You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Example CDCT Appendix 25Document53 pagesExample CDCT Appendix 25Osama AshourNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

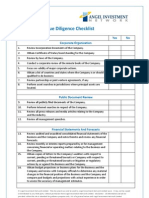

- Due Diligence ChecklistDocument10 pagesDue Diligence ChecklistVikasdeep SharmaNo ratings yet

- Austin Custom Brass MouthpiecesDocument4 pagesAustin Custom Brass MouthpiecesÍtalo R. H. FerroNo ratings yet

- Harrods Development PlansDocument8 pagesHarrods Development PlansAsghar AbbasNo ratings yet

- Privacy Persuasive EssayDocument3 pagesPrivacy Persuasive Essayapi-251934738No ratings yet

- What Is ProductivityDocument12 pagesWhat Is ProductivityAsghar AbbasNo ratings yet

- Ferrarri DetailedDocument35 pagesFerrarri DetailedAsghar AbbasNo ratings yet

- Ferrari Analysis and PastDocument2 pagesFerrari Analysis and PastAsghar AbbasNo ratings yet

- Android Application Secure Design/Secure Coding GuidebookDocument385 pagesAndroid Application Secure Design/Secure Coding GuidebookFrancesco Bicco Iberite100% (1)

- Eco Project ReportDocument21 pagesEco Project Reportswapnil_thakre_1No ratings yet

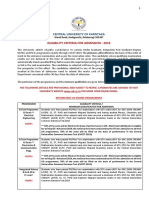

- Eligibility CriteriaDocument13 pagesEligibility CriteriaArnab SahaNo ratings yet

- Tecco System: Ruvolum Workshop - Armin RodunerDocument95 pagesTecco System: Ruvolum Workshop - Armin RodunerNam TrinhNo ratings yet

- MM OverlordDocument6 pagesMM OverlordIsiahTanEdquibanNo ratings yet

- Resources DTDocument8 pagesResources DTDicky AfrizalNo ratings yet

- Cell As A Unit of Life (Science Form 1 - Short Notes)Document2 pagesCell As A Unit of Life (Science Form 1 - Short Notes)jrpyroNo ratings yet

- Test1 Test2 Test3 MergedDocument9 pagesTest1 Test2 Test3 Merged1081PARTH CHATTERJEENo ratings yet

- Case Studies On Major Concepts: PerfusionDocument37 pagesCase Studies On Major Concepts: PerfusionJek Dela CruzNo ratings yet

- Doanh Nhan Sai Gon 2016Document24 pagesDoanh Nhan Sai Gon 2016Chung NguyễnNo ratings yet

- Iec 62305 1 7Document7 pagesIec 62305 1 7Hamza AHMED SAADINo ratings yet

- XXX XXX Open Source Designing Ceed: Sub SectionDocument3 pagesXXX XXX Open Source Designing Ceed: Sub SectionnashpdNo ratings yet

- Confined Space Safety ChecklistDocument2 pagesConfined Space Safety ChecklistOul-kr Oul-krNo ratings yet

- Purisima vs. Lazatin (November 29, 2016)Document22 pagesPurisima vs. Lazatin (November 29, 2016)Clarinda MerleNo ratings yet

- Traffic Engineering Determination of Optimum Cycle length-IRC MethodDocument6 pagesTraffic Engineering Determination of Optimum Cycle length-IRC MethodNishanth NishiNo ratings yet

- Kushal Kala: Treasuring, Managing and Rewarding People Towards BettermentDocument9 pagesKushal Kala: Treasuring, Managing and Rewarding People Towards BettermentManigandan SrinivasaNo ratings yet

- 9 M Carrying Out Animal Husbandry Practice and Farm ManagementDocument127 pages9 M Carrying Out Animal Husbandry Practice and Farm ManagementEndash HaileNo ratings yet

- Key Check 3:: Practiced Synchronous Planting After A Rest PeriodDocument18 pagesKey Check 3:: Practiced Synchronous Planting After A Rest PeriodFroy100% (1)

- Fuel Cells - Types and ChemistryDocument18 pagesFuel Cells - Types and ChemistryAditya KumarNo ratings yet

- Mother by Grace PaleyDocument9 pagesMother by Grace Paleylourdes.pereirorodriguezNo ratings yet

- ST 8100 ManualDocument66 pagesST 8100 ManualRadomír MachačNo ratings yet

- STP PracticeTest-3Document19 pagesSTP PracticeTest-3Ahmed tahaNo ratings yet

- Buku Gitar 1Document29 pagesBuku Gitar 1R Heru Suseno PusponegoroNo ratings yet

- 4BE0 01 Rms BengaliDocument13 pages4BE0 01 Rms BengaliJohn HopkinsNo ratings yet

- Rotational Molding DesignDocument110 pagesRotational Molding Designdamonlanglois100% (1)

- Rajba 2017Document4 pagesRajba 2017mohdsabithtNo ratings yet