You might also like

- An Indonesian Citizen As A Foreign Tax ResidentDocument1 pageAn Indonesian Citizen As A Foreign Tax ResidentmelsyNo ratings yet

- Assignment Answer of Questions Raihan Shidqi Raditiya 1910533024Document3 pagesAssignment Answer of Questions Raihan Shidqi Raditiya 1910533024Raihan RaditiyaNo ratings yet

- TaxpayersDocument26 pagesTaxpayersJessa Mae IgotNo ratings yet

- BUT-WPS OfficeDocument6 pagesBUT-WPS OfficeVentito StyleNo ratings yet

- Indonesia Individual Income Tax Guide 1Document24 pagesIndonesia Individual Income Tax Guide 1Abu AfkariNo ratings yet

- Document .36Document15 pagesDocument .36jyotisingh6908501No ratings yet

- Tax ExamDocument29 pagesTax ExamAnn Olivia VallavanadanNo ratings yet

- Faq ITDocument9 pagesFaq ITManu GuptaNo ratings yet

- Income TaxDocument20 pagesIncome TaxuzmaNo ratings yet

- 3 Income Tax ConceptsDocument37 pages3 Income Tax ConceptsRommel Espinocilla Jr.No ratings yet

- Income Tax 2Document10 pagesIncome Tax 2Blaise VENo ratings yet

- Income TaxDocument6 pagesIncome TaxDISHANNo ratings yet

- Lesson 4.2 - TAXATION INCOMEDocument4 pagesLesson 4.2 - TAXATION INCOMEIshi MaxineNo ratings yet

- Taxation Topic 3Document29 pagesTaxation Topic 3Philip Gwadenya100% (2)

- Lecture-3 Income Classsification and Residential StatusDocument25 pagesLecture-3 Income Classsification and Residential Statusimdadul haqueNo ratings yet

- Income Taxation NotesDocument14 pagesIncome Taxation Notescristiepearl100% (2)

- Bahasa Inggris PPHDocument9 pagesBahasa Inggris PPHRiska UsmawardaniNo ratings yet

- Income Tax FaqDocument11 pagesIncome Tax FaqNasir AhmedNo ratings yet

- Unit 1-DefinitionDocument15 pagesUnit 1-Definitionsinghnegilaxman500No ratings yet

- Corporate Income TaxDocument24 pagesCorporate Income TaxRIRI RUMAIZHANo ratings yet

- Income TaxationDocument138 pagesIncome TaxationLimberge Paul CorpuzNo ratings yet

- Module - 1 Basic Concepts.Document11 pagesModule - 1 Basic Concepts.Dimple JainNo ratings yet

- UNIT-1 Basic Concepts of Income TaxDocument38 pagesUNIT-1 Basic Concepts of Income TaxGarimaNo ratings yet

- Report in Taxation Group 3Document25 pagesReport in Taxation Group 3Patricia BacatanoNo ratings yet

- Tax Income in GeneralDocument38 pagesTax Income in GeneralRIRI RUMAIZHANo ratings yet

- Unit 1 ItlaDocument11 pagesUnit 1 ItlaAbdul basitNo ratings yet

- Introduction To Income TaxationDocument3 pagesIntroduction To Income TaxationescrowNo ratings yet

- Share Taxpayer and Elements of Gross IncomeDocument24 pagesShare Taxpayer and Elements of Gross IncomeJessa Mae IgotNo ratings yet

- EC1B1 - Intro TaxationDocument38 pagesEC1B1 - Intro TaxationZen Marcus RodasNo ratings yet

- Income Tax Matatag NotesDocument21 pagesIncome Tax Matatag NotesRicel CriziaNo ratings yet

- Basic Concept of Income TaxDocument4 pagesBasic Concept of Income TaxNaurah Atika DinaNo ratings yet

- Income TaxDocument51 pagesIncome TaxInternet 223No ratings yet

- Situs of Taxation Literally Means Place of TaxationDocument19 pagesSitus of Taxation Literally Means Place of TaxationRowie Ann Arista SiribanNo ratings yet

- Tax Planning and ManagementDocument16 pagesTax Planning and ManagementDeepika GuptaNo ratings yet

- Income TaxationDocument32 pagesIncome Taxationblackphoenix303No ratings yet

- NOTES Income TaxDocument6 pagesNOTES Income Taxcanetadexter87No ratings yet

- Taxation System in IndiaDocument30 pagesTaxation System in IndiaSwapnil Pisal-DeshmukhNo ratings yet

- SeemaDocument61 pagesSeemaAkash ShewadeNo ratings yet

- Subject and Object of TaxationDocument12 pagesSubject and Object of TaxationCahyani PrastutiNo ratings yet

- Semester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaDocument14 pagesSemester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaHarsh KamaliyaNo ratings yet

- Lecture Outline: Taxation of IncomeDocument65 pagesLecture Outline: Taxation of IncomeNickson AkolaNo ratings yet

- LLB Tax NavDocument31 pagesLLB Tax Navamit HCSNo ratings yet

- Basic ConceptsDocument35 pagesBasic Concepts3208 A PallaviNo ratings yet

- With Its Rich Cultural Landscape and International PopulationDocument6 pagesWith Its Rich Cultural Landscape and International PopulationYongkiNo ratings yet

- Tax Reviewer by MoiDocument4 pagesTax Reviewer by MoiKenny BesarioNo ratings yet

- Taxation 2 NIRCDocument84 pagesTaxation 2 NIRCEric GarciaNo ratings yet

- Module 4 - Lesson 18 - FinalDocument8 pagesModule 4 - Lesson 18 - FinalMai RuizNo ratings yet

- Lesson Income TaxDocument8 pagesLesson Income TaxEfren Lester ReyesNo ratings yet

- BasicDocument18 pagesBasicHello BrotherNo ratings yet

- Interview 3. Direct TaxDocument14 pagesInterview 3. Direct TaxNiladri SahaNo ratings yet

- Unit 3 - Concepts of Income & Income TaxationDocument10 pagesUnit 3 - Concepts of Income & Income TaxationJoseph Anthony RomeroNo ratings yet

- Module No 2 - INCOME TAXATION PART1ADocument11 pagesModule No 2 - INCOME TAXATION PART1APrinces S. RoqueNo ratings yet

- I. Basic Concepts in Income TaxationDocument79 pagesI. Basic Concepts in Income Taxationcmv mendoza100% (1)

- Income Tax ActDocument9 pagesIncome Tax Actbishtrohan064No ratings yet

- Income Tax FinalDocument20 pagesIncome Tax FinalSiddarood KumbarNo ratings yet

- Lesson 5 Inclusions Exclusions From Gi Final TaxDocument17 pagesLesson 5 Inclusions Exclusions From Gi Final TaxOrduna Mae AnnNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Indonesian Taxation: for Academics and Foreign Business Practitioners Doing Business in IndonesiaFrom EverandIndonesian Taxation: for Academics and Foreign Business Practitioners Doing Business in IndonesiaNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

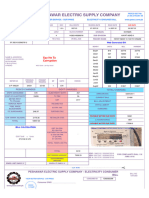

- Pesco Online BillDocument2 pagesPesco Online Billshahjahan_173960965No ratings yet

- Incotax Quiz 2Document6 pagesIncotax Quiz 2Stephanie LeeNo ratings yet

- Payroll ProjectDocument16 pagesPayroll ProjectKatrina Rardon-Swoboda68% (25)

- ABS-CBN Vs CTADocument3 pagesABS-CBN Vs CTAShiela PilarNo ratings yet

- Full Download Ebook Ebook PDF Mcgraw Hills Essentials of Federal Taxation 2020 Edition 11th Edition PDFDocument41 pagesFull Download Ebook Ebook PDF Mcgraw Hills Essentials of Federal Taxation 2020 Edition 11th Edition PDFyolanda.richards657100% (39)

- Tax Quiz 3 Q Tax 1Document4 pagesTax Quiz 3 Q Tax 1bimbyboNo ratings yet

- ACW2491 - 2018 S1 - WK 2 Lecture ExampleDocument2 pagesACW2491 - 2018 S1 - WK 2 Lecture Examplehi2joeyNo ratings yet

- Guarding Against Pandemics 2022 Tax FilingDocument30 pagesGuarding Against Pandemics 2022 Tax FilingTeddy SchleiferNo ratings yet

- BIR Ruling 383-15 - Dividends Received by Luxembourg Entity (Participation Exemption)Document5 pagesBIR Ruling 383-15 - Dividends Received by Luxembourg Entity (Participation Exemption)Jerwin DaveNo ratings yet

- Signed By:Bulusu Samba Murthy Reason:Security Reason Location:Mumbai Signing Date:16.07.2020 18:41Document8 pagesSigned By:Bulusu Samba Murthy Reason:Security Reason Location:Mumbai Signing Date:16.07.2020 18:41Aviral SankhyadharNo ratings yet

- Tax InvoiceDocument2 pagesTax Invoicearihantjha36No ratings yet

- II A - Income Tax QuestionsDocument1 pageII A - Income Tax QuestionsRohith krishnan ktNo ratings yet

- Downloadfile 2Document17 pagesDownloadfile 2Jung Hwan SoNo ratings yet

- TGT403Document7 pagesTGT403vikasNo ratings yet

- SSS TableDocument1 pageSSS Tablegmangalo95% (22)

- Icfai Business School Pune GSTDocument6 pagesIcfai Business School Pune GSTHIMANSHU PATHAKNo ratings yet

- 2551Q Jan 2018 ENCS Final Rev 3Document2 pages2551Q Jan 2018 ENCS Final Rev 3MIS MijerssNo ratings yet

- E39042b6 PDFDocument199 pagesE39042b6 PDFGilbert PariyoNo ratings yet

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 pageBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountAmanNo ratings yet

- 4 2021 UST Golden Notes Taxation LawDocument465 pages4 2021 UST Golden Notes Taxation LawRomme Andrae Velasco100% (4)

- Bedding F-702 NEWDocument2 pagesBedding F-702 NEWBADIGA SHIVA GOUDNo ratings yet

- GST MCQs Chapter 3 Reverse Charge by Vishal BhattadDocument5 pagesGST MCQs Chapter 3 Reverse Charge by Vishal Bhattadadiacharya0021No ratings yet

- PMK 242-03-2014 (English)Document49 pagesPMK 242-03-2014 (English)Irka PlayingNo ratings yet

- Income Tax: Full PFRS, Prfs For Smes & Pfrs For SesDocument15 pagesIncome Tax: Full PFRS, Prfs For Smes & Pfrs For SesChara etangNo ratings yet

- Hrishad - Income TaxDocument9 pagesHrishad - Income Taxkhayyum0% (1)

- Cellsons Appeal StatementDocument45 pagesCellsons Appeal Statementjenniferthanu1521No ratings yet

- Income Tax Law & PracticeDocument29 pagesIncome Tax Law & PracticeMohanNo ratings yet

- Realmebuds q2Document1 pageRealmebuds q2vimal vajpeyiNo ratings yet

- Payment Receipt 0005743148Document1 pagePayment Receipt 0005743148Chitradeep FalguniyaNo ratings yet

- Module 5 Unit 2 Taxable Capital Gains-2Document7 pagesModule 5 Unit 2 Taxable Capital Gains-2Jade EdajNo ratings yet