You might also like

- Comprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeFrom EverandComprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeRating: 5 out of 5 stars5/5 (1)

- Planning Kaplan Chapter 6: Acca Paper F8 Int Audit and AssuranceDocument38 pagesPlanning Kaplan Chapter 6: Acca Paper F8 Int Audit and Assurancehaddad2020No ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- At.3207-Considering Materiality and Audit RiskDocument5 pagesAt.3207-Considering Materiality and Audit RiskDenny June CraususNo ratings yet

- Information Systems Auditing: The IS Audit Reporting ProcessFrom EverandInformation Systems Auditing: The IS Audit Reporting ProcessRating: 4.5 out of 5 stars4.5/5 (3)

- Updated Slides Introducing The Conceptual FrameworkDocument24 pagesUpdated Slides Introducing The Conceptual FrameworkHunal Kumar MautadinNo ratings yet

- F8-17 Accounting EstimatesDocument10 pagesF8-17 Accounting EstimatesReever RiverNo ratings yet

- Lecture 21 - Standards On Auditing (SA 320 and 402) PDFDocument6 pagesLecture 21 - Standards On Auditing (SA 320 and 402) PDFAruna RajappaNo ratings yet

- AT.109 - Materiality and RisksDocument7 pagesAT.109 - Materiality and Risksandrew dacullaNo ratings yet

- F8-30 The Auditor's Report On Financial StatementsDocument18 pagesF8-30 The Auditor's Report On Financial StatementsReever RiverNo ratings yet

- AT - Materiality and RisksDocument7 pagesAT - Materiality and RisksRey Joyce AbuelNo ratings yet

- Pre0131 Midterm Reviewer - Pdf-MaterialityDocument2 pagesPre0131 Midterm Reviewer - Pdf-MaterialityEliny CruzNo ratings yet

- Resumen Capitulo 2Document4 pagesResumen Capitulo 2Lucho EnriqueNo ratings yet

- Nature of AccountingDocument39 pagesNature of AccountinghotpokerchipsNo ratings yet

- Conceptual Frame Work-CAP IIDocument9 pagesConceptual Frame Work-CAP IIbinuNo ratings yet

- Cfas Chapter 2Document55 pagesCfas Chapter 2Lance Lenard Divinagracia Calimpos100% (1)

- Materiality, Misstatements and Reporting Part I: ISA Implementation Support ModuleDocument14 pagesMateriality, Misstatements and Reporting Part I: ISA Implementation Support ModulelloydNo ratings yet

- Going Concern: Session 31Document14 pagesGoing Concern: Session 31Abdullah EjazNo ratings yet

- Cost Accounting (Chapter 1-3)Document5 pagesCost Accounting (Chapter 1-3)eunice0% (1)

- Accounting 1Document146 pagesAccounting 1Touhidul IslamNo ratings yet

- Audit Planning: Auditor's Main ObjectiveDocument7 pagesAudit Planning: Auditor's Main Objectivemarie aniceteNo ratings yet

- Planning The Audit and Development of Audit StrategyDocument38 pagesPlanning The Audit and Development of Audit StrategyReyna Mae ZamoraNo ratings yet

- Investing and Financing Decisions and The Balance SheetDocument57 pagesInvesting and Financing Decisions and The Balance Sheetd-fbuser-57033070No ratings yet

- IAASB ISA 315 Revised 2019Document16 pagesIAASB ISA 315 Revised 2019Bianca Marie PedrozoNo ratings yet

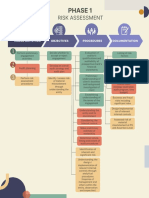

- Phase I-Risk Assessment Planning The AudDocument21 pagesPhase I-Risk Assessment Planning The AudGelyn CruzNo ratings yet

- Rapid Review Kieso v1Document12 pagesRapid Review Kieso v1mehmood981460No ratings yet

- Acctg 14 - Midterm Lesson Part3Document21 pagesAcctg 14 - Midterm Lesson Part3NANNo ratings yet

- Chapter 3: Sampling & Materiality: SA 320 - Materiality in Planning & Performing An AuditDocument14 pagesChapter 3: Sampling & Materiality: SA 320 - Materiality in Planning & Performing An AuditlohitacademyNo ratings yet

- Kieso, Weygandt, WarfieldDocument56 pagesKieso, Weygandt, WarfieldShevina Maghari shsnohsNo ratings yet

- Status and Purpose of The Framework, Objective and Qualitative CharacteristicsDocument35 pagesStatus and Purpose of The Framework, Objective and Qualitative CharacteristicsCharmaine Mari OlmosNo ratings yet

- Framework For Accounting & ReportingDocument32 pagesFramework For Accounting & ReportingJason InufiNo ratings yet

- Aa CH10Document26 pagesAa CH10Thuỳ DươngNo ratings yet

- LS 2.90 - PSA 320 Materiality in The Planning and Performing An AuditDocument6 pagesLS 2.90 - PSA 320 Materiality in The Planning and Performing An AuditSkye Lee100% (1)

- Audit and Assurance PrincipleDocument2 pagesAudit and Assurance PrincipleIsabell CastroNo ratings yet

- GROUP 8 - Risk AssessmentDocument1 pageGROUP 8 - Risk AssessmentRhad Lester C. MaestradoNo ratings yet

- Module 1 AUDIT PLANNINGDocument3 pagesModule 1 AUDIT PLANNINGLady BirdNo ratings yet

- "Plans Are Worthless But Planning Is Everything." - Dwight D. EisenhowerDocument4 pages"Plans Are Worthless But Planning Is Everything." - Dwight D. EisenhowerLady BirdNo ratings yet

- The Concept MaterialityDocument27 pagesThe Concept MaterialityemeraldNo ratings yet

- Topic 2 - Conceptual FrameworkDocument36 pagesTopic 2 - Conceptual FrameworkA2T5 Haziqah HousnaNo ratings yet

- 2 Financial Reporting Theory UpdatedDocument52 pages2 Financial Reporting Theory UpdatedSiham OsmanNo ratings yet

- Chapter 2: The Conceptual FrameworkDocument36 pagesChapter 2: The Conceptual FrameworkNida Mohammad Khan AchakzaiNo ratings yet

- Chapter 2 Aau Understanding Materiality Context Financial StatementsDocument4 pagesChapter 2 Aau Understanding Materiality Context Financial StatementsDaysonNo ratings yet

- Basel II Capital Accord SlidesDocument25 pagesBasel II Capital Accord SlidesAamir RazaNo ratings yet

- Lu - Valuation Challenges Credit Institutions Investment Firms - 03072015Document17 pagesLu - Valuation Challenges Credit Institutions Investment Firms - 03072015Simon AltkornNo ratings yet

- Lecture 1Document38 pagesLecture 1Preet LohanaNo ratings yet

- Audit of Financial StatementsDocument69 pagesAudit of Financial StatementsFazlihaq DurraniNo ratings yet

- 1 - Overview of AuditingDocument13 pages1 - Overview of AuditingZooeyNo ratings yet

- F2-17 Capital Budgeting and Discounted Cash Flows PDFDocument28 pagesF2-17 Capital Budgeting and Discounted Cash Flows PDFJaved ImranNo ratings yet

- CR November 2020 Mark PlanDocument31 pagesCR November 2020 Mark PlanZaid AhmadNo ratings yet

- Revised CF Webcast Slides April 2018Document16 pagesRevised CF Webcast Slides April 2018drew aranasNo ratings yet

- Summary NotesDocument2 pagesSummary NotesFar100% (1)

- Standards and The Conceptual Framework Underlying Financial AccountingDocument26 pagesStandards and The Conceptual Framework Underlying Financial AccountingLodovicus LasdiNo ratings yet

- Chap 4 - Audit Planning P2Document14 pagesChap 4 - Audit Planning P2hangNo ratings yet

- Forensic Investigation - ReportDocument6 pagesForensic Investigation - Reportjhon DavidNo ratings yet

- COA R2019-016 AnnexA GuidelinesDocument56 pagesCOA R2019-016 AnnexA Guidelinesbislig water district67% (3)

- Auditing & Assurance MAC005 Trimester 2 2020 ASSIGNMENTDocument8 pagesAuditing & Assurance MAC005 Trimester 2 2020 ASSIGNMENTKarma SherpaNo ratings yet

- Chapter 2 - Framework - Edited Oct 2022Document26 pagesChapter 2 - Framework - Edited Oct 2022Kim AlyaNo ratings yet

- Welcome To Acc721: Framework For Accounting & ReportingDocument30 pagesWelcome To Acc721: Framework For Accounting & ReportingJason InufiNo ratings yet

- Chapter 2: The Conceptual Framework: Fundamentals of Intermediate Accounting Weygandt, Kieso, and WarfieldDocument36 pagesChapter 2: The Conceptual Framework: Fundamentals of Intermediate Accounting Weygandt, Kieso, and WarfieldMohammed Akhtab Ul HudaNo ratings yet

- External Audit: Session 2Document20 pagesExternal Audit: Session 2Abdullah EjazNo ratings yet

- Non-Current Asse TS: Session 22Document14 pagesNon-Current Asse TS: Session 22Abdullah EjazNo ratings yet

- Using The Work of An Expert: Session 18Document12 pagesUsing The Work of An Expert: Session 18Abdullah EjazNo ratings yet

- Tests of Control: Session 12Document40 pagesTests of Control: Session 12Abdullah EjazNo ratings yet

- Internal Audit: Session 32Document26 pagesInternal Audit: Session 32Abdullah EjazNo ratings yet

- Going Concern: Session 31Document14 pagesGoing Concern: Session 31Abdullah EjazNo ratings yet

- Inventory: Session 23Document22 pagesInventory: Session 23Abdullah EjazNo ratings yet

- 5154 Articles (SBR) Examiners Approach v3Document4 pages5154 Articles (SBR) Examiners Approach v3Htoo HtooNo ratings yet

- Day 1 - Capital Gain TaxDocument20 pagesDay 1 - Capital Gain TaxAbdullah EjazNo ratings yet

- ACCA Exam Approach Webinars September 2020Document3 pagesACCA Exam Approach Webinars September 2020Abdullah EjazNo ratings yet

- Questoin 1Document6 pagesQuestoin 1Abdullah EjazNo ratings yet

- Examiner's Report: Strategic Business Reporting (SBR) July 2020Document7 pagesExaminer's Report: Strategic Business Reporting (SBR) July 2020OzzNo ratings yet

- Question - September 2018 BackgroundDocument6 pagesQuestion - September 2018 BackgroundAbdullah EjazNo ratings yet

- Day 1Document11 pagesDay 1Abdullah EjazNo ratings yet

- Details of Sample Watches-Converted (Version 1)Document4 pagesDetails of Sample Watches-Converted (Version 1)Abdullah EjazNo ratings yet

- Retriever June 13Document3 pagesRetriever June 13Abdullah EjazNo ratings yet

- Lark Dec 12Document3 pagesLark Dec 12Abdullah EjazNo ratings yet

- Retriever June 13Document3 pagesRetriever June 13Abdullah EjazNo ratings yet

- Quiz 1 - ACGN PrelimsDocument9 pagesQuiz 1 - ACGN Prelimsnatalie clyde matesNo ratings yet

- Some of The Accounting Recits PointersDocument7 pagesSome of The Accounting Recits PointersJoseNo ratings yet

- Ienergizer Limited 31 March 2019 Execution VersionDocument85 pagesIenergizer Limited 31 March 2019 Execution VersionzvetibaNo ratings yet

- Exam Techniques Articles - Part 2 - Risk - Part 3 - Accounting Issues PDFDocument18 pagesExam Techniques Articles - Part 2 - Risk - Part 3 - Accounting Issues PDFLoveluHoqueNo ratings yet

- At-03: Financial Statements Audits - OverviewDocument70 pagesAt-03: Financial Statements Audits - OverviewMae Danica CalunsagNo ratings yet

- Auditing Theory Chapter 9 Summary NotesDocument10 pagesAuditing Theory Chapter 9 Summary NotesJwyneth Royce DenolanNo ratings yet

- Chapter 8 Con .: Audit Planning and Analytical ProceduresDocument15 pagesChapter 8 Con .: Audit Planning and Analytical Proceduresاحمد العربيNo ratings yet

- International Standard On Auditing (UK) 530: Audit SamplingDocument16 pagesInternational Standard On Auditing (UK) 530: Audit SamplingTaehyung KimNo ratings yet

- Chapter 4 Accounting Concepts and PrinciplesDocument14 pagesChapter 4 Accounting Concepts and PrinciplesAngellouiza MatampacNo ratings yet

- Refference Book 2Document77 pagesRefference Book 2ahmed hindiNo ratings yet

- CFASDocument17 pagesCFASKie Magracia BustillosNo ratings yet

- @catatan Audit Siap MidDocument31 pages@catatan Audit Siap MidEarly Saputra100% (1)

- CFASDocument19 pagesCFASKuroko TetsuyaNo ratings yet

- Audit Handbook For MFIDocument96 pagesAudit Handbook For MFIChirag Vasa100% (1)

- Statutory Audit ChecklistDocument7 pagesStatutory Audit ChecklistRanganathan NRGNo ratings yet

- 1) AFC Club Licensing RegulationsDocument68 pages1) AFC Club Licensing RegulationssaidNo ratings yet

- Auditing TheoryDocument13 pagesAuditing TheoryJamaica DavidNo ratings yet

- Chap 006Document28 pagesChap 006Rafael GarciaNo ratings yet

- Salamatu Chapter 1 3Document33 pagesSalamatu Chapter 1 3Ishmael FofanahNo ratings yet

- Account MCQ PDFDocument93 pagesAccount MCQ PDFsunil kalura100% (1)

- At.2506 Determining MaterialityDocument26 pagesAt.2506 Determining Materialityawesome bloggersNo ratings yet

- Week 5 & 6 Risk Assessment and ResponseDocument53 pagesWeek 5 & 6 Risk Assessment and ResponsefauziahezzyNo ratings yet

- Making Materiality Judgment Practice StatementDocument48 pagesMaking Materiality Judgment Practice StatementwellawalalasithNo ratings yet

- Efficiency GuidanceDocument25 pagesEfficiency GuidanceSalauddin Kader ACCANo ratings yet

- Audit Questions 6Document20 pagesAudit Questions 6Humayun KhanNo ratings yet

- Chapter 3 SolutionsDocument15 pagesChapter 3 Solutionsjohn brown100% (1)

- Aud689 Advanced Auditing Exam February 2021 Suggested SolutionsDocument10 pagesAud689 Advanced Auditing Exam February 2021 Suggested SolutionsAKMAL ASYRAF BIN HASHIM (MOH)No ratings yet

- Auditing Theory 3rd Examination (Answer Key)Document13 pagesAuditing Theory 3rd Examination (Answer Key)KathleenNo ratings yet

- Audit Procedure: A Case Study On ACNABIN-Chartered AccountantsDocument18 pagesAudit Procedure: A Case Study On ACNABIN-Chartered AccountantsAdnanNo ratings yet

- Final Exam AADocument29 pagesFinal Exam AAFungai MajuriraNo ratings yet

- A Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowFrom EverandA Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowNo ratings yet

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideFrom Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideRating: 2.5 out of 5 stars2.5/5 (2)

- Business Process Mapping: Improving Customer SatisfactionFrom EverandBusiness Process Mapping: Improving Customer SatisfactionRating: 5 out of 5 stars5/5 (1)

- Bribery and Corruption Casebook: The View from Under the TableFrom EverandBribery and Corruption Casebook: The View from Under the TableNo ratings yet

- Guide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyFrom EverandGuide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyNo ratings yet

- Audit. Review. Compilation. What's the Difference?From EverandAudit. Review. Compilation. What's the Difference?Rating: 5 out of 5 stars5/5 (1)

- The Layman's Guide GDPR Compliance for Small Medium BusinessFrom EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessRating: 5 out of 5 stars5/5 (1)

- Frequently Asked Questions in International Standards on AuditingFrom EverandFrequently Asked Questions in International Standards on AuditingRating: 1 out of 5 stars1/5 (1)

- GDPR for DevOp(Sec) - The laws, Controls and solutionsFrom EverandGDPR for DevOp(Sec) - The laws, Controls and solutionsRating: 5 out of 5 stars5/5 (1)

- Scrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsFrom EverandScrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsNo ratings yet

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersFrom EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersRating: 4.5 out of 5 stars4.5/5 (11)

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekFrom EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekNo ratings yet

- Audit and Assurance Essentials: For Professional Accountancy ExamsFrom EverandAudit and Assurance Essentials: For Professional Accountancy ExamsNo ratings yet

- Financial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksFrom EverandFinancial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksRating: 4 out of 5 stars4/5 (1)

- Executive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceFrom EverandExecutive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceRating: 4 out of 5 stars4/5 (1)