You might also like

- Dealing With The Tax Issues: Discount and Premium BondsDocument4 pagesDealing With The Tax Issues: Discount and Premium BondsAntonio J FernósNo ratings yet

- Trends Networks Module 3Document35 pagesTrends Networks Module 3Joseph Mondo�edo91% (34)

- Transfer Pricing Documentation File TemplateDocument4 pagesTransfer Pricing Documentation File TemplateMuris Supic33% (3)

- Stock Market - A Complete Guide BookDocument43 pagesStock Market - A Complete Guide BookParag Saxena100% (1)

- 9th Chapter 3 - Planning and Implementing Customer Relationship Management ProjectsDocument32 pages9th Chapter 3 - Planning and Implementing Customer Relationship Management ProjectsHarpreetNo ratings yet

- Assignments: Program: MFC Semester-IvDocument16 pagesAssignments: Program: MFC Semester-IvkeenodiidNo ratings yet

- Chapter Three Interest Rates in The Financial SystemDocument41 pagesChapter Three Interest Rates in The Financial SystemHamza AbduremanNo ratings yet

- Tutorial 10 - CH18-1Document4 pagesTutorial 10 - CH18-1zachNo ratings yet

- FIN2601-chapter 6Document28 pagesFIN2601-chapter 6Atiqa Aslam100% (1)

- Predatory Pricing and Its Aspects - Competition LawDocument18 pagesPredatory Pricing and Its Aspects - Competition LawKanishkMauryaNo ratings yet

- Chapter-6 GITMAN SOLMANDocument24 pagesChapter-6 GITMAN SOLMANJudy Ann Margate Victoria67% (6)

- Fabozzi Fofmi4 Ch11 ImDocument12 pagesFabozzi Fofmi4 Ch11 ImYasir ArafatNo ratings yet

- Cfi1203 Module 2 Interest Rates Determination & StructureDocument8 pagesCfi1203 Module 2 Interest Rates Determination & StructureLeonorahNo ratings yet

- John J Murphy - Technical Analysis of The Financial MarketsDocument547 pagesJohn J Murphy - Technical Analysis of The Financial MarketsJaime González100% (1)

- Reverse FactoringDocument83 pagesReverse Factoringcamy0529100% (1)

- Resource Based Theory Creating and Sustaining Competitive Advantage PDFDocument327 pagesResource Based Theory Creating and Sustaining Competitive Advantage PDFRofi Sang MaesTro0% (1)

- Dhillon Garcia Fronti Zhang Sovereign Debt The Impact of Creditor's CompositionDocument36 pagesDhillon Garcia Fronti Zhang Sovereign Debt The Impact of Creditor's CompositionecrcauNo ratings yet

- A Preferred-Habitat Model of The Term Structure of Interest Rates-Nov09Document59 pagesA Preferred-Habitat Model of The Term Structure of Interest Rates-Nov09kevNo ratings yet

- Pension DurationDocument48 pagesPension DurationZerohedge100% (1)

- Modeling Term Structures of Swap SpreadsDocument50 pagesModeling Term Structures of Swap SpreadsAshwin R JohnNo ratings yet

- Chapter 3 FIMDocument7 pagesChapter 3 FIMMintayto TebekaNo ratings yet

- Term Premia: Models and Some Stylised FactsDocument13 pagesTerm Premia: Models and Some Stylised FactssdafwetNo ratings yet

- Sovereign Debt Auctions With Strategic InteractionsDocument84 pagesSovereign Debt Auctions With Strategic InteractionsGabriel DAnnunzioNo ratings yet

- amihud1991Document16 pagesamihud1991Phoenix WhiteNo ratings yet

- PFM15e IM CH06Document24 pagesPFM15e IM CH06Daniel HakimNo ratings yet

- The Declining U.S. Equity PremiumDocument19 pagesThe Declining U.S. Equity PremiumpostscriptNo ratings yet

- Credit Default Swaps and Equity Prices: The Itraxx Cds Index MarketDocument14 pagesCredit Default Swaps and Equity Prices: The Itraxx Cds Index MarketLiam MescallNo ratings yet

- Price Efficiency and Short Selling HighlightedDocument32 pagesPrice Efficiency and Short Selling HighlightedSUNLINo ratings yet

- How Risk and Term Structure Affect Interest RatesDocument8 pagesHow Risk and Term Structure Affect Interest RatesAisha Bint TilaNo ratings yet

- Interest Rate Swaps M An Agency Theqretic Model M Pnterest RatesDocument10 pagesInterest Rate Swaps M An Agency Theqretic Model M Pnterest RateserererehgjdsassdfNo ratings yet

- SSRN Id686681Document47 pagesSSRN Id686681Qurrotu AiniNo ratings yet

- Benefits and Limitations of Inflation Indexed Treasury BondsDocument16 pagesBenefits and Limitations of Inflation Indexed Treasury BondsBindia AhujaNo ratings yet

- Blanco - Brennan - Marsh Journal of Finance 2005Document28 pagesBlanco - Brennan - Marsh Journal of Finance 2005Nur KhamisahNo ratings yet

- Tutorial Questions Unit 2-AnsDocument9 pagesTutorial Questions Unit 2-AnsPrincessCC20No ratings yet

- Chapter 6 Solution Manual For Principles of Managerial Finance 13th Edition Lawrence PDFDocument24 pagesChapter 6 Solution Manual For Principles of Managerial Finance 13th Edition Lawrence PDFNazar FaridNo ratings yet

- Thesis Interest Rate Risk ManagementDocument6 pagesThesis Interest Rate Risk Managementvaleriemejiabakersfield100% (2)

- Bond Indenture Provisions and The Risk of Corporate Debt 1982 Journal of Financial EconomicsDocument32 pagesBond Indenture Provisions and The Risk of Corporate Debt 1982 Journal of Financial EconomicsZhang PeilinNo ratings yet

- The Role of Operating Contracts in Influencing Loan Spreads and Leverage in Project Finance DealsDocument43 pagesThe Role of Operating Contracts in Influencing Loan Spreads and Leverage in Project Finance DealsCUTto1122No ratings yet

- Chapter 4 SolutionsDocument12 pagesChapter 4 SolutionsEdmond ZNo ratings yet

- 03 Handout 1Document13 pages03 Handout 1Adrasteia ZachryNo ratings yet

- Chapter 6Document23 pagesChapter 6red8blue8No ratings yet

- Financial Institutin ManagementDocument7 pagesFinancial Institutin ManagementAbu SufianNo ratings yet

- An Arbitrage-Free Three-Factor Term Structure Model and The Recent Behavior of Long-Term Yields and Distant-Horizon Forward RatesDocument27 pagesAn Arbitrage-Free Three-Factor Term Structure Model and The Recent Behavior of Long-Term Yields and Distant-Horizon Forward RatessjanaszakNo ratings yet

- The Liquidity Premium For Illiquid AnnuitiesDocument25 pagesThe Liquidity Premium For Illiquid Annuitieseric__boxNo ratings yet

- Informal Sector and Economic Growth: The Supply of Credit ChannelDocument24 pagesInformal Sector and Economic Growth: The Supply of Credit ChannelPride Tutorials Manikbagh RoadNo ratings yet

- Discussing Theories of the Term Structure of Interest RatesDocument12 pagesDiscussing Theories of the Term Structure of Interest RatesEdwin Lwandle NcubeNo ratings yet

- UnderstandingReturnsToShortSellingU PreviewDocument52 pagesUnderstandingReturnsToShortSellingU PreviewDjtux75No ratings yet

- Levich Ch11 Net Assignment SolutionsDocument16 pagesLevich Ch11 Net Assignment SolutionsNisarg JoshiNo ratings yet

- Chapter Three Interest Rates in The Financial SystemDocument40 pagesChapter Three Interest Rates in The Financial SystemKalkayeNo ratings yet

- BFC5935 - Tutorial 7 SolutionsDocument4 pagesBFC5935 - Tutorial 7 SolutionsXue XuNo ratings yet

- Econometric Analysis of Life Insurance Policy Loan DemandDocument14 pagesEconometric Analysis of Life Insurance Policy Loan DemandFurkan TuraNo ratings yet

- Leasing Decisions Impact Bank DebtDocument29 pagesLeasing Decisions Impact Bank DebtmirelushiNo ratings yet

- Types of Derivatives: Forwards: FuturesDocument5 pagesTypes of Derivatives: Forwards: FuturesVinayak DalbhanjanNo ratings yet

- Debt and Incomplete Financial Markets: A Case For Nominal GDP TargetingDocument52 pagesDebt and Incomplete Financial Markets: A Case For Nominal GDP Targetingmirando93No ratings yet

- A Note On Term Structure and Inflationary Expectations in Kenya - by Francis MwegaDocument14 pagesA Note On Term Structure and Inflationary Expectations in Kenya - by Francis Mwegamburu. hNo ratings yet

- SLloyd CERFDocument60 pagesSLloyd CERFKamel RamtanNo ratings yet

- Answers To Chapter 6 QuestionsDocument9 pagesAnswers To Chapter 6 QuestionsMoNo ratings yet

- Interest Rates Determinants and TheoriesDocument11 pagesInterest Rates Determinants and TheoriesEugene AlipioNo ratings yet

- Derivative (Finance)Document18 pagesDerivative (Finance)Martin FeNo ratings yet

- Working Paper No. 343: Efficient Frameworks For Sovereign BorrowingDocument33 pagesWorking Paper No. 343: Efficient Frameworks For Sovereign BorrowingChristo FilevNo ratings yet

- 02 Financial Markets 2 140-17-29Document13 pages02 Financial Markets 2 140-17-29Armando CarreñoNo ratings yet

- Collateral and Credit Issues in Derivatives PricingDocument36 pagesCollateral and Credit Issues in Derivatives PricingAakash KhandelwalNo ratings yet

- Chapter 3 - Structure of Interest RatesDocument34 pagesChapter 3 - Structure of Interest RatesSajjad HussainNo ratings yet

- Dissertation Report On Working Capital ManagementDocument33 pagesDissertation Report On Working Capital ManagementAnirudh SinghaNo ratings yet

- Chapter Three Interest Rates in The Financial SystemDocument34 pagesChapter Three Interest Rates in The Financial SystemNatnael Asfaw0% (1)

- FRBSF E L: Conomic EtterDocument4 pagesFRBSF E L: Conomic Ettertariq74739No ratings yet

- Interest Rate Risk: Prof Mahesh Kumar Amity Business SchoolDocument110 pagesInterest Rate Risk: Prof Mahesh Kumar Amity Business SchoolasifanisNo ratings yet

- Roles and Responsibilities: The Financing Team in An Initial Municipal Bond OfferingDocument4 pagesRoles and Responsibilities: The Financing Team in An Initial Municipal Bond OfferingAntonio J FernósNo ratings yet

- A Federal Strategic Action Plan On Immigrant & Refugee Integration - April2015 - TheWhiteHouseDocument70 pagesA Federal Strategic Action Plan On Immigrant & Refugee Integration - April2015 - TheWhiteHouseAntonio J FernósNo ratings yet

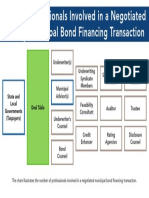

- Professionals Involved in A Negotiated Municipal Bond Financing TransactionDocument1 pageProfessionals Involved in A Negotiated Municipal Bond Financing TransactionAntonio J FernósNo ratings yet

- S&P Perspectives On The State of The Municipal Market: Where We Have Been and Where We Are HeadingDocument52 pagesS&P Perspectives On The State of The Municipal Market: Where We Have Been and Where We Are HeadingAntonio J FernósNo ratings yet

- Fama&MacBeth PresentationDocument16 pagesFama&MacBeth PresentationAntonio J FernósNo ratings yet

- S&P Perspectives On The State of The Municipal Market: Where We Have Been and Where We Are HeadingDocument52 pagesS&P Perspectives On The State of The Municipal Market: Where We Have Been and Where We Are HeadingAntonio J FernósNo ratings yet

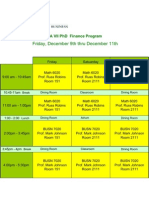

- LA VII PhD Finance Program Schedule Dec 9-11Document1 pageLA VII PhD Finance Program Schedule Dec 9-11Antonio J FernósNo ratings yet

- The Volcker Rule As Proposed QuestionsDocument51 pagesThe Volcker Rule As Proposed QuestionsAntonio J FernósNo ratings yet

- Bidvest BankDocument2 pagesBidvest BankDurban Chamber of Commerce and Industry0% (1)

- Gmail - DropshippingDocument2 pagesGmail - DropshippingEli MentoNo ratings yet

- Charter 5-General Supplier ConsolidationDocument3 pagesCharter 5-General Supplier ConsolidationgenfinNo ratings yet

- Function of MoneyDocument2 pagesFunction of MoneyAlexandraNo ratings yet

- BED2206 VIRTUAL CATS INTERMEDIATE MICRO ECONOMICS AnnieDocument5 pagesBED2206 VIRTUAL CATS INTERMEDIATE MICRO ECONOMICS AnniecyrusNo ratings yet

- Ibo-6 Unit-1 International Monetary Systems and InstitutionsDocument7 pagesIbo-6 Unit-1 International Monetary Systems and InstitutionsGaytri KochharNo ratings yet

- Online Test Series and Capsule for JAIIB ExamDocument169 pagesOnline Test Series and Capsule for JAIIB ExamSinha KanhaiyajiNo ratings yet

- Payment Banks & Mobile/Digital Wallets in South Africa: Submitted By-Group 4Document21 pagesPayment Banks & Mobile/Digital Wallets in South Africa: Submitted By-Group 4piyushghsaNo ratings yet

- Industrial Environment: Chapter OutlineDocument13 pagesIndustrial Environment: Chapter OutlineRevti sainNo ratings yet

- TECHNOLOGY TRANSFER METHODS-by Denis 2013 PDFDocument5 pagesTECHNOLOGY TRANSFER METHODS-by Denis 2013 PDFHana AfifahNo ratings yet

- Srac MHRMDocument1 pageSrac MHRMPraWin KharateNo ratings yet

- 07MB105 Financial & Management Accounting - OKDocument21 pages07MB105 Financial & Management Accounting - OKKumaran Thayumanavan0% (1)

- CUSAT MBA Admission Test Sample QuestionsDocument5 pagesCUSAT MBA Admission Test Sample QuestionsCMA RajaNo ratings yet

- Charles P. Jones, Investments: Analysis and Management, 12 Edition, John Wiley & SonsDocument23 pagesCharles P. Jones, Investments: Analysis and Management, 12 Edition, John Wiley & SonsJc TambauanNo ratings yet

- 2.1 Recap - Money Markets PDFDocument26 pages2.1 Recap - Money Markets PDFRedNo ratings yet

- Dividend Policy and Stock Price Volatility in GhanaDocument1 pageDividend Policy and Stock Price Volatility in GhanaFahad MunirNo ratings yet

- Positioning and its importance for service companiesDocument3 pagesPositioning and its importance for service companieswardakhanNo ratings yet

- Derivatives Market FinalDocument19 pagesDerivatives Market FinalRohit ChellaniNo ratings yet

- Importance of Reverse Logistics & Recovery OptionsDocument23 pagesImportance of Reverse Logistics & Recovery OptionsJoanna Tee Kai YinNo ratings yet

- Compliance of Buy Back of SharesDocument18 pagesCompliance of Buy Back of Sharesswaraj_chaw1485No ratings yet

- Chapter 3Document2 pagesChapter 3Ashwini PudasainiNo ratings yet

- Contingency Theory Some Suggested Directions PDFDocument20 pagesContingency Theory Some Suggested Directions PDFNirolama 11 2ndNo ratings yet

- Swot AnalysisDocument2 pagesSwot Analysisapi-360980791No ratings yet