You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- ACST603 Exam - Session 2 2017Document14 pagesACST603 Exam - Session 2 2017St Dalfour CebuNo ratings yet

- Smart Rentals LTD General Journal 30 June 2020: Date Account Name Post Ref Debit CreditDocument3 pagesSmart Rentals LTD General Journal 30 June 2020: Date Account Name Post Ref Debit CreditSt Dalfour CebuNo ratings yet

- ACCG 611 Principles of Accounting Session 2, 2019 Final Examination: DIRECTIONS TO CANDIDATESDocument2 pagesACCG 611 Principles of Accounting Session 2, 2019 Final Examination: DIRECTIONS TO CANDIDATESSt Dalfour CebuNo ratings yet

- Quiz 2 Announcement: ACCG 611 Principles of AccountingDocument1 pageQuiz 2 Announcement: ACCG 611 Principles of AccountingSt Dalfour CebuNo ratings yet

- Extra Critical Thinking and Challenging QuestionDocument2 pagesExtra Critical Thinking and Challenging QuestionSt Dalfour CebuNo ratings yet

- Week 10 WACCDocument10 pagesWeek 10 WACCSt Dalfour CebuNo ratings yet

- ACST603 Final Exam2019 Sem2 Cover SheetFormula Sheet-2Document5 pagesACST603 Final Exam2019 Sem2 Cover SheetFormula Sheet-2St Dalfour CebuNo ratings yet

- Tutorial Week 12 WACC QuestionsDocument4 pagesTutorial Week 12 WACC QuestionsSt Dalfour CebuNo ratings yet

- Real Life Example of The Role of Accounting in A Corporate CollapseDocument1 pageReal Life Example of The Role of Accounting in A Corporate CollapseSt Dalfour CebuNo ratings yet

- Tutorial Week 12 WACC QuestionsDocument4 pagesTutorial Week 12 WACC QuestionsSt Dalfour CebuNo ratings yet

- Final Exam Information Sheet - ACST603-2Document5 pagesFinal Exam Information Sheet - ACST603-2St Dalfour CebuNo ratings yet

- Final Exam Paper - ACST603 - 2018.S2Document21 pagesFinal Exam Paper - ACST603 - 2018.S2St Dalfour CebuNo ratings yet

- ACST603 Exam - Session 2 2017Document14 pagesACST603 Exam - Session 2 2017St Dalfour CebuNo ratings yet

- Tutorial On Risk and StatisticsDocument5 pagesTutorial On Risk and StatisticsSt Dalfour CebuNo ratings yet

- ACST603 Final Exam2019 Sem2 Cover SheetFormula Sheet-2Document5 pagesACST603 Final Exam2019 Sem2 Cover SheetFormula Sheet-2St Dalfour CebuNo ratings yet

- ACST603 Exam - Session 2 2017Document14 pagesACST603 Exam - Session 2 2017St Dalfour CebuNo ratings yet

- Lecture 2 Single Payment Cashflows 2017 S2Document41 pagesLecture 2 Single Payment Cashflows 2017 S2St Dalfour CebuNo ratings yet

- Tutorial Week 12 WACC QuestionsDocument4 pagesTutorial Week 12 WACC QuestionsSt Dalfour CebuNo ratings yet

- Lecture 1 (I) Forms of Business - 2017S2Document13 pagesLecture 1 (I) Forms of Business - 2017S2St Dalfour CebuNo ratings yet

- Lecture 1 (Ii) Taxation Depreciation-2017s2Document15 pagesLecture 1 (Ii) Taxation Depreciation-2017s2St Dalfour CebuNo ratings yet

- Tut5 HomeLoans-QuestionsDocument256 pagesTut5 HomeLoans-QuestionsSt Dalfour CebuNo ratings yet

- ACST603 Tutorial 2 S1 2017 QuestionsDocument3 pagesACST603 Tutorial 2 S1 2017 QuestionsSt Dalfour CebuNo ratings yet

- Sample Balance Sheet and Income Statement Lecture 1 (III) - 2Document2 pagesSample Balance Sheet and Income Statement Lecture 1 (III) - 2St Dalfour CebuNo ratings yet

- Sample Balance Sheet and Income Statement Lecture 1 (III) - 2Document2 pagesSample Balance Sheet and Income Statement Lecture 1 (III) - 2St Dalfour CebuNo ratings yet

- (16 Cost Accounting Systems)Document71 pages(16 Cost Accounting Systems)St Dalfour CebuNo ratings yet

- Lecture 4 Bond Valuation S1 2017Document23 pagesLecture 4 Bond Valuation S1 2017St Dalfour CebuNo ratings yet

- Lecture 1 (Iii) Financial Measurement - 2017S2Document24 pagesLecture 1 (Iii) Financial Measurement - 2017S2St Dalfour CebuNo ratings yet

- Delegation Skills PresentationDocument61 pagesDelegation Skills PresentationSt Dalfour CebuNo ratings yet

- A.C. No. 8380 November 20, 2009 ARELLANO UNIVERSITY, INC. Complainant, Atty. Leovigildo H. Mijares Iii, RespondentDocument4 pagesA.C. No. 8380 November 20, 2009 ARELLANO UNIVERSITY, INC. Complainant, Atty. Leovigildo H. Mijares Iii, RespondentSt Dalfour CebuNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Taxpack: A Guide To Help You Prepare and Lodge Your Tax ReturnDocument132 pagesTaxpack: A Guide To Help You Prepare and Lodge Your Tax ReturnRanji SoulNo ratings yet

- Obligation Are Usually Greater Than BeforeDocument4 pagesObligation Are Usually Greater Than Beforehyunsuk fhebieNo ratings yet

- 6 Months Gove Scheme 2Document11 pages6 Months Gove Scheme 2Pavan BathamNo ratings yet

- Challenge-Trg Recruitment LTDDocument1 pageChallenge-Trg Recruitment LTDVEROVWO DUKUNo ratings yet

- List of Annuity Service Providers Enrolled Under NPS - NPS TrustDocument10 pagesList of Annuity Service Providers Enrolled Under NPS - NPS TrustPURCHASE OFFICERNo ratings yet

- Retirement BenefitsDocument10 pagesRetirement BenefitsRs AbhishekNo ratings yet

- Enforcement of The Employees' Provident Funds and Miscellaneous Provisions Act, 1952Document14 pagesEnforcement of The Employees' Provident Funds and Miscellaneous Provisions Act, 1952BhaveshNo ratings yet

- HL Guide Retirement For Under 40s 1018Document18 pagesHL Guide Retirement For Under 40s 1018BenNo ratings yet

- 398 Special Teachers Notional Increments G.O.no.28 Dated 01.03.2019Document2 pages398 Special Teachers Notional Increments G.O.no.28 Dated 01.03.2019Abdul Aleem ShaikNo ratings yet

- Paper 4Document25 pagesPaper 4sivaramkumarNo ratings yet

- HR Policy of Icici BankDocument4 pagesHR Policy of Icici Bankabdul rehman100% (1)

- The Employees' Pension SchemeDocument2 pagesThe Employees' Pension Schemedayanidhi nayakNo ratings yet

- SchemesTap Booster - JANUARY-MAY-2023-RBIDocument51 pagesSchemesTap Booster - JANUARY-MAY-2023-RBIRoshu MISHUNo ratings yet

- FAQs On NPS (UOS)Document27 pagesFAQs On NPS (UOS)abhinavNo ratings yet

- List of Master Circulars Issued by Railway BoardDocument10 pagesList of Master Circulars Issued by Railway BoardRajendra Kumar100% (2)

- certification ETHICSDocument22 pagescertification ETHICSranjitdhillon770No ratings yet

- Literature Review On Sbi Life InsuranceDocument4 pagesLiterature Review On Sbi Life Insurancefvgneqv8100% (1)

- Chapter 4. Personnal Income Tax (I)Document8 pagesChapter 4. Personnal Income Tax (I)Martin Pelaez PerezNo ratings yet

- DLCPM00312970000013908 2022Document2 pagesDLCPM00312970000013908 2022Anshul KatiyarNo ratings yet

- Glaxosmithkline Consumer Healthcare Pakistan Limited List of Shareholders As of 30-06-2021Document522 pagesGlaxosmithkline Consumer Healthcare Pakistan Limited List of Shareholders As of 30-06-2021Hamza AsifNo ratings yet

- Salary HP Liability in Special CasesDocument33 pagesSalary HP Liability in Special CasesPriyanshu tripathiNo ratings yet

- Application To Start Family PensionDocument4 pagesApplication To Start Family PensionSabuj SarkarNo ratings yet

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 418366390250720 Assessment Year: 2019-20Document6 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 418366390250720 Assessment Year: 2019-20Mudavath RajuNo ratings yet

- Andhra Pradesh Grameena Vikas Bank pension regulationsDocument97 pagesAndhra Pradesh Grameena Vikas Bank pension regulationskiran dupatiNo ratings yet

- College of Business Administration and Accountancy Final Exam ReviewDocument11 pagesCollege of Business Administration and Accountancy Final Exam ReviewtannyNo ratings yet

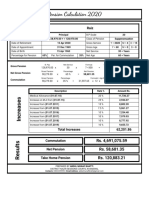

- Pension Calculation 2020 DetailsDocument1 pagePension Calculation 2020 DetailsAhmad FarhanNo ratings yet

- GO Ms No.52 - Dt.11.06.2021 - DADocument3 pagesGO Ms No.52 - Dt.11.06.2021 - DAExecutive Engineer R&BNo ratings yet

- Accounting For The Payroll System in An Ethiopian ContextDocument11 pagesAccounting For The Payroll System in An Ethiopian ContextalemayehuNo ratings yet

- Update Income Tax Software for New or Old Tax SlabDocument29 pagesUpdate Income Tax Software for New or Old Tax SlabSREERAMULA VENKATA PRASADNo ratings yet

- PrmRptPayslipgeneral0001 PDFDocument1 pagePrmRptPayslipgeneral0001 PDFNiloy BiswasNo ratings yet