You might also like

- Technical Drawing Business PlanDocument7 pagesTechnical Drawing Business PlanVinood SeepersaudNo ratings yet

- Mid Term Assignment 1 On FAR - Journalizing, Posting, and Unadjusted Trial BalanceDocument1 pageMid Term Assignment 1 On FAR - Journalizing, Posting, and Unadjusted Trial BalanceAnne AlagNo ratings yet

- A Short Review On Basic FinanceDocument4 pagesA Short Review On Basic FinanceJed AoananNo ratings yet

- History of TQMDocument23 pagesHistory of TQMVarsha PandeyNo ratings yet

- FM1 ActivityDocument4 pagesFM1 ActivityChieMae Benson Quinto100% (1)

- Co-Operative Housing SocietyDocument29 pagesCo-Operative Housing SocietyVish Patilvs67% (3)

- Securitization For DummiesDocument5 pagesSecuritization For DummiesHarpott GhantaNo ratings yet

- Official Form 309A (For Individuals or Joint Debtors) : Order and Notice of Chapter 7 Bankruptcy Case 01/19Document3 pagesOfficial Form 309A (For Individuals or Joint Debtors) : Order and Notice of Chapter 7 Bankruptcy Case 01/19Anonymous Te6DQINo ratings yet

- Activity 1 (Module 1)Document1 pageActivity 1 (Module 1)Jherrie Mae MattaNo ratings yet

- M LhuillierDocument28 pagesM LhuillierAyidar Luratsi Nassah100% (1)

- Sales 140, 800 Less: Cost of Sales (84, 480) Gross ProfitDocument5 pagesSales 140, 800 Less: Cost of Sales (84, 480) Gross ProfitMichaela KowalskiNo ratings yet

- Humborg Activity 4Document1 pageHumborg Activity 4Frances CarpioNo ratings yet

- Good Gorvernanc-WPS OfficeDocument11 pagesGood Gorvernanc-WPS Officeclarisse villegas100% (2)

- Basic Accounting EquationDocument4 pagesBasic Accounting EquationMuhammad AhmadNo ratings yet

- Eoq PDFDocument23 pagesEoq PDFMica Ella Gutierrez0% (1)

- Basic FinanceDocument3 pagesBasic Financezandro_ico5041No ratings yet

- Evaluating Firm Performance - ReportDocument5 pagesEvaluating Firm Performance - ReportJeane Mae BooNo ratings yet

- Time Value of MoneyDocument58 pagesTime Value of MoneyJennifer Rasonabe100% (1)

- Computing Mean Historical ReturnsDocument2 pagesComputing Mean Historical Returnsmubarek oumerNo ratings yet

- Writing Up A Case StudyDocument3 pagesWriting Up A Case StudyalliahnahNo ratings yet

- Developing An Effective Ethics ProgramDocument22 pagesDeveloping An Effective Ethics ProgramKarthikSingaporeNo ratings yet

- Financial Management 2: Prepared By: Eunice Meanne B. SiapnoDocument33 pagesFinancial Management 2: Prepared By: Eunice Meanne B. SiapnoRyan TamondsNo ratings yet

- Perceiving Ourselves and Others in OrganizationDocument54 pagesPerceiving Ourselves and Others in OrganizationYana RamliNo ratings yet

- Working Capital Management - Introduction - Session 1 & 2Document56 pagesWorking Capital Management - Introduction - Session 1 & 2Vaidyanathan RavichandranNo ratings yet

- Chapter 4 To 6 (Merge)Document35 pagesChapter 4 To 6 (Merge)KENNETH IAN MADERANo ratings yet

- Q: Compare The Following Goals and Explain Why Wealth Maximization Is Chosen by The Firms?Document1 pageQ: Compare The Following Goals and Explain Why Wealth Maximization Is Chosen by The Firms?Mahvesh ZahraNo ratings yet

- NIKE Company's CSR StrategyDocument24 pagesNIKE Company's CSR StrategyMzito Jnr MzitoNo ratings yet

- Corporate Governance ResponsibilitiesDocument18 pagesCorporate Governance ResponsibilitiesAlvin VidalNo ratings yet

- Lesson 1 Prepared By: Asst. Prof. Sherylyn T. Trinidad: The Management ScienceDocument17 pagesLesson 1 Prepared By: Asst. Prof. Sherylyn T. Trinidad: The Management ScienceErine ContranoNo ratings yet

- Chapter 1 A Strategic Management Model HRDDocument10 pagesChapter 1 A Strategic Management Model HRDJanrhey EnriquezNo ratings yet

- Wright Technological College of Antique Senior High School Sibalom Branch Sibalom, AntiqueDocument6 pagesWright Technological College of Antique Senior High School Sibalom Branch Sibalom, AntiqueLen PenieroNo ratings yet

- Accounting ReviewerDocument21 pagesAccounting ReviewerAdriya Ley PangilinanNo ratings yet

- I. Learning Activities: Sum of Weights (3+2+1) 6Document6 pagesI. Learning Activities: Sum of Weights (3+2+1) 6Valdez AlyssaNo ratings yet

- CH 9 - Completing The Cycle - MerchandisingDocument38 pagesCH 9 - Completing The Cycle - MerchandisingJem Bobiles100% (1)

- Holy Cross of Davao College: Other Campuses: Camudmud (IGACOS), Bajada (SOS Drive)Document3 pagesHoly Cross of Davao College: Other Campuses: Camudmud (IGACOS), Bajada (SOS Drive)Haries Vi Traboc Micolob100% (1)

- Orge University. AnjieDocument4 pagesOrge University. AnjieKim Kyun SiNo ratings yet

- Monitoring of Credit and Collection FundsDocument24 pagesMonitoring of Credit and Collection FundsADALIA BEATRIZ ONGNo ratings yet

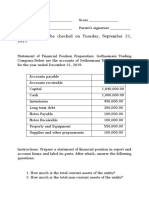

- Answer This To Be Checked On Tuesday, September 21, 2021Document2 pagesAnswer This To Be Checked On Tuesday, September 21, 2021Teresa Mae OrquiaNo ratings yet

- MBA 103 Chapter 12Document27 pagesMBA 103 Chapter 12Art Virgel DensingNo ratings yet

- Chapter 5 - Globalization & SocietyDocument18 pagesChapter 5 - Globalization & SocietyAnonymous cwC8kTyNo ratings yet

- Lesson 1 Introduction PDFDocument5 pagesLesson 1 Introduction PDFAngelita Dela cruzNo ratings yet

- Social Responsibility & Ethical Issues in International BusinessDocument16 pagesSocial Responsibility & Ethical Issues in International BusinessRavindra GoyalNo ratings yet

- Assignment 4: International Business EnvironmentDocument1 pageAssignment 4: International Business EnvironmentSheen CatayongNo ratings yet

- Chapter 1Document7 pagesChapter 1Lhea Tomas Bicera-AlcantaraNo ratings yet

- Lesson 1 The Nature and Forms of Business OrganizationsDocument1 pageLesson 1 The Nature and Forms of Business OrganizationsYanko Yap BondocNo ratings yet

- Chapter 2Document5 pagesChapter 2Sundaramani SaranNo ratings yet

- Buisness CycleDocument8 pagesBuisness CycleyagyatiwariNo ratings yet

- Janelle. CHANGE ORIENTATION OF ORGANIZATIONAL DEVELOPMENT.Document4 pagesJanelle. CHANGE ORIENTATION OF ORGANIZATIONAL DEVELOPMENT.Jelyne PachecoNo ratings yet

- Planning Spoken and Written MessagesDocument42 pagesPlanning Spoken and Written MessagesJessa Mae GuzmanNo ratings yet

- Ch01 McGuiganDocument31 pagesCh01 McGuiganJonathan WatersNo ratings yet

- Bank ReserveDocument11 pagesBank ReserveNicole Ocampo100% (1)

- Partnership and Corporation Part 1Document60 pagesPartnership and Corporation Part 1Jeraldine DejanNo ratings yet

- Foa p1 Module 2 For Bsa & Bsais StudentsDocument64 pagesFoa p1 Module 2 For Bsa & Bsais StudentsMiquel VillamarinNo ratings yet

- CHAPTER 5 - Portfolio TheoryDocument58 pagesCHAPTER 5 - Portfolio TheoryKabutu ChuungaNo ratings yet

- Chapter 11Document50 pagesChapter 11Randi ZamrajjasaNo ratings yet

- Prelim Good GovernanceDocument7 pagesPrelim Good GovernanceDDDNo ratings yet

- Introduction To Investment Decision in Financial Management (Open Compatibility)Document5 pagesIntroduction To Investment Decision in Financial Management (Open Compatibility)karl markxNo ratings yet

- 3 Promotion of Ethical Behavior in An OrganizationDocument2 pages3 Promotion of Ethical Behavior in An OrganizationAngelika Marimar RabeNo ratings yet

- Twenty-Three Investment CompaniesDocument17 pagesTwenty-Three Investment CompaniesMahendra SinghNo ratings yet

- Human Behavior in OrganizationDocument22 pagesHuman Behavior in Organizationmirmo tokiNo ratings yet

- AdjustmentsDocument34 pagesAdjustmentsFaiza ShahNo ratings yet

- Principal of Accounting-1Document34 pagesPrincipal of Accounting-1thefleetstrikerNo ratings yet

- Value Chain Management Capability A Complete Guide - 2020 EditionFrom EverandValue Chain Management Capability A Complete Guide - 2020 EditionNo ratings yet

- Velmonte vs. Belmonte (Case Digest)Document1 pageVelmonte vs. Belmonte (Case Digest)Vanz AsoqueNo ratings yet

- Industrial Finance Vs Ramirez, G.R. No. L-43821, May 26, 1977 - ANCELDocument7 pagesIndustrial Finance Vs Ramirez, G.R. No. L-43821, May 26, 1977 - ANCELLeizl A. VillapandoNo ratings yet

- Seatwork CH3&4Document2 pagesSeatwork CH3&4Jemely Bagang100% (1)

- Chapter 4 and 6 Full Text CasesDocument94 pagesChapter 4 and 6 Full Text Casessally deeNo ratings yet

- Transfer of Property Assignment Final - DoDocument30 pagesTransfer of Property Assignment Final - DoSom Dutt VyasNo ratings yet

- Premier BonusDocument2 pagesPremier BonusJane LyNo ratings yet

- 2Document2 pages2Maireen Jade NamoroNo ratings yet

- Reyes v. RCPI Employees Credit Union Inc.Document2 pagesReyes v. RCPI Employees Credit Union Inc.CeresjudicataNo ratings yet

- California Qui Tam False Claims Recording FeesDocument18 pagesCalifornia Qui Tam False Claims Recording Feesthorne1022No ratings yet

- International Financial Market Instruments: Presented ByDocument45 pagesInternational Financial Market Instruments: Presented BygeetshijNo ratings yet

- A Summary of Your Rights Under The Fair Credit Reporting ActDocument4 pagesA Summary of Your Rights Under The Fair Credit Reporting ActKathieNo ratings yet

- Lease Agreement Format - Lease Deed FormDocument3 pagesLease Agreement Format - Lease Deed FormAdarsh Kumar DubeleNo ratings yet

- Sme Study Modules For Quick Reference PDFDocument180 pagesSme Study Modules For Quick Reference PDFNilima ChowdhuryNo ratings yet

- 12 Florencio Fabillo and Josefa TanaDocument4 pages12 Florencio Fabillo and Josefa TanaMary Joy GorospeNo ratings yet

- Article VIII-: Selective Regulation of Bank OperationsDocument35 pagesArticle VIII-: Selective Regulation of Bank OperationsVirgilio CarpioNo ratings yet

- NABARDDocument40 pagesNABARDJesse LarsenNo ratings yet

- Deed of SaleDocument2 pagesDeed of SaleDamanMandaNo ratings yet

- 29) Chua Vs MesinaDocument4 pages29) Chua Vs MesinaMaima ZosaNo ratings yet

- AP 2006 (Liabilities) v2.0Document8 pagesAP 2006 (Liabilities) v2.0jalrestauroNo ratings yet

- Swarnajayanti Gram Swarozgar YojanaDocument13 pagesSwarnajayanti Gram Swarozgar YojanaKunal AggarwalNo ratings yet

- Business Mangement (3.4 Final Accounts)Document35 pagesBusiness Mangement (3.4 Final Accounts)Yatharth SejpalNo ratings yet

- Case Study On Inflation in IndiaDocument13 pagesCase Study On Inflation in IndiaAkash KamalNo ratings yet

- Land Bank of The Philippines, G.R. No. 190755Document20 pagesLand Bank of The Philippines, G.R. No. 190755Dexter CircaNo ratings yet

- HQP-HLF-006 Loan Restructuring Computation SheetDocument1 pageHQP-HLF-006 Loan Restructuring Computation Sheetmaxx villaNo ratings yet

- Bond Markets: Financial Markets and Institutions, 10e, Jeff MaduraDocument38 pagesBond Markets: Financial Markets and Institutions, 10e, Jeff MaduraYoga AdiNo ratings yet

- AntichresisDocument2 pagesAntichresiscrisypilNo ratings yet