You might also like

- Instructions For Form 941 (Rev. June 2021) 1Document29 pagesInstructions For Form 941 (Rev. June 2021) 1Wen' George BeyNo ratings yet

- Trading Plan Template ContentsDocument29 pagesTrading Plan Template ContentsAndrea Davila100% (1)

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Section-By-Section Coronavirus Tax Relief MeasuresDocument4 pagesSection-By-Section Coronavirus Tax Relief MeasuresFox News80% (5)

- Contract of LeaseDocument4 pagesContract of LeaseJayvee Olayres100% (6)

- Instructions For Form 941: (Rev. March 2021)Document20 pagesInstructions For Form 941: (Rev. March 2021)Btakeshi1No ratings yet

- Introduction To Accounting - 1st Edition - Anthony WebsterDocument243 pagesIntroduction To Accounting - 1st Edition - Anthony Webstervikarun100% (2)

- RMC No.110-2020Document4 pagesRMC No.110-2020Jayvee OlayresNo ratings yet

- Withholding Tax: Taxation LawDocument21 pagesWithholding Tax: Taxation LawB-an JavelosaNo ratings yet

- BIR Ruling 555-12Document4 pagesBIR Ruling 555-12Rebecca ChanNo ratings yet

- Deduction, Collection & Recovery of TaxesDocument143 pagesDeduction, Collection & Recovery of TaxesjyotiNo ratings yet

- Revenue Regulations Digest Issued On October 15, 2020Document2 pagesRevenue Regulations Digest Issued On October 15, 2020SJ LiminNo ratings yet

- Instructions For Form CT-1: Employer's Annual Railroad Retirement Tax ReturnDocument6 pagesInstructions For Form CT-1: Employer's Annual Railroad Retirement Tax ReturnIRSNo ratings yet

- Instructions For Form CT-1: Employer's Annual Railroad Retirement Tax ReturnDocument6 pagesInstructions For Form CT-1: Employer's Annual Railroad Retirement Tax ReturnIRSNo ratings yet

- Common Questions TaxationDocument5 pagesCommon Questions TaxationChris TineNo ratings yet

- Chapter 12 Tds & TcsDocument28 pagesChapter 12 Tds & TcsRajNo ratings yet

- Bos 60408Document8 pagesBos 60408M Nidhi MallyaNo ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- Week - 2 Assignment BDocument3 pagesWeek - 2 Assignment BJulan Calo CredoNo ratings yet

- Sick Leave and Family Leave CreditDocument3 pagesSick Leave and Family Leave CreditmdcharisNo ratings yet

- Importance of Withholding Tax SystemDocument7 pagesImportance of Withholding Tax SystemALAJID, KIM EMMANUELNo ratings yet

- Final Indirect Tax ProjectDocument39 pagesFinal Indirect Tax Projectssg1015No ratings yet

- 31188sm DTL Finalnew-May-Nov14 Cp28Document66 pages31188sm DTL Finalnew-May-Nov14 Cp28gvcNo ratings yet

- DFDFDocument2 pagesDFDFVel JuneNo ratings yet

- DBM CL No. 8, S. 2019 (Employer Share On PHIC)Document3 pagesDBM CL No. 8, S. 2019 (Employer Share On PHIC)James G. DocogNo ratings yet

- Document 2710162.1Document3 pagesDocument 2710162.1achrefNo ratings yet

- Guidance For Employers Claiming Employee Retention Credit During Third and Fourth Quarters of 2021 (IR-2021-165)Document2 pagesGuidance For Employers Claiming Employee Retention Credit During Third and Fourth Quarters of 2021 (IR-2021-165)Ishaani AwasthiNo ratings yet

- Unit Number/ Heading Learning Outcomes: Intermediate Accounting Ii (Ae 16) Learning Material: Other Employee BenefitsDocument7 pagesUnit Number/ Heading Learning Outcomes: Intermediate Accounting Ii (Ae 16) Learning Material: Other Employee BenefitsJason MablesNo ratings yet

- Instructions For Form CT-1: Employer's Annual Railroad Retirement Tax ReturnDocument4 pagesInstructions For Form CT-1: Employer's Annual Railroad Retirement Tax ReturnIRSNo ratings yet

- 1601 CDocument8 pages1601 CMhyckee GuinoNo ratings yet

- Final Paper 07 - Module 03 - Chapter 15Document169 pagesFinal Paper 07 - Module 03 - Chapter 15arunNo ratings yet

- Instructions For Form CT-1: Pager/SgmlDocument6 pagesInstructions For Form CT-1: Pager/SgmlIRSNo ratings yet

- NMIMS Taxation - Assignment Answers (Sem-III)Document6 pagesNMIMS Taxation - Assignment Answers (Sem-III)Udit JoshiNo ratings yet

- TDS On Salaries - Income Tax Department, INDIADocument112 pagesTDS On Salaries - Income Tax Department, INDIAArnav MendirattaNo ratings yet

- Instructions For Form CT-1: Employer's Annual Railroad Retirement Tax ReturnDocument4 pagesInstructions For Form CT-1: Employer's Annual Railroad Retirement Tax ReturnIRSNo ratings yet

- US Internal Revenue Service: n-06-12Document6 pagesUS Internal Revenue Service: n-06-12IRSNo ratings yet

- Unit 2 Notes, Part 1Document19 pagesUnit 2 Notes, Part 1Sandip Kumar BhartiNo ratings yet

- RMC No. 120-2020Document3 pagesRMC No. 120-2020nathalie velasquezNo ratings yet

- V:Philippine Health Insurance Corporation: Remittances of Philhealth Premium ContributionsDocument3 pagesV:Philippine Health Insurance Corporation: Remittances of Philhealth Premium ContributionspogirtNo ratings yet

- 05 Frequently Asked Questions On Salary IncomeDocument5 pages05 Frequently Asked Questions On Salary IncomeSankar LoganathanNo ratings yet

- Latest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Document0 pagesLatest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Ketan ThakkarNo ratings yet

- Income Tax Amendments For May-2023Document12 pagesIncome Tax Amendments For May-2023Shubham krNo ratings yet

- OL 4 - BLT Study Text Suppliment 2021 - On New Tax AmmendmentsDocument28 pagesOL 4 - BLT Study Text Suppliment 2021 - On New Tax Ammendmentshte19031No ratings yet

- LDC Tax Practice - Employment Income Notes - November 2022 PDFDocument11 pagesLDC Tax Practice - Employment Income Notes - November 2022 PDFNathan NakibingeNo ratings yet

- Summary of Revenue Regulations Pertaining To Income TaxDocument2 pagesSummary of Revenue Regulations Pertaining To Income TaxfionnaNo ratings yet

- Tax Deducted at SourceDocument20 pagesTax Deducted at Sourceaditisrivastava0511No ratings yet

- Accounting For Employment BenefitsDocument5 pagesAccounting For Employment BenefitsiamacrusaderNo ratings yet

- Employee Benefits and Retirement PlanningDocument20 pagesEmployee Benefits and Retirement PlanningchiposityNo ratings yet

- Pansacola V CIRDocument4 pagesPansacola V CIRRB BalanayNo ratings yet

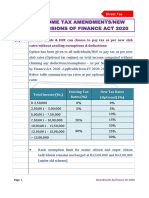

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- Chapter-9 Salary IncomeDocument21 pagesChapter-9 Salary IncomeDhrubo Chandro RoyNo ratings yet

- Questions & Answers Direct Taxes Issues On Tds Under The Head SalaryDocument4 pagesQuestions & Answers Direct Taxes Issues On Tds Under The Head Salarycgvipin8639No ratings yet

- Salary IncomeDocument83 pagesSalary IncomechitkarashellyNo ratings yet

- TDS ElaboratedDocument80 pagesTDS ElaboratedAncyNo ratings yet

- Untitled DocumentDocument4 pagesUntitled DocumentUjjawal MishraNo ratings yet

- Tds Law and Practice: Under Income Tax Act, 1961Document84 pagesTds Law and Practice: Under Income Tax Act, 1961Vaibhav ChauhanNo ratings yet

- 67908bos54451 cp15Document167 pages67908bos54451 cp15Pools KingNo ratings yet

- INTGR TAX 006 Withholding Tax On CompensationDocument4 pagesINTGR TAX 006 Withholding Tax On CompensationZatsumono YamamotoNo ratings yet

- Taxation 2 Prelim NotesDocument11 pagesTaxation 2 Prelim NotesMae TrabajoNo ratings yet

- Deduction, Collection and Recovery of Tax: After Studying This Chapter, You Would Be Able ToDocument169 pagesDeduction, Collection and Recovery of Tax: After Studying This Chapter, You Would Be Able ToRajNo ratings yet

- For Tds On SalaryDocument40 pagesFor Tds On SalarykshitijsaxenaNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- RMC No. 114-2020Document10 pagesRMC No. 114-2020Jayvee OlayresNo ratings yet

- flg-20 ?RT: Republic Philippines Department of Finance InternalDocument1 pageflg-20 ?RT: Republic Philippines Department of Finance InternalJayvee OlayresNo ratings yet

- People v. Pareja, December 9, 1996Document8 pagesPeople v. Pareja, December 9, 1996Jayvee OlayresNo ratings yet

- RR No. 28-2020Document4 pagesRR No. 28-2020Jayvee OlayresNo ratings yet

- People V Oliver, February 11, 1999Document10 pagesPeople V Oliver, February 11, 1999Jayvee OlayresNo ratings yet

- De Leon v. Esguerra, 1987Document15 pagesDe Leon v. Esguerra, 1987Jayvee OlayresNo ratings yet

- CTA Case No 8394Document16 pagesCTA Case No 8394Jayvee OlayresNo ratings yet

- Revenue Memorandum Order 26-2010Document2 pagesRevenue Memorandum Order 26-2010Jayvee OlayresNo ratings yet

- Francisco v. House of Representatives, 2003Document63 pagesFrancisco v. House of Representatives, 2003Jayvee OlayresNo ratings yet

- Buildingcode Irr PDFDocument45 pagesBuildingcode Irr PDFJayvee OlayresNo ratings yet

- Оleksii+Vlasenko 0503472695Document4 pagesОleksii+Vlasenko 0503472695Alexandra VlasiukNo ratings yet

- SBI Life ULIP News Letter April 2023Document34 pagesSBI Life ULIP News Letter April 2023Kritika ThakurNo ratings yet

- Chapter 10Document50 pagesChapter 10duy blaNo ratings yet

- Key Point Slides - Ch9Document10 pagesKey Point Slides - Ch927Winanda Setyaning KridantikaNo ratings yet

- 01 Fintech Industry Powerpoint Templates 16x9Document34 pages01 Fintech Industry Powerpoint Templates 16x9Sofyan AgustiawanNo ratings yet

- Discounted Cash Flow Model: Leesb@hanyang - Ac.krDocument2 pagesDiscounted Cash Flow Model: Leesb@hanyang - Ac.krw_fibNo ratings yet

- 5 MCQ - Professional EthicsDocument2 pages5 MCQ - Professional EthicsRAISA LIDASANNo ratings yet

- Apex Mining Co Inc - Conso AFS As of 12.13.14Document100 pagesApex Mining Co Inc - Conso AFS As of 12.13.14Ashley Ibe GuevarraNo ratings yet

- ImpactofTaxationonEconomicDevelopmentofNigeria2000 2013Document20 pagesImpactofTaxationonEconomicDevelopmentofNigeria2000 2013Made Dwi RatnadiNo ratings yet

- CLC BudgetingCashFlows 2024Document5 pagesCLC BudgetingCashFlows 2024rozoli.mlNo ratings yet

- Information Technology (PUNO)Document9 pagesInformation Technology (PUNO)Daniel Gabriel PunoNo ratings yet

- Free Sample of Portfolio OptimizationDocument37 pagesFree Sample of Portfolio Optimizationismailhasan85No ratings yet

- Money Time Relationships and Equivalence PDFDocument21 pagesMoney Time Relationships and Equivalence PDFTaga Phase 7No ratings yet

- BNI Presentation - 25 12 2018 FinalDocument13 pagesBNI Presentation - 25 12 2018 FinalNavneetNo ratings yet

- Mepco Online BilllDocument1 pageMepco Online BilllMr. ADNo ratings yet

- BBA203 Financial AccountingDocument3 pagesBBA203 Financial AccountingRajdeep KumarNo ratings yet

- Table of Contents Credit Management of IFIC Bank LTDDocument7 pagesTable of Contents Credit Management of IFIC Bank LTDTamim SikderNo ratings yet

- Corporation Bank Interview QuestionsDocument3 pagesCorporation Bank Interview QuestionssheicyNo ratings yet

- Assurance EngagementDocument6 pagesAssurance EngagementEmmaNo ratings yet

- Risk Assessment and Risk Management PlanDocument2 pagesRisk Assessment and Risk Management PlanWilvic Jan GacitaNo ratings yet

- Implementing Risk Based Internal Audit in Indian Banks: An Assessment of Organizational PreparednessDocument19 pagesImplementing Risk Based Internal Audit in Indian Banks: An Assessment of Organizational Preparednessnasir_m68No ratings yet

- Final Report of Engro PDF FreeDocument58 pagesFinal Report of Engro PDF FreeMadni Enterprises DGKNo ratings yet

- Annuities Modeling With R: Giorgio Alfredo Spedicato, PH.D C.Stat ACASDocument34 pagesAnnuities Modeling With R: Giorgio Alfredo Spedicato, PH.D C.Stat ACAScyrine rienNo ratings yet

- CH 3Document45 pagesCH 3Ella ApeloNo ratings yet

- West Bengal Student Credit Card SchemeDocument17 pagesWest Bengal Student Credit Card SchemeSwapnanil GuinNo ratings yet

- Chapter 11 17Document62 pagesChapter 11 17Melissa Cabigat Abdul KarimNo ratings yet

- Credit Access Grameen Limited IPO Note-201808071226511901045Document16 pagesCredit Access Grameen Limited IPO Note-201808071226511901045Arvind KumarNo ratings yet

- TestReviewer Docx LDocument27 pagesTestReviewer Docx LCes100% (1)