You might also like

- Dmms Tutorial 4Document2 pagesDmms Tutorial 4Luis OvalleNo ratings yet

- Dmms Module 1 SlidesnDocument11 pagesDmms Module 1 SlidesnLuis OvalleNo ratings yet

- Dmms Module 2Document30 pagesDmms Module 2Luis OvalleNo ratings yet

- Dmms Module 4 SlidesDocument6 pagesDmms Module 4 SlidesLuis OvalleNo ratings yet

- Dmms Module 4Document29 pagesDmms Module 4Luis OvalleNo ratings yet

- Dmms Module 1Document11 pagesDmms Module 1Luis OvalleNo ratings yet

- ThwmbutiowDocument193 pagesThwmbutiowLuis OvalleNo ratings yet

- Cybergriping - Violating The Law While E-ComplainingDocument20 pagesCybergriping - Violating The Law While E-ComplainingLuis OvalleNo ratings yet

- Wells 2006 Applying Systems Engineering To NaDocument14 pagesWells 2006 Applying Systems Engineering To NaLuis OvalleNo ratings yet

- Anthony F Molland - Stephen R Turnock - Dominic A Hudson-Ship Resistance and Propulsion - Practical Estimation of Ship Propulsive Power-Cambridge University Press (2011)Document563 pagesAnthony F Molland - Stephen R Turnock - Dominic A Hudson-Ship Resistance and Propulsion - Practical Estimation of Ship Propulsive Power-Cambridge University Press (2011)ghanbari8668100% (1)

- Ref 4Document7 pagesRef 4kamarajchowdaryNo ratings yet

- MANTOD2014JanFeb2014 - 025 Send & Package para Esay 1Document3 pagesMANTOD2014JanFeb2014 - 025 Send & Package para Esay 1Luis OvalleNo ratings yet

- Rina 1860-2010 2010-2020Document92 pagesRina 1860-2010 2010-2020Luis OvalleNo ratings yet

- Including Navigation PatternsDocument16 pagesIncluding Navigation PatternsLuis OvalleNo ratings yet

- MEPC 1-Circ 878Document13 pagesMEPC 1-Circ 878Li Ann ChungNo ratings yet

- The Comma (,) : English, 2Document3 pagesThe Comma (,) : English, 2Luis OvalleNo ratings yet

- DNV GL - IMO Ship Implementation PlanDocument1 pageDNV GL - IMO Ship Implementation PlanShivani SarkarNo ratings yet

- Sulphur 2020: From Contracting To Final CombustionDocument24 pagesSulphur 2020: From Contracting To Final Combustionvran77No ratings yet

- 1 PDFDocument9 pages1 PDFAnnieNo ratings yet

- LR Marine Training Services Brochure Digital v1.0 PDFDocument16 pagesLR Marine Training Services Brochure Digital v1.0 PDFCristina Díaz ÁlvarezNo ratings yet

- MO Sulphur 2020 GuidanceDocument24 pagesMO Sulphur 2020 GuidanceF FNo ratings yet

- Vice-Chancellor's Leadership Program Guidelines 2019: Student Leadership, Career Development and EmploymentDocument13 pagesVice-Chancellor's Leadership Program Guidelines 2019: Student Leadership, Career Development and EmploymentLuis OvalleNo ratings yet

- Simple Solow Model: Savings Rate 0.238 Depreciation Rate 0.02 Technology A 1.46 Plot Range 1410Document2 pagesSimple Solow Model: Savings Rate 0.238 Depreciation Rate 0.02 Technology A 1.46 Plot Range 1410Luis OvalleNo ratings yet

- The Apostrophe (') : The Apostrophes and NounsDocument2 pagesThe Apostrophe (') : The Apostrophes and NounsLuis OvalleNo ratings yet

- 2013 Timothy Dickeson Ielts High Score VocabularyDocument38 pages2013 Timothy Dickeson Ielts High Score Vocabularymaxman11094% (18)

- 2013 Timothy Dickeson Ielts High Score VocabularyDocument38 pages2013 Timothy Dickeson Ielts High Score Vocabularymaxman11094% (18)

- Howitt Weil Economic GrowthDocument12 pagesHowitt Weil Economic GrowthLuis OvalleNo ratings yet

- Rand Rr1093Document294 pagesRand Rr1093Luis OvalleNo ratings yet

- A Contribution To The Empirics of Economic GrowthDocument32 pagesA Contribution To The Empirics of Economic GrowtharlenevieiraNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

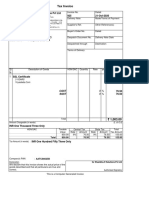

- Tax Invoice: Gstin/Uin: 24AABCY0257H1ZI State Name: Gujarat, Code: 24Document1 pageTax Invoice: Gstin/Uin: 24AABCY0257H1ZI State Name: Gujarat, Code: 24jayshah_26No ratings yet

- Kalp Shah Mobile: 9106359201 EmailDocument25 pagesKalp Shah Mobile: 9106359201 EmailBharathNo ratings yet

- In Thousand 60kg Bags: World Coffee ConsumptionDocument2 pagesIn Thousand 60kg Bags: World Coffee ConsumptionLia ElNo ratings yet

- + Why Subsidy and Dumping Is Closedly Linked?Document2 pages+ Why Subsidy and Dumping Is Closedly Linked?ALù DũngNo ratings yet

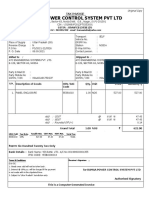

- Hinduja National Power Corporation LIMITED (Hinduja Power Plant)Document2 pagesHinduja National Power Corporation LIMITED (Hinduja Power Plant)Anurag AllaNo ratings yet

- Key Pointers For The RDM Role - TIEDDocument3 pagesKey Pointers For The RDM Role - TIEDNalla Thambi100% (1)

- Circular Debt in PakistanDocument17 pagesCircular Debt in PakistanHira Noor91% (11)

- Mind Map EcoDocument1 pageMind Map EcoJung JihyunNo ratings yet

- Ibe MCQDocument7 pagesIbe MCQLokesh Kawale0% (1)

- International Trade at A Casual Environment Exercise & Script - Listening ComprehensionDocument2 pagesInternational Trade at A Casual Environment Exercise & Script - Listening ComprehensionFrancisco J. Salinas B.No ratings yet

- Economics 1 Problem Set 5 - Suggested AnswersDocument5 pagesEconomics 1 Problem Set 5 - Suggested AnswersLi XiangNo ratings yet

- Insurance PpsDocument13 pagesInsurance Ppsaziz_sediqiNo ratings yet

- Amaia Payment SchemesDocument6 pagesAmaia Payment SchemesMhack ColisNo ratings yet

- Important Bank Mergers From 2017 To 2019: Merger of Bank of Baroda, Vijaya Bank, Dena BankDocument2 pagesImportant Bank Mergers From 2017 To 2019: Merger of Bank of Baroda, Vijaya Bank, Dena BankParasuRam37No ratings yet

- LEVI's SWOT and TOWS AnalysisDocument13 pagesLEVI's SWOT and TOWS AnalysisRakeysh Coomar67% (3)

- Real Estate in Israel - Y.H. Dimri Construction - Israel ExporterDocument1 pageReal Estate in Israel - Y.H. Dimri Construction - Israel ExporterIsrael ExporterNo ratings yet

- Using The Material Given in The Case Studies 1 & 2, Answer The Following QuestionsDocument1 pageUsing The Material Given in The Case Studies 1 & 2, Answer The Following QuestionsPRAKRITI SANKHLANo ratings yet

- Bill No. 162 Atc 08.09.2021Document3 pagesBill No. 162 Atc 08.09.2021TILAK RAJ KambojNo ratings yet

- Exam Kit E2 Answers EngDocument6 pagesExam Kit E2 Answers EngWasangLiNo ratings yet

- Tax Invoice: B.D. Inno Ventures Private LimitedDocument1 pageTax Invoice: B.D. Inno Ventures Private Limitedzeel dholakiyaNo ratings yet

- ASEB1102 Module 1 The Role of Agric in Economic DevelopmentDocument3 pagesASEB1102 Module 1 The Role of Agric in Economic Developmentdylan munyanyiNo ratings yet

- Russia Ukraine ConflictDocument3 pagesRussia Ukraine ConflictSimon DruryNo ratings yet

- Bcom Sem Vi Business EconomicsDocument36 pagesBcom Sem Vi Business EconomicsRamesh BabuNo ratings yet

- 7 - Bcom Benefits of GST To Economy and IndustryDocument13 pages7 - Bcom Benefits of GST To Economy and Industrymnr81No ratings yet

- World Trade: An Overview: - Who Trades With Whom?Document21 pagesWorld Trade: An Overview: - Who Trades With Whom?Bachuu HossanNo ratings yet

- Bill of Exchange 078Document1 pageBill of Exchange 078trung2iNo ratings yet

- Class 10th EconomicsDocument4 pagesClass 10th EconomicsNihalSoniNo ratings yet

- Meaning of Fema: Switch From FERADocument6 pagesMeaning of Fema: Switch From FERAAalok GhoshNo ratings yet

- Marcom PlanDocument2 pagesMarcom PlanSuhaib BaluchNo ratings yet

- Chapter 2 - Comparative Economic DevelopmentDocument62 pagesChapter 2 - Comparative Economic DevelopmentKenzel lawasNo ratings yet