You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- 0105 SC Supreme Court Abortion RulingDocument147 pages0105 SC Supreme Court Abortion RulingWLTXNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Wisconsin Special Counsel Gableman Election Integrity Investigation Interim ReportDocument25 pagesWisconsin Special Counsel Gableman Election Integrity Investigation Interim ReportUncoverDCNo ratings yet

- Lawsuit From Greg YoungDocument11 pagesLawsuit From Greg YoungElizaNo ratings yet

- Constitution and By-Laws: Christian Women'S AssociationDocument12 pagesConstitution and By-Laws: Christian Women'S AssociationDarren CariñoNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- AP US Government and Politics SGDocument68 pagesAP US Government and Politics SGLovejosaayNo ratings yet

- Heir SharesDocument232 pagesHeir SharesRascille LaranasNo ratings yet

- Comprehensive Agrarian Reform LawDocument22 pagesComprehensive Agrarian Reform LawRascille LaranasNo ratings yet

- Marksville Police LawsuitDocument53 pagesMarksville Police Lawsuittom clearyNo ratings yet

- The Vedic PropheciesDocument152 pagesThe Vedic PropheciesNill Salunke100% (1)

- The Law The Money and Your Choice Lee BrobstDocument0 pagesThe Law The Money and Your Choice Lee BrobstGreg Ward100% (1)

- Motion To StayDocument10 pagesMotion To StayAnonymous Pb39klJNo ratings yet

- James Kilpatrick - The Sovereign StatesDocument210 pagesJames Kilpatrick - The Sovereign StatesJohn SutherlandNo ratings yet

- States V Us and States Compl 2021-11-23Document82 pagesStates V Us and States Compl 2021-11-23Washington Examiner100% (1)

- Labor Relations Case Digest CompilationDocument3 pagesLabor Relations Case Digest CompilationPraisah Marjorey PicotNo ratings yet

- Adofo and Others V Attorney-General and AnotherDocument12 pagesAdofo and Others V Attorney-General and AnotherMusah YahayaNo ratings yet

- Rules of Evidence Reviewer 2nd ExamDocument11 pagesRules of Evidence Reviewer 2nd ExamRascille LaranasNo ratings yet

- New York Convention of 1958 OverviewDocument22 pagesNew York Convention of 1958 OverviewminchanmonNo ratings yet

- COA-Alabel Audit Report2019Document130 pagesCOA-Alabel Audit Report2019Rascille LaranasNo ratings yet

- Gonzales III V Office of The President Case DigestDocument3 pagesGonzales III V Office of The President Case DigestKarmaranthNo ratings yet

- International Humanitarian LawDocument10 pagesInternational Humanitarian LawRascille LaranasNo ratings yet

- Staff of The White HouseDocument34 pagesStaff of The White HouseRascille LaranasNo ratings yet

- Privileges and ResponsibilitiesDocument6 pagesPrivileges and ResponsibilitiesRascille LaranasNo ratings yet

- Reciprocal WorkingDocument12 pagesReciprocal WorkingRascille LaranasNo ratings yet

- Decade of DisastersDocument27 pagesDecade of DisastersRascille LaranasNo ratings yet

- Com - Shares of Heir - DigestsDocument185 pagesCom - Shares of Heir - DigestsRascille LaranasNo ratings yet

- 211589-Article Text-524003-1-10-20210730Document9 pages211589-Article Text-524003-1-10-20210730Rascille LaranasNo ratings yet

- Maglasang Vs CabatinganDocument5 pagesMaglasang Vs CabatinganRascille LaranasNo ratings yet

- COA-SaranganiPov2019 Audit ReportDocument186 pagesCOA-SaranganiPov2019 Audit ReportRascille LaranasNo ratings yet

- Palarong PambansaDocument18 pagesPalarong PambansaRascille LaranasNo ratings yet

- Compiled Cases On Intestate Judicial AdministrationDocument95 pagesCompiled Cases On Intestate Judicial AdministrationRascille LaranasNo ratings yet

- Notes For Revelation 21Document4 pagesNotes For Revelation 21Rascille LaranasNo ratings yet

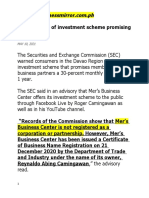

- Ponzi-Scheme: SEC Advisory On Mer'sDocument3 pagesPonzi-Scheme: SEC Advisory On Mer'sRascille LaranasNo ratings yet

- CIR v. PAL, GR No180066Document12 pagesCIR v. PAL, GR No180066Rascille LaranasNo ratings yet

- COA-Sarangani2018 Audit ReportDocument202 pagesCOA-Sarangani2018 Audit ReportRascille LaranasNo ratings yet

- List of ETEEAP-Dep HEIs and Their Program Offerings - Revised July 2019Document2 pagesList of ETEEAP-Dep HEIs and Their Program Offerings - Revised July 2019Rascille LaranasNo ratings yet

- San Pablo v. CIR, GR 147749, 22 June 2006Document6 pagesSan Pablo v. CIR, GR 147749, 22 June 2006Rascille LaranasNo ratings yet

- Alta Vista Golf v. The City of Cebu, GR 180235, 20 Jan 2016Document15 pagesAlta Vista Golf v. The City of Cebu, GR 180235, 20 Jan 2016Rascille LaranasNo ratings yet

- Gulf Air Company v. CIR, GR 182045, 19 September 2012Document7 pagesGulf Air Company v. CIR, GR 182045, 19 September 2012Rascille LaranasNo ratings yet

- CIR v. Fortune Tobacco GR Nos 167274-75, 21 July 2008Document12 pagesCIR v. Fortune Tobacco GR Nos 167274-75, 21 July 2008Rascille LaranasNo ratings yet

- Commands To (Constitutional Officer Sheriff Bouchard) To Secure The Three (3) Unrebutted Affidavits of Sacred Allodial Indigenous Land Property Titles and Repossessions.Document205 pagesCommands To (Constitutional Officer Sheriff Bouchard) To Secure The Three (3) Unrebutted Affidavits of Sacred Allodial Indigenous Land Property Titles and Repossessions.Sharon A. Morris BeyNo ratings yet

- As A Future Teacher, Write A Reaction Paper of Not Less Than 100 Words, About This TopicDocument4 pagesAs A Future Teacher, Write A Reaction Paper of Not Less Than 100 Words, About This TopiclorenzoNo ratings yet

- Decree 15-2021 ND-CP MANAGEMENT OF CONSTRUCTION PROJECTSDocument85 pagesDecree 15-2021 ND-CP MANAGEMENT OF CONSTRUCTION PROJECTSHanh BuiNo ratings yet

- Reyes V ITC - ITC Original AnswerDocument6 pagesReyes V ITC - ITC Original AnswerAnonymous pPSymSvyNo ratings yet

- Article I of The Us Constitution Guiding QuestionsDocument2 pagesArticle I of The Us Constitution Guiding Questionsapi-262416934No ratings yet

- COLREGS - International Regulations For Preventing Collisions at SeaDocument74 pagesCOLREGS - International Regulations For Preventing Collisions at SeaBisratNo ratings yet

- John Marshall and The Bank Case: Mcculloch V. Maryland (1819)Document4 pagesJohn Marshall and The Bank Case: Mcculloch V. Maryland (1819)Helen Joy F. Javier - AdvientoNo ratings yet

- Stern vs. Levine & City of Miami BeachDocument10 pagesStern vs. Levine & City of Miami BeachGrant SternNo ratings yet

- Labstand Compiled Set of Case DoctrinesDocument33 pagesLabstand Compiled Set of Case DoctrinesTeam2KissNo ratings yet

- TTP - Teachers' Code of EthicsDocument7 pagesTTP - Teachers' Code of EthicsDahlz RodriguezNo ratings yet

- Rhinebeck Town Proposed Zoning Law CH A136Document410 pagesRhinebeck Town Proposed Zoning Law CH A136Kerri KarvetskiNo ratings yet

- United States Court of Appeals, Fourth CircuitDocument12 pagesUnited States Court of Appeals, Fourth CircuitScribd Government DocsNo ratings yet

- Little Valley Fire Motion To DismissDocument19 pagesLittle Valley Fire Motion To DismissOlivia DeGennaroNo ratings yet

- House Ways and Means ComplaintDocument172 pagesHouse Ways and Means ComplaintdarrenkaplanNo ratings yet

- Separation of Power 2Document23 pagesSeparation of Power 2muhammad tararNo ratings yet