You might also like

- AfarDocument128 pagesAfarlloyd77% (57)

- (Afar) Week1 Compiled QuestionsDocument78 pages(Afar) Week1 Compiled QuestionsBeef Testosterone84% (25)

- Chapter 1 Partnership Formation Test BanksDocument46 pagesChapter 1 Partnership Formation Test BanksRaisa Gelera91% (23)

- Chapter 12Document6 pagesChapter 12Marki Mendina100% (3)

- Reviewer in Partnership Corporation MycDocument22 pagesReviewer in Partnership Corporation MycScwythle65% (20)

- Partnership and Corp Liquid TestbankDocument288 pagesPartnership and Corp Liquid TestbankWendelyn Tutor83% (6)

- Partnership Liquidation. Alynna Joy P. IbanezDocument32 pagesPartnership Liquidation. Alynna Joy P. IbanezAllynna Joy83% (6)

- Partnership Formation111Document6 pagesPartnership Formation111Rhoiz75% (8)

- Corp Liq HandoutDocument14 pagesCorp Liq HandoutJesh Raz100% (12)

- Illustrations Partnership OperationsDocument23 pagesIllustrations Partnership OperationsMary Joy AlbandiaNo ratings yet

- Division of Profits and Losses Case #1: Sufficient Profit: Partnership OperationsDocument7 pagesDivision of Profits and Losses Case #1: Sufficient Profit: Partnership OperationsJuliana Cheng100% (3)

- 4 ACCT 2AB P. LiquidationDocument11 pages4 ACCT 2AB P. LiquidationMary Angeline Lopez100% (2)

- The Big Picture: Brief ExercisesDocument13 pagesThe Big Picture: Brief ExercisesRacel Agonia0% (1)

- CH 03Document4 pagesCH 03Rabie HarounNo ratings yet

- Practical Accounting 2: Angelito R. Punzalan, CPA, MBADocument33 pagesPractical Accounting 2: Angelito R. Punzalan, CPA, MBADaniella Mae Elip100% (1)

- Partnership: Formation of A PartnershipDocument70 pagesPartnership: Formation of A PartnershipWe W100% (1)

- Reminder: Use Your Official Answer Sheet: Universidad de ManilaDocument25 pagesReminder: Use Your Official Answer Sheet: Universidad de ManilaMarcellana ArianeNo ratings yet

- HahahahaDocument3 pagesHahahahaTyrelle Dela Cruz100% (1)

- Parcor CaseletsDocument13 pagesParcor CaseletsErika delos Santos100% (2)

- Partnership Liquidation: Debit CreditDocument7 pagesPartnership Liquidation: Debit CreditWenjun0% (1)

- Practical Accounting 2: Theory & Practice Advanced Accounting Partnership Liquidation & IncorporationDocument41 pagesPractical Accounting 2: Theory & Practice Advanced Accounting Partnership Liquidation & Incorporationsino akoNo ratings yet

- DocDocument1 pageDocaccounts 3 life100% (1)

- Chapter 1&2Document34 pagesChapter 1&2iptrcrmlNo ratings yet

- Afar ParcorDocument271 pagesAfar Parcorawesome bloggers0% (1)

- Quiz 3 Partnership DissolutionDocument6 pagesQuiz 3 Partnership DissolutionWenjun100% (1)

- ACCT4110 Advanced Accounting PRACTICE Exam 2 KEY v2Document14 pagesACCT4110 Advanced Accounting PRACTICE Exam 2 KEY v2accounts 3 lifeNo ratings yet

- Internal Reco Dec 2020Document12 pagesInternal Reco Dec 2020binuNo ratings yet

- ReiceivablesDocument27 pagesReiceivablesrivaceline100% (3)

- NSBZDocument6 pagesNSBZKenncy100% (4)

- Quiz in PartnershipDocument12 pagesQuiz in Partnershiplouise carino50% (2)

- Mid Term Exam Oct 2016 With SolDocument11 pagesMid Term Exam Oct 2016 With Solsunflower33% (3)

- OperationDocument6 pagesOperationKenncy50% (2)

- Accounting For Special Transactions Prelim Examination: Use The Following Information For The Next Two QuestionsDocument24 pagesAccounting For Special Transactions Prelim Examination: Use The Following Information For The Next Two QuestionsArtisan82% (11)

- Partnership DissolutionDocument17 pagesPartnership DissolutionMich Salvatorē0% (1)

- Quiz in Partnership Operations PDF FreeDocument1 pageQuiz in Partnership Operations PDF FreeKristine Esplana Toralde100% (1)

- Afar1-Exercises 2Document17 pagesAfar1-Exercises 2aleachon100% (1)

- Ast - 3B - Quiz No. 1Document10 pagesAst - 3B - Quiz No. 1Renalyn Paras0% (1)

- Finals Quiz Dissolution To LiquidationDocument6 pagesFinals Quiz Dissolution To LiquidationJeane Mae Boo75% (4)

- Partnership Dissolution: National College of Business and ArtsDocument5 pagesPartnership Dissolution: National College of Business and ArtsKate Jezel SantoniaNo ratings yet

- Blue and Rubi Are Partners Who Share Profits and Losses in The Ratio of 6Document7 pagesBlue and Rubi Are Partners Who Share Profits and Losses in The Ratio of 6Mark Edgar De Guzman100% (1)

- Prelim PartnershipDissolutionSampleProblemDocument12 pagesPrelim PartnershipDissolutionSampleProblemLee SuarezNo ratings yet

- Partnership 2Document45 pagesPartnership 2Леиа Аморес0% (1)

- LTCCDocument7 pagesLTCCGenesis Dizon67% (6)

- p1 Quiz With TheoryDocument15 pagesp1 Quiz With TheoryGrace CorpoNo ratings yet

- Reviewer 1 Fundamentals of Accounting 2 PDFDocument13 pagesReviewer 1 Fundamentals of Accounting 2 PDFelminvaldez80% (5)

- Accounting Special Transaction - PartnershipDocument12 pagesAccounting Special Transaction - PartnershipMikee LajatoNo ratings yet

- 8901 - Partnership FormationDocument3 pages8901 - Partnership FormationRica Jane Santos Marcelo100% (1)

- PUNZALANDocument16 pagesPUNZALANAngelique Kate Tanding DuguiangNo ratings yet

- Partnership - Key Notes and Sample ProblemsDocument6 pagesPartnership - Key Notes and Sample ProblemsCrestinaNo ratings yet

- Practical Accounting 2 - RMYCDocument10 pagesPractical Accounting 2 - RMYCZadharie Abby Gail BurataNo ratings yet

- 139Document9 pages139Allynna JoyNo ratings yet

- 1st Grading Exam - Key AnswersDocument28 pages1st Grading Exam - Key AnswersAmie Jane MirandaNo ratings yet

- Solutions Ang UbanDocument20 pagesSolutions Ang UbanPrincess Frean VillegasNo ratings yet

- ExmDocument18 pagesExmRoy Mitz Bautista0% (2)

- Long Quiz - Ast - MarcellanaDocument11 pagesLong Quiz - Ast - MarcellanaMarcellana ArianeNo ratings yet

- PacoaDocument18 pagesPacoaBianca VinluanNo ratings yet

- Accounting For Special Transactions First Grading ExaminationDocument22 pagesAccounting For Special Transactions First Grading ExaminationJasmine Sollestre100% (1)

- No Solutions, No PointsDocument5 pagesNo Solutions, No PointsLois Yanzeigh Habbiling BalachaweNo ratings yet

- AAA and BBB Are Partners With Capital of P60Document5 pagesAAA and BBB Are Partners With Capital of P60thats nottyNo ratings yet

- 1ST GRADING EXAM For StudentsDocument12 pages1ST GRADING EXAM For StudentsAndrea Florence Guy VidalNo ratings yet

- AFAR Finals With SolutionsDocument16 pagesAFAR Finals With SolutionsJr TanNo ratings yet

- Name: Date: Professor: Section: Score: Quiz No.3Document4 pagesName: Date: Professor: Section: Score: Quiz No.3Clint Agustin M. RoblesNo ratings yet

- Magic Dominique Julius Julius TotalDocument4 pagesMagic Dominique Julius Julius TotalPaupauNo ratings yet

- Quiz 1 ProblemsDocument6 pagesQuiz 1 ProblemsRuthchell CiriacoNo ratings yet

- SATURDAYDocument20 pagesSATURDAYkristine bandaviaNo ratings yet

- Practical Accounting 2 - ExaminationDocument10 pagesPractical Accounting 2 - ExaminationPrincess Claris ArauctoNo ratings yet

- The Responsibility For The Detection and Prevention of Errors, Fraud and Noncompliance With Laws and Regulations Rests With A. AuditorDocument2 pagesThe Responsibility For The Detection and Prevention of Errors, Fraud and Noncompliance With Laws and Regulations Rests With A. Auditoraccounts 3 lifeNo ratings yet

- Fraudu: 12. An Intentional Act by One or More Individuals AmongDocument2 pagesFraudu: 12. An Intentional Act by One or More Individuals Amongaccounts 3 lifeNo ratings yet

- Problem 1: Comprehensive Examination Applied Auditng Name: Score: Professor: DateDocument17 pagesProblem 1: Comprehensive Examination Applied Auditng Name: Score: Professor: Dateaccounts 3 life100% (1)

- B. Auditors Usually Rely On Lawyers' Representations To DetectDocument2 pagesB. Auditors Usually Rely On Lawyers' Representations To Detectaccounts 3 lifeNo ratings yet

- When Comparing The Auditor's Responsibility For DetectinDocument2 pagesWhen Comparing The Auditor's Responsibility For Detectinaccounts 3 lifeNo ratings yet

- D. Reasonable Assurance 34. Professional Skepticism Requires Auditors To Possess ADocument2 pagesD. Reasonable Assurance 34. Professional Skepticism Requires Auditors To Possess Aaccounts 3 lifeNo ratings yet

- BDocument2 pagesBaccounts 3 lifeNo ratings yet

- Which of The Following Is An Example of Fraudulent Financial Reporting?Document2 pagesWhich of The Following Is An Example of Fraudulent Financial Reporting?accounts 3 lifeNo ratings yet

- Strategy Vocabulary 1Document10 pagesStrategy Vocabulary 1accounts 3 lifeNo ratings yet

- Intro To S&T: Learning OutcomesDocument6 pagesIntro To S&T: Learning Outcomesaccounts 3 lifeNo ratings yet

- Of Employees in The Organization,: 23. If There Is Fraud Involving Top Management, The ProbabilityDocument2 pagesOf Employees in The Organization,: 23. If There Is Fraud Involving Top Management, The Probabilityaccounts 3 lifeNo ratings yet

- The Following Statements Relate To The Auditor's ResponsibilityDocument2 pagesThe Following Statements Relate To The Auditor's Responsibilityaccounts 3 lifeNo ratings yet

- Liven: 81. When Is The Auditor Responsible For Detecting Fraud?Document2 pagesLiven: 81. When Is The Auditor Responsible For Detecting Fraud?accounts 3 lifeNo ratings yet

- EAPP Lesson-4 SUMMARIZINGPARAPHRASING-TSDocument85 pagesEAPP Lesson-4 SUMMARIZINGPARAPHRASING-TSaccounts 3 lifeNo ratings yet

- Solution Chapter 4Document11 pagesSolution Chapter 4accounts 3 lifeNo ratings yet

- You Answered Correctly.: TREPD-0077Document55 pagesYou Answered Correctly.: TREPD-0077Bill SharmanNo ratings yet

- Salasar Sales 2023Document20 pagesSalasar Sales 2023tryabhi1234No ratings yet

- Translation Exposure Part 1Document31 pagesTranslation Exposure Part 1Magzoub MohaNo ratings yet

- Book of Accounts Practice SetDocument60 pagesBook of Accounts Practice SetMylene SalvadorNo ratings yet

- 1 - ExercisesDocument6 pages1 - ExercisesTrang Nguyễn QuỳnhNo ratings yet

- Final Account FormatDocument4 pagesFinal Account FormatHasdanNo ratings yet

- Topic 5 - Single-Entry MethodDocument49 pagesTopic 5 - Single-Entry MethodMary Yvonne AresNo ratings yet

- Lone Pine Cafe SolutionDocument5 pagesLone Pine Cafe SolutionRitu ChhipaNo ratings yet

- Activity 1.4.A Preparation of Financial ReportsDocument1 pageActivity 1.4.A Preparation of Financial ReportsheyheyNo ratings yet

- Literature ReviewDocument56 pagesLiterature ReviewVijaya LakshmiNo ratings yet

- Accounting Cycle - MALAYA KA NA COMPANYDocument7 pagesAccounting Cycle - MALAYA KA NA COMPANYkrisllyuyuyNo ratings yet

- EV 2 - KVS Agra XI Acc QP & MS (Annual Exam) 19-20Document13 pagesEV 2 - KVS Agra XI Acc QP & MS (Annual Exam) 19-20minita sharmaNo ratings yet

- Long-Term Financial Planning and GrowthDocument37 pagesLong-Term Financial Planning and GrowthNauryzbek MukhanovNo ratings yet

- Practice Exam 4 - Chapters 8, 9, - Fall 2012Document6 pagesPractice Exam 4 - Chapters 8, 9, - Fall 2012Vincent ChinNo ratings yet

- Group Reporting II: Application of The Acquisition Method Under IFRS 3Document77 pagesGroup Reporting II: Application of The Acquisition Method Under IFRS 3فهد التويجريNo ratings yet

- Introduction To Financial AccountingDocument64 pagesIntroduction To Financial AccountingGurkirat Singh100% (1)

- Jawaban Silus Adijaya 2015Document15 pagesJawaban Silus Adijaya 2015natsu dragnelNo ratings yet

- Ch16 Financial Statement AnalysisDocument134 pagesCh16 Financial Statement AnalysisLeigh Garanchon100% (3)

- CH 05Document77 pagesCH 05Phan Quynh Ha100% (1)

- Book 1Document2 pagesBook 1Laika DuradaNo ratings yet

- Hamza ZarishDocument31 pagesHamza ZarishTehreem FatimaNo ratings yet

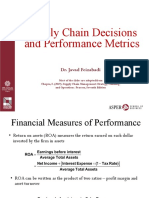

- 3-Supply Chain Decisions and Performance Metrics (A)Document21 pages3-Supply Chain Decisions and Performance Metrics (A)eeman kNo ratings yet

- (Module 10 - Module 18) MGT 101 FinalDocument453 pages(Module 10 - Module 18) MGT 101 FinalUsama KJ100% (1)

- Homework On Single Entry PDFDocument2 pagesHomework On Single Entry PDFalyssaNo ratings yet

- Chapter 10 Exercises Acc101Document6 pagesChapter 10 Exercises Acc101Nguyen Thi Van Anh (K17 HL)No ratings yet