (1)

- Practical Exercises SpredsheetsDocument17 pagesPractical Exercises SpredsheetsCecille IdjaoNo ratings yet

- Final ExamDocument15 pagesFinal Examruacon35No ratings yet

- 2 TOEIC Moon Part 5Document90 pages2 TOEIC Moon Part 5Luz Dianne SoloriaNo ratings yet

- Ms Access Practice Quiz 01Document5 pagesMs Access Practice Quiz 01specialityNo ratings yet

- CH 09Document64 pagesCH 09Khánh Nguyễn100% (1)

- Cost AacctDocument19 pagesCost AacctKiraYamatoNo ratings yet

- Business Statistics Class Practice QuestionsDocument12 pagesBusiness Statistics Class Practice QuestionsRaman KulkarniNo ratings yet

- Relationship Between Pointers and ArraysDocument46 pagesRelationship Between Pointers and Arraysfadi lamoNo ratings yet

- Solution Manuals DownloadDocument5 pagesSolution Manuals DownloadPutu DenyNo ratings yet

- Exam # 2 Chapter 15, 16, 17 ReviewDocument2 pagesExam # 2 Chapter 15, 16, 17 ReviewAnnNo ratings yet

- ch01 ProblemsDocument7 pagesch01 Problemsapi-274120622No ratings yet

- Preston Department Store Has A New Promotional Program That Offers A Free GiftDocument3 pagesPreston Department Store Has A New Promotional Program That Offers A Free GiftElliot RichardNo ratings yet

- Ass's PackDocument14 pagesAss's PackbayushNo ratings yet

- ch04 STDocument74 pagesch04 STKaseyNo ratings yet

- Financial Accounting Chap4Document48 pagesFinancial Accounting Chap4k60.2114920002No ratings yet

- Completing The Accounting Cycle: IFRS 4th EditionDocument74 pagesCompleting The Accounting Cycle: IFRS 4th EditionAnnie DuolingoNo ratings yet

- CH 04Document71 pagesCH 04Linh Trần Thị KhánhNo ratings yet

- Chapter 4 - Completing The Accounting CycleDocument39 pagesChapter 4 - Completing The Accounting CycleHuỳnh TrọngNo ratings yet

- Proofreading Exercise 3: Identifying 20 Mechanical ErrorsDocument1 pageProofreading Exercise 3: Identifying 20 Mechanical ErrorsIsmadth2918388No ratings yet

- Antigen ReceptorsDocument25 pagesAntigen ReceptorsIsmadth2918388No ratings yet

- Carcinogen Es IsDocument45 pagesCarcinogen Es IsIsmadth2918388No ratings yet

- The Pathogen MDSC-1405Document70 pagesThe Pathogen MDSC-1405Ismadth2918388No ratings yet

- Global Marketing - Ch10 Brand and Product Decisions in Global MarketingDocument22 pagesGlobal Marketing - Ch10 Brand and Product Decisions in Global MarketingIsmadth2918388No ratings yet

- How to Write a Compare and Contrast EssayDocument4 pagesHow to Write a Compare and Contrast EssayIsmadth2918388No ratings yet

- Week 12 - Comparison and Contrast Analysis Essay - Two Protective Services in A Named Caribbean CountryDocument3 pagesWeek 12 - Comparison and Contrast Analysis Essay - Two Protective Services in A Named Caribbean CountryIsmadth2918388No ratings yet

- Essaytigers Compare and Contrast Essay Sample PDFDocument4 pagesEssaytigers Compare and Contrast Essay Sample PDFbelbachirNo ratings yet

- Week 11 - Comparison and Contrast Analysis Essay - Local Elections and General Elections in A Named Caribbean CountryDocument4 pagesWeek 11 - Comparison and Contrast Analysis Essay - Local Elections and General Elections in A Named Caribbean CountryIsmadth2918388No ratings yet

- MGMT2023 Lecture 7 STOCK VALUATION - Parts I, II IIIDocument86 pagesMGMT2023 Lecture 7 STOCK VALUATION - Parts I, II IIIIsmadth2918388No ratings yet

- Self-Assessment Exercise (Week 10) - Editing A Comparison and Contrast Analysis EssayDocument3 pagesSelf-Assessment Exercise (Week 10) - Editing A Comparison and Contrast Analysis EssayIsmadth2918388No ratings yet

- Self-Assessment Answers (Week 10) - Editing A Comparison and Contrast Analysis EssayDocument3 pagesSelf-Assessment Answers (Week 10) - Editing A Comparison and Contrast Analysis EssayIsmadth2918388No ratings yet

- Ezrti: The University The West IndiesDocument8 pagesEzrti: The University The West IndiesIsmadth2918388No ratings yet

- The Umversity of The West IndiesDocument7 pagesThe Umversity of The West IndiesIsmadth2918388No ratings yet

- MGMT2023 Lecture 7 BOND VALUATION - Parts I IIDocument66 pagesMGMT2023 Lecture 7 BOND VALUATION - Parts I IIIsmadth2918388No ratings yet

- TVM Part I - Calculating Future ValueDocument91 pagesTVM Part I - Calculating Future ValueIsmadth2918388No ratings yet

- Risk and ReturnDocument57 pagesRisk and ReturnIsmadth2918388No ratings yet

- Lecture 1 - StudentDocument15 pagesLecture 1 - StudentIsmadth2918388No ratings yet

- Cash Flow and Financial PlanningDocument48 pagesCash Flow and Financial PlanningIsmadth2918388100% (1)

- MGMT2023 Lecture 8 - Capital Budgeting Part 1Document44 pagesMGMT2023 Lecture 8 - Capital Budgeting Part 1Ismadth2918388No ratings yet

- MGMT2023 MGMT2023 Lecture 2Document51 pagesMGMT2023 MGMT2023 Lecture 2Ismadth2918388No ratings yet

- MGMT2023 Lecture 9. Capital Budgeting Part 2 PDFDocument45 pagesMGMT2023 Lecture 9. Capital Budgeting Part 2 PDFIsmadth2918388No ratings yet

- Blueprint For Engagement - Authentic Leadership PDFDocument143 pagesBlueprint For Engagement - Authentic Leadership PDFSaNo ratings yet

- MGMT2023-Lecture 1-Intro To Financial ManagementDocument23 pagesMGMT2023-Lecture 1-Intro To Financial ManagementIsmadth2918388No ratings yet

- Sample Group Project - Ethics FinalDocument35 pagesSample Group Project - Ethics FinalIsmadth2918388No ratings yet

- Mgmt3035 FinalsDocument4 pagesMgmt3035 FinalsIsmadth2918388No ratings yet

- Intro To Time Value of MoneyDocument1 pageIntro To Time Value of MoneyIsmadth2918388No ratings yet

- Student SlidesDocument14 pagesStudent SlidesIsmadth2918388No ratings yet

- Rajinanti Ramdass Assignment 1Document1 pageRajinanti Ramdass Assignment 1Ismadth2918388No ratings yet

- mgmt3035 FinalsDocument4 pagesmgmt3035 FinalsIsmadth2918388No ratings yet

- Muchael - Challenges of Cross Border Mergers and Acquisition A Case Study of Tiger Brands Limited (HACO Industries Limited)Document64 pagesMuchael - Challenges of Cross Border Mergers and Acquisition A Case Study of Tiger Brands Limited (HACO Industries Limited)Denis Deno RotichNo ratings yet

- Energy Drinks, Sports DrinksDocument13 pagesEnergy Drinks, Sports DrinksNadia RevaldyNo ratings yet

- Case Study 6 AccentureDocument3 pagesCase Study 6 AccentureYash BansalNo ratings yet

- Articles Continuation VMVDocument3 pagesArticles Continuation VMVScott Adkins100% (2)

- Chapter 7 Cash ReceivablesDocument8 pagesChapter 7 Cash Receivablesironcross1988No ratings yet

- Cash BooksDocument13 pagesCash BooksWanjala RajabNo ratings yet

- Capitalization TableDocument10 pagesCapitalization TableDiego OssaNo ratings yet

- SWOT of Comm. Bank of CeylonDocument2 pagesSWOT of Comm. Bank of Ceylonpavel45702567% (21)

- Management Basics PDFDocument14 pagesManagement Basics PDFanissaNo ratings yet

- f1098t PDFDocument6 pagesf1098t PDFashley valdiviaNo ratings yet

- Tata Family TreeDocument1 pageTata Family Treemadan321100% (1)

- Accounting Processes For Remittance To PLIsDocument12 pagesAccounting Processes For Remittance To PLIsjojeNo ratings yet

- The Travels of A T-Shirt in The Global Economy SCRDocument11 pagesThe Travels of A T-Shirt in The Global Economy SCRCarlos MendezNo ratings yet

- Week 9 - Job Order&process Costing ActivityDocument5 pagesWeek 9 - Job Order&process Costing ActivityMark IlanoNo ratings yet

- Patanjali Strategy Segmentation Positioning Growth Objectives Strengths Weaknesses Market Share Competitor ReactionDocument2 pagesPatanjali Strategy Segmentation Positioning Growth Objectives Strengths Weaknesses Market Share Competitor ReactionGitanshNo ratings yet

- NBFC CompaniesDocument62 pagesNBFC CompaniesVikram ChauhanNo ratings yet

- Econ 20039 Final Exam AdviceDocument2 pagesEcon 20039 Final Exam AdviceShaikh Hafizur RahmanNo ratings yet

- Modeling and Analysis of Stochastic Systems 3rd Kulkarni Solution ManualDocument8 pagesModeling and Analysis of Stochastic Systems 3rd Kulkarni Solution ManualJamesAndersongoki94% (31)

- Rockford Company Case StudyDocument1 pageRockford Company Case StudyYohanes Fernando50% (2)

- Approved List of Contractors Military Engineer List of Contractors Upto 29 FebDocument89 pagesApproved List of Contractors Military Engineer List of Contractors Upto 29 Febmaxisinc.inNo ratings yet

- Logistics StandardDocument26 pagesLogistics StandardMarcoNo ratings yet

- Dow EmulsifiersDocument4 pagesDow EmulsifiersxxtupikxxNo ratings yet

- Review-ASM1-Nguyen Thi Cam TienDocument12 pagesReview-ASM1-Nguyen Thi Cam TienNguyen Thi Cam Tien (FPI HCM)No ratings yet

- Production Subcontracting - External Processing (BJK - DE) : Test Script SAP S/4HANA Cloud - 12-04-19Document20 pagesProduction Subcontracting - External Processing (BJK - DE) : Test Script SAP S/4HANA Cloud - 12-04-19sathishkumr_rsk100% (1)

- Movement of Nigeria From Mixed Economy To Capital EconomyDocument9 pagesMovement of Nigeria From Mixed Economy To Capital EconomyAdedokun AbayomiNo ratings yet

- Duke Plasto Ratio ReportDocument43 pagesDuke Plasto Ratio ReportMukesh Patel100% (2)

- Capitalstructuretheory 090408162048 Phpapp02Document22 pagesCapitalstructuretheory 090408162048 Phpapp02Khodeez NingthoujamNo ratings yet

- Employee Engagement Project ReportDocument38 pagesEmployee Engagement Project ReportArpitathakor100% (1)

- Effects of Environment On International BusinessDocument28 pagesEffects of Environment On International BusinessSumit BanduniNo ratings yet

- Negotiation StrategiesDocument4 pagesNegotiation Strategiescindy oktriaNo ratings yet