You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Chapter Two-Foundation of Individual Behavior and Learning in An OrganizationDocument16 pagesChapter Two-Foundation of Individual Behavior and Learning in An OrganizationMikias DegwaleNo ratings yet

- Chapter Three Foundation of Group Behavior: 1.1. Defining and Classifying Team And/or GroupDocument15 pagesChapter Three Foundation of Group Behavior: 1.1. Defining and Classifying Team And/or GroupMikias DegwaleNo ratings yet

- Chapter Three Foundation of Group Behavior: 1.1. Defining and Classifying Team And/or GroupDocument17 pagesChapter Three Foundation of Group Behavior: 1.1. Defining and Classifying Team And/or GroupMikias DegwaleNo ratings yet

- CH 01Document13 pagesCH 01Mikias DegwaleNo ratings yet

- 1.1. What Is Stress?: Chapter Six-Stress ManagementDocument6 pages1.1. What Is Stress?: Chapter Six-Stress ManagementMikias DegwaleNo ratings yet

- Chapter Seven-Organizational Culture and DiversityDocument7 pagesChapter Seven-Organizational Culture and DiversityMikias Degwale100% (1)

- Chapter Two-Foundation of Individual Behavior and Learning in An OrganizationDocument14 pagesChapter Two-Foundation of Individual Behavior and Learning in An OrganizationMikias DegwaleNo ratings yet

- Chapter Three: Dividend Decision/PolicyDocument38 pagesChapter Three: Dividend Decision/PolicyMikias DegwaleNo ratings yet

- Chapter Eight - Power and Politics in An OrganizationDocument4 pagesChapter Eight - Power and Politics in An OrganizationMikias DegwaleNo ratings yet

- Chapter Five Part One: Business ValuationDocument57 pagesChapter Five Part One: Business ValuationMikias Degwale100% (1)

- Chapter Two: Financing Decisions / Capital StructureDocument72 pagesChapter Two: Financing Decisions / Capital StructureMikias DegwaleNo ratings yet

- Chapter Four: Investment/Project Appraisal - Capital BudgetingDocument40 pagesChapter Four: Investment/Project Appraisal - Capital BudgetingMikias DegwaleNo ratings yet

- Registering For VATDocument1 pageRegistering For VATMikias DegwaleNo ratings yet

- Advanced Corporate Finance (ACFN - 551) (Credit Hours: 3) : Departmet of Accounting and FinanceDocument85 pagesAdvanced Corporate Finance (ACFN - 551) (Credit Hours: 3) : Departmet of Accounting and FinanceMikias DegwaleNo ratings yet

- Chapter Four Financial Markets in The Financial SystemDocument66 pagesChapter Four Financial Markets in The Financial SystemMikias DegwaleNo ratings yet

- Chapter Five Regulation of Financial Markets and Institutions and Financial InnovationDocument22 pagesChapter Five Regulation of Financial Markets and Institutions and Financial InnovationMikias DegwaleNo ratings yet

- Financial Institutions and Market: (ACFN, 2 Credit Hour)Document25 pagesFinancial Institutions and Market: (ACFN, 2 Credit Hour)Mikias DegwaleNo ratings yet

- Chapter Six: Risk Management in Financial InstitutionsDocument22 pagesChapter Six: Risk Management in Financial InstitutionsMikias DegwaleNo ratings yet

- Raw Materials InventoryDocument4 pagesRaw Materials InventoryMikias DegwaleNo ratings yet

- Chapter Five: Interest Rate Determination and Bond ValuationDocument38 pagesChapter Five: Interest Rate Determination and Bond ValuationMikias DegwaleNo ratings yet

- Debre Markos Universty College of Post-Graduate Studies Department of Accounting and FinanceDocument14 pagesDebre Markos Universty College of Post-Graduate Studies Department of Accounting and FinanceMikias DegwaleNo ratings yet

- Chapter Three Financial Institutions in The Financial SystemDocument9 pagesChapter Three Financial Institutions in The Financial SystemMikias DegwaleNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

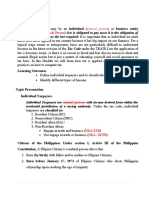

- Classification of Individual TaxpayerDocument4 pagesClassification of Individual TaxpayerJj helterbrandNo ratings yet

- House No.D-9, Block N, North Nazimabad, Karachi Central North Nazimabad Town Imran Bashir CHDocument2 pagesHouse No.D-9, Block N, North Nazimabad, Karachi Central North Nazimabad Town Imran Bashir CHMIRZA AKHTAR ALINo ratings yet

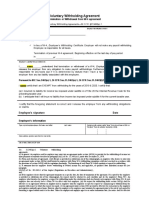

- Voluntary Withholding Agreement: Termination or Withdrawal From W-4 AgreementDocument2 pagesVoluntary Withholding Agreement: Termination or Withdrawal From W-4 Agreementkildea90% (20)

- Withholding Tax On Rental Services: Guide 01Document2 pagesWithholding Tax On Rental Services: Guide 01Abdul NafiNo ratings yet

- Commissioner of Internal Revenue Vs Soriano y CIADocument1 pageCommissioner of Internal Revenue Vs Soriano y CIAAmor5678No ratings yet

- Salary Slip (32119327 April, 2019)Document1 pageSalary Slip (32119327 April, 2019)Hassan RanaNo ratings yet

- IRS Reporting Requirements For Offshore Trusts and Foreign LLCDocument2 pagesIRS Reporting Requirements For Offshore Trusts and Foreign LLCed_nyc100% (1)

- W8-Eci 2021-06-01 Preview DocDocument1 pageW8-Eci 2021-06-01 Preview Docfuture warriorNo ratings yet

- Army Institute of Law, Mohali: Provisions Relating To Rebates Under The Income Tax Act, 1961 A Project Submitted ToDocument7 pagesArmy Institute of Law, Mohali: Provisions Relating To Rebates Under The Income Tax Act, 1961 A Project Submitted ToAyushi JaryalNo ratings yet

- Sales InvoicesDocument1 pageSales InvoicesMayank ManiNo ratings yet

- As485070 Dec2022 PayslipDocument2 pagesAs485070 Dec2022 PayslipAKM Enterprises Pvt LtdNo ratings yet

- You Have Opted For Old Tax RegimeDocument2 pagesYou Have Opted For Old Tax RegimeRamsheed Ashraf100% (1)

- Quotation QU100949Document1 pageQuotation QU100949LesegoNo ratings yet

- Salary Details For 06/2020: Earnings Code Description Source AmountDocument1 pageSalary Details For 06/2020: Earnings Code Description Source AmountHomi NathNo ratings yet

- SYLLABUS Tax FOR 2023 BARDocument3 pagesSYLLABUS Tax FOR 2023 BARJournal SP DabawNo ratings yet

- Cir vs. CA and Anscor, G.R. No. 108576, January 20. 1999Document2 pagesCir vs. CA and Anscor, G.R. No. 108576, January 20. 1999Ayra CadigalNo ratings yet

- Uma Salary Slip JulyDocument1 pageUma Salary Slip Julyjyothi sNo ratings yet

- Reinforcement in Business TaxationDocument24 pagesReinforcement in Business TaxationTulungan Para sa Modular at Online Classes0% (1)

- Pay Slip - 604316 - Mar-23Document1 pagePay Slip - 604316 - Mar-23ArchanaNo ratings yet

- State Tax FormDocument2 pagesState Tax FormSaintjinx21No ratings yet

- Aguinaldo Industries V CirDocument1 pageAguinaldo Industries V CirChristine JacintoNo ratings yet

- SAJ-Sales Quotation - 10-Sep-2022Document2 pagesSAJ-Sales Quotation - 10-Sep-2022Michael NjugunaNo ratings yet

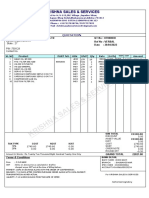

- RV ICE S: Krishna Sales & ServicesDocument1 pageRV ICE S: Krishna Sales & ServicesSaikatNo ratings yet

- Instructions For Schedule R (Form 941) : (Rev. June 2021)Document3 pagesInstructions For Schedule R (Form 941) : (Rev. June 2021)Josh JasperNo ratings yet

- Rajasthan - State FormatDocument9 pagesRajasthan - State FormatvjvksNo ratings yet

- Rian Inc Proforma Invoice 2019-2020Document2 pagesRian Inc Proforma Invoice 2019-2020Saurabh GujratiNo ratings yet

- Income Tax Calculator 2023Document50 pagesIncome Tax Calculator 2023Pani NiNo ratings yet

- ACT Internet BillDocument3 pagesACT Internet BillPradeep N KNo ratings yet

- GST CouncilDocument2 pagesGST CouncilMilind SwaroopNo ratings yet

- Home TestDocument22 pagesHome TestSelina ChenNo ratings yet