You might also like

- The Financial System: Primary Function and InstitutionsDocument59 pagesThe Financial System: Primary Function and InstitutionsPratyush Goel100% (1)

- Indusind Bank Fiasco and The Sleeping Sentinels 1Document55 pagesIndusind Bank Fiasco and The Sleeping Sentinels 1SidNo ratings yet

- Effect of Drip Irrigation on Crop Yield and QualityDocument88 pagesEffect of Drip Irrigation on Crop Yield and Qualitysukhchain maan100% (1)

- All Metabolic Reactions That Use Proteins, Fats, and CarbohydratesDocument32 pagesAll Metabolic Reactions That Use Proteins, Fats, and Carbohydratesshannon c. lewisNo ratings yet

- Saving Food - Project ReportDocument19 pagesSaving Food - Project Reportapi-541958559No ratings yet

- Analysis of Financial Statements of IndusInd BankDocument19 pagesAnalysis of Financial Statements of IndusInd Bankcharu kapoorNo ratings yet

- Medicliam InsuranceDocument84 pagesMedicliam Insurancemanwanimuki12No ratings yet

- ANIL-FINAL Climate Change - Emerging Challenges For Sustainable DevelopmentDocument21 pagesANIL-FINAL Climate Change - Emerging Challenges For Sustainable DevelopmentanilbarikNo ratings yet

- Comparative Study of Reliance & Birla SunlifeDocument64 pagesComparative Study of Reliance & Birla SunlifeRohitParjapat100% (1)

- Marketing Strategies Analysis of Sri Lanka's Handloom IndustryDocument7 pagesMarketing Strategies Analysis of Sri Lanka's Handloom IndustryHiruni RajapakshaNo ratings yet

- Effects of Covid 19 To International TradeDocument4 pagesEffects of Covid 19 To International TradeWilliam Jefferson HomyaoNo ratings yet

- Report Hand Sanitizers Report 1 JuneDocument58 pagesReport Hand Sanitizers Report 1 JuneMarienNo ratings yet

- Product Mix DaburDocument29 pagesProduct Mix DaburgetgauravsbestNo ratings yet

- Agricultural FinanceDocument59 pagesAgricultural FinanceRizwan KhalidNo ratings yet

- Consumerism and Rise of Indian Middle ClassDocument12 pagesConsumerism and Rise of Indian Middle ClassPulkit AroraNo ratings yet

- Icici BankDocument33 pagesIcici BankpRiNcE DuDhAtRaNo ratings yet

- A Study of New Dimension of Direct Marketing by FMCG CompaniesDocument91 pagesA Study of New Dimension of Direct Marketing by FMCG CompaniesPrints BindingsNo ratings yet

- Agriculture Micro FinanceDocument18 pagesAgriculture Micro FinanceGaurav Sinha100% (1)

- Indian InsuranceDocument54 pagesIndian InsuranceMadhup Desai33% (3)

- Portfolio Analysis Banking SectorDocument40 pagesPortfolio Analysis Banking SectorMaster RajharshNo ratings yet

- IFR Magazine - April 11, 2020 PDFDocument102 pagesIFR Magazine - April 11, 2020 PDFChristian Del BarcoNo ratings yet

- FMCG Meaning Fast Moving Consumer GoodsDocument4 pagesFMCG Meaning Fast Moving Consumer GoodsSustain FitnessNo ratings yet

- A Novel One-Step Chemical Method For Preparation of Copper NanofluidsDocument4 pagesA Novel One-Step Chemical Method For Preparation of Copper NanofluidsbacNo ratings yet

- An In-Depth Study of Indian Consumer Durable IndustryDocument18 pagesAn In-Depth Study of Indian Consumer Durable Industrysaraswat2009No ratings yet

- Branded Cooking Oils Consumer BehaviorDocument22 pagesBranded Cooking Oils Consumer BehaviorHarshit KrishnaNo ratings yet

- Indian SugarDocument22 pagesIndian Sugardj2991No ratings yet

- Effects of Agricultural Credit On Agriculture OutputDocument21 pagesEffects of Agricultural Credit On Agriculture OutputHajra ANo ratings yet

- Dabur Vs ParachuteDocument14 pagesDabur Vs ParachutePrashant Raghav100% (1)

- FINAL PFR Report-Hand SanitizerDocument40 pagesFINAL PFR Report-Hand SanitizerKumar Prince RajNo ratings yet

- Housing Finance SystemsDocument45 pagesHousing Finance SystemsPriyanka100% (1)

- Internationalization of ExxonmobilDocument4 pagesInternationalization of ExxonmobilJuan FernandoNo ratings yet

- Buying Behaviour of Consumers Towards Instant Food ProductsDocument13 pagesBuying Behaviour of Consumers Towards Instant Food ProductsHarsh AnchaliaNo ratings yet

- IRCTC Performance AnalysisDocument44 pagesIRCTC Performance AnalysisRanjeet RajputNo ratings yet

- Grasim Industries Financial ReportsDocument8 pagesGrasim Industries Financial ReportsIshan GoyalNo ratings yet

- A Telemedicine Platform: A Case Study of Apollo Hospitals Telemedicine ProjectDocument25 pagesA Telemedicine Platform: A Case Study of Apollo Hospitals Telemedicine Projecttanushree26No ratings yet

- Direct MarketingDocument22 pagesDirect MarketingkidihhNo ratings yet

- HDFCDocument10 pagesHDFCSumit SinghNo ratings yet

- Final ProjectDocument73 pagesFinal ProjectShilpa NikamNo ratings yet

- Fatty Acid Market: Food & Feed 2% Candle 2% Various 5%Document5 pagesFatty Acid Market: Food & Feed 2% Candle 2% Various 5%Abdul AzizNo ratings yet

- Detailed Study of Edelweiss Tokio Life InsuranceDocument73 pagesDetailed Study of Edelweiss Tokio Life InsuranceHardik AgarwalNo ratings yet

- Banana Cultivation and Export Opportunities in Jalgaon RegionDocument31 pagesBanana Cultivation and Export Opportunities in Jalgaon RegionSuyog RaneNo ratings yet

- Literature Review of Microfinance SME in PakistanDocument7 pagesLiterature Review of Microfinance SME in PakistanSadiq Sagheer100% (1)

- Understanding HDFC Bank's Private Banking ServicesDocument18 pagesUnderstanding HDFC Bank's Private Banking Servicesritvik24No ratings yet

- Impact of Covid-19 On BusinessDocument8 pagesImpact of Covid-19 On BusinessPrajwal Vemala JagadeeshwaraNo ratings yet

- TYBBI ProjectDocument57 pagesTYBBI ProjectPranav ViraNo ratings yet

- Impact of Covid-19 On TranportationDocument42 pagesImpact of Covid-19 On TranportationAlyssa MasinagNo ratings yet

- A Study On Profitability Ratio Analysis of Britannia Biscuts India LTD - S.vijiDocument6 pagesA Study On Profitability Ratio Analysis of Britannia Biscuts India LTD - S.vijiInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- ITC Limited CSRDocument13 pagesITC Limited CSRRahul Purshottam100% (2)

- A Study On The Performance of Meghalaya Cooperative Apex BankDocument4 pagesA Study On The Performance of Meghalaya Cooperative Apex Bankhunrisha nongdharNo ratings yet

- CAMEL evaluation of Kotak Mahindra BankDocument22 pagesCAMEL evaluation of Kotak Mahindra BankAbideez PaNo ratings yet

- Strategic Management Mid ProjectDocument25 pagesStrategic Management Mid ProjectDea HandayaniNo ratings yet

- Ratio Analysis On Dabur India Ltd.Document62 pagesRatio Analysis On Dabur India Ltd.dheeraj dawar50% (2)

- Expensive Housing Turning Australia Into A Nation of RentersDocument3 pagesExpensive Housing Turning Australia Into A Nation of RentersJason NorthwoodNo ratings yet

- Repo Rate and Its Effect On GDP: An Empirical Indian ExperienceDocument11 pagesRepo Rate and Its Effect On GDP: An Empirical Indian ExperienceAnonymous CwJeBCAXpNo ratings yet

- Rural Banking and Agricultural FinancingDocument17 pagesRural Banking and Agricultural FinancingNilanshi MukherjeeNo ratings yet

- Thoosan Wheat Plate ProjectDocument56 pagesThoosan Wheat Plate ProjectApple Computers100% (2)

- Final PPT of IndusInd BankDocument14 pagesFinal PPT of IndusInd BanktruptiNo ratings yet

- Investing in Natural Capital for a Sustainable Future in the Greater Mekong SubregionFrom EverandInvesting in Natural Capital for a Sustainable Future in the Greater Mekong SubregionNo ratings yet

- The Press ReleaseDocument19 pagesThe Press ReleaseRafa BorgesNo ratings yet

- VIV PR Vivendi Q1 2022 RevenuesDocument9 pagesVIV PR Vivendi Q1 2022 RevenuesRafa BorgesNo ratings yet

- Z! ( - ! "!) " "! ""! ! ! "! #"!) ! ! !) ! - ) ! - (! !) (! "! ! (! ! (!) "! ! (! ( - ! ZZ! - ) ") !) ! (! ! " ! ZZZ! - ) ") !) ! (! ! " !Document2 pagesZ! ( - ! "!) " "! ""! ! ! "! #"!) ! ! !) ! - ) ! - (! !) (! "! ! (! ! (!) "! ! (! ( - ! ZZ! - ) ") !) ! (! ! " ! ZZZ! - ) ") !) ! (! ! " !Rafa BorgesNo ratings yet

- 2Q22 Alcoa Financial ResultsDocument16 pages2Q22 Alcoa Financial ResultsRafa BorgesNo ratings yet

- Z! ( - ! "!) " "! ""! ! ! "! #"!) ! ! !) ! - ) ! - (! !) (! "! ! (! ! (!) "! ! (! ( - ! ZZ! - ) ") !) ! (! ! " ! ZZZ! - ) ") !) ! (! ! " !Document2 pagesZ! ( - ! "!) " "! ""! ! ! "! #"!) ! ! !) ! - ) ! - (! !) (! "! ! (! ! (!) "! ! (! ( - ! ZZ! - ) ") !) ! (! ! " ! ZZZ! - ) ") !) ! (! ! " !Rafa BorgesNo ratings yet

- Powell Testimony 1-11-22Document4 pagesPowell Testimony 1-11-22Joseph Adinolfi Jr.No ratings yet

- R 20220218Document2 pagesR 20220218Rafa BorgesNo ratings yet

- Ipc S 924 FGV Press Release 0Document3 pagesIpc S 924 FGV Press Release 0Rafa BorgesNo ratings yet

- R 20220225Document2 pagesR 20220225Rafa BorgesNo ratings yet

- Boletim FocusDocument2 pagesBoletim FocusTacio Lorran SilvaNo ratings yet

- R 20220107Document2 pagesR 20220107Rafa BorgesNo ratings yet

- Adp National Employment Report December2021 Final Press ReleaseDocument5 pagesAdp National Employment Report December2021 Final Press ReleaseRafa BorgesNo ratings yet

- R 20211231Document2 pagesR 20211231Rafa BorgesNo ratings yet

- C P I - N 2021Document38 pagesC P I - N 2021Rafa BorgesNo ratings yet

- R 20211203Document2 pagesR 20211203Rafa BorgesNo ratings yet

- Unemployment Insurance Weekly Claims Nov. 24, 2021Document12 pagesUnemployment Insurance Weekly Claims Nov. 24, 2021Katie CrolleyNo ratings yet

- Relatório Focus 22/11/2021Document2 pagesRelatório Focus 22/11/2021Tacio Lorran SilvaNo ratings yet

- Fomc Minutes 20210922Document13 pagesFomc Minutes 20210922ZerohedgeNo ratings yet

- Z# ( - ! # $# ") $" $!# $$# # !" # $# %!$#) !" ! # # !#) !# - ! ) # - ! (# #) (!# $# # (# # (# !!) $# # " (# ( - ! # ZZ# ! - ) $) #) # " (# # $" # ZZZ# ! - ) $) #) # " (# # $" # "Document2 pagesZ# ( - ! # $# ") $" $!# $$# # !" # $# %!$#) !" ! # # !#) !# - ! ) # - ! (# #) (!# $# # (# # (# !!) $# # " (# ( - ! # ZZ# ! - ) $) #) # " (# # $" # ZZZ# ! - ) $) #) # " (# # $" # "Rafa BorgesNo ratings yet

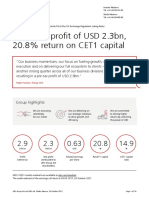

- 3Q21 Net Profit of USD 2.3bn, 20.8% Return On CET1 Capital: Group HighlightsDocument14 pages3Q21 Net Profit of USD 2.3bn, 20.8% Return On CET1 Capital: Group HighlightsRafa BorgesNo ratings yet

- Supply and Demand Imbalances Related ToDocument5 pagesSupply and Demand Imbalances Related ToRafa BorgesNo ratings yet

- Unemployment Insurance Weekly Claims 10.14.21Document12 pagesUnemployment Insurance Weekly Claims 10.14.21Katie Crolley100% (1)

- Wells FargoDocument11 pagesWells FargoRafa BorgesNo ratings yet

- Morgan StanleyDocument9 pagesMorgan StanleyRafa BorgesNo ratings yet

- Bank of America Reports Q3-21 Net Income of $7.7 Billion, EPS of $0.85Document19 pagesBank of America Reports Q3-21 Net Income of $7.7 Billion, EPS of $0.85Rafa BorgesNo ratings yet

- R 20211008Document2 pagesR 20211008Rafa BorgesNo ratings yet

- Unemployment Insurance Weekly Claims 10.14.21Document12 pagesUnemployment Insurance Weekly Claims 10.14.21Katie Crolley100% (1)

- PayrollDocument41 pagesPayrollRafa BorgesNo ratings yet

- Z" ( - " #" !) #! # " ##" " ! " #" $ #") ! " " ") " - ) " - (" ") (" #" " (" " (") #" " ! (" ( - " ZZ" - ) #) ") " ! (" " #! " ZZZ" - ) #) ") " ! (" " #! " !Document2 pagesZ" ( - " #" !) #! # " ##" " ! " #" $ #") ! " " ") " - ) " - (" ") (" #" " (" " (") #" " ! (" ( - " ZZ" - ) #) ") " ! (" " #! " ZZZ" - ) #) ") " ! (" " #! " !Rafa BorgesNo ratings yet

- R 20211001Document2 pagesR 20211001Tacio Lorran SilvaNo ratings yet

- Justin Valenti Unit2 Part3Document14 pagesJustin Valenti Unit2 Part3JustinValentiNo ratings yet

- Laporan Mingguan 2021Document293 pagesLaporan Mingguan 2021AMMNo ratings yet

- Deliverable Commodities Under RegistrationDocument6 pagesDeliverable Commodities Under RegistrationPhương NguyễnNo ratings yet

- Key Cerrado Deforesters Linked To The Clearing of More Than 110000 HectaresDocument16 pagesKey Cerrado Deforesters Linked To The Clearing of More Than 110000 HectaresRafa BorgesNo ratings yet

- Marketing The Core 7th Edition Kerin Test Bank 1Document52 pagesMarketing The Core 7th Edition Kerin Test Bank 1jeffrey100% (49)

- Saumya Agarwal ResumeDocument1 pageSaumya Agarwal ResumeArisha NarangNo ratings yet

- The Benefits of Working with FibersolDocument8 pagesThe Benefits of Working with FibersolSri. SiriNo ratings yet

- ADM - GFSI - Audit ReportDocument28 pagesADM - GFSI - Audit ReportWasim ArshadNo ratings yet

- DanieDocument12 pagesDanieRINTAN FALAH ISPRIDEVINo ratings yet

- FA Europe Past AttendeesDocument35 pagesFA Europe Past AttendeesCesarNo ratings yet

- 33Document42 pages33seaseow9No ratings yet

- Marketing The Core 6Th Edition Kerin Test Bank Full Chapter PDFDocument36 pagesMarketing The Core 6Th Edition Kerin Test Bank Full Chapter PDFfay.rowden768100% (12)

- Directory of Export Elevators Including Facility Data USDA FGIS 2012Document61 pagesDirectory of Export Elevators Including Facility Data USDA FGIS 2012William DavisNo ratings yet

- History of the Global Citric Acid Industry DevelopmentDocument26 pagesHistory of the Global Citric Acid Industry Developmenterfan davariNo ratings yet

- ADM and LG Chem To Develop Sustainable Technology For Superabsorbent PolymersDocument2 pagesADM and LG Chem To Develop Sustainable Technology For Superabsorbent PolymersEng Hau QuaNo ratings yet

- ARCHAR CASE StudyDocument2 pagesARCHAR CASE StudyzainNo ratings yet

- WG 2013 10 01Document108 pagesWG 2013 10 01ersNo ratings yet

- "Our Customers Are Our Enemies" - The Lysine Cartel - ConnorFileDocument19 pages"Our Customers Are Our Enemies" - The Lysine Cartel - ConnorFileIvy WNo ratings yet

- 2022 Nus Invest Responses & Stock Pitch ReportDocument12 pages2022 Nus Invest Responses & Stock Pitch ReportDev DesaiNo ratings yet

- vessels_sailed_update (16)Document10 pagesvessels_sailed_update (16)Lê Quyết ChungNo ratings yet