You might also like

- Module 3 Nominal and Effective IRDocument18 pagesModule 3 Nominal and Effective IRMeifrinaldiGamaBizenNo ratings yet

- Module 3 Nominal and Effective IRDocument19 pagesModule 3 Nominal and Effective IRkikiNo ratings yet

- Module 3 Nominal and Effective IR - RevDocument20 pagesModule 3 Nominal and Effective IR - RevTerra PradanaNo ratings yet

- INDE 232-Chapter3Document29 pagesINDE 232-Chapter3Abdullah AfefNo ratings yet

- 7 Interest Lec5Document52 pages7 Interest Lec5Marco ConopioNo ratings yet

- Module 3: Nominal and Effective Interest Rates: SI-4151 Ekonomi TeknikDocument21 pagesModule 3: Nominal and Effective Interest Rates: SI-4151 Ekonomi TeknikSanjika IlhamNo ratings yet

- Module 3 Nominal and Effective IRDocument24 pagesModule 3 Nominal and Effective IRtori doriNo ratings yet

- Module 3 Nominal and Effective IRDocument19 pagesModule 3 Nominal and Effective IRTimbul SihotangNo ratings yet

- Lecture No. 4 Nominal and Effective Interest Rates 1. GeneralDocument7 pagesLecture No. 4 Nominal and Effective Interest Rates 1. GeneralRadha RampalliNo ratings yet

- PPT02 - Nominal and Effective Interest RatesDocument33 pagesPPT02 - Nominal and Effective Interest RatesImam Al GhazaliNo ratings yet

- ENGINEERING ECONOMY - Nomınal - and - Effective - InterestDocument18 pagesENGINEERING ECONOMY - Nomınal - and - Effective - InterestBlessing FajemirokunNo ratings yet

- Econimics (Nominal&Effective)Document38 pagesEconimics (Nominal&Effective)api-26367767No ratings yet

- CH 4 Effective - InterestDocument23 pagesCH 4 Effective - InterestRashadafanehNo ratings yet

- Nominal and Effective Interest RatesDocument7 pagesNominal and Effective Interest Ratessj199325No ratings yet

- Econ - 4Document14 pagesEcon - 4Adrianne CespedesNo ratings yet

- Chapter 4-Nominal and Effective Interest Rates - 0Document24 pagesChapter 4-Nominal and Effective Interest Rates - 0dalbaasNo ratings yet

- Pertemuan 4 Nominal and Effective Interest RatesDocument115 pagesPertemuan 4 Nominal and Effective Interest Ratesreprano PNo ratings yet

- CH3. Sample QuestionsDocument11 pagesCH3. Sample QuestionsMaria Charity Flores OrañoNo ratings yet

- Module 3 Nominal and Effective IRDocument19 pagesModule 3 Nominal and Effective IRRhonita Dea Andarini100% (1)

- Nominal and Effective Interest Rates: CE 314 Engineering EconomyDocument30 pagesNominal and Effective Interest Rates: CE 314 Engineering EconomySaad Hanif SardarNo ratings yet

- Advanced Engineering Economics: Nominal and Effective Interest RatesDocument21 pagesAdvanced Engineering Economics: Nominal and Effective Interest RatesA GlaumNo ratings yet

- Nominal and Effective Interest Rates: EC - Lec 08Document23 pagesNominal and Effective Interest Rates: EC - Lec 08Junaid YNo ratings yet

- Engineering Economy Lecture21 WisDocument35 pagesEngineering Economy Lecture21 WisMelissa Delgado100% (1)

- Lecture 07Document10 pagesLecture 07Muhammad Shoaib Aslam KhichiNo ratings yet

- 2 Nominal and Effective Interest Rate 2015Document11 pages2 Nominal and Effective Interest Rate 2015Muhammad SaepudinNo ratings yet

- Engineering Economics (MS-291) : Lecture # 12Document15 pagesEngineering Economics (MS-291) : Lecture # 12samadNo ratings yet

- Lecture 2 - Interest and Money - Engg EconomyDocument22 pagesLecture 2 - Interest and Money - Engg EconomyFrenz Villasis100% (1)

- Simple InterestDocument31 pagesSimple InterestShiela YuNo ratings yet

- CE22 - 06 - Nominal Effective Interest RateDocument42 pagesCE22 - 06 - Nominal Effective Interest RateMarco ConopioNo ratings yet

- 03-Interest RateDocument9 pages03-Interest RatehilyauliaNo ratings yet

- CHAPTER 4 Mathematics of FinanceDocument66 pagesCHAPTER 4 Mathematics of FinanceHailemariamNo ratings yet

- SHS GENMATH AY 23-24 8 Business MathematicsDocument70 pagesSHS GENMATH AY 23-24 8 Business Mathematics11-13D MANAIG MattNo ratings yet

- Engineering Economics: Ali SalmanDocument10 pagesEngineering Economics: Ali SalmanZargham KhanNo ratings yet

- 04 Nominal and Effective Interest RatesDocument26 pages04 Nominal and Effective Interest Rates王泓鈞No ratings yet

- Engineering Economics: Ali SalmanDocument11 pagesEngineering Economics: Ali SalmanAli Haider RizviNo ratings yet

- Ecnomic Notes 2Document4 pagesEcnomic Notes 2ehnzdhmNo ratings yet

- Engineering Economics (MS-291) : Lecture # 13Document32 pagesEngineering Economics (MS-291) : Lecture # 13samadNo ratings yet

- Compound Interest: Simple Interest vs. Compound Interest Formula Sample ProblemsDocument46 pagesCompound Interest: Simple Interest vs. Compound Interest Formula Sample ProblemsRoselle Malabanan100% (1)

- Engineering Economics: Ali SalmanDocument11 pagesEngineering Economics: Ali SalmanUsama FarooqNo ratings yet

- EC07Document22 pagesEC07engrsaab51No ratings yet

- Gen Math Lesson 23 Compounding More Than Once A YearDocument18 pagesGen Math Lesson 23 Compounding More Than Once A Yeardelimaernesto10No ratings yet

- Lesson I. Simple and Compound InterestDocument6 pagesLesson I. Simple and Compound InterestKaren BrionesNo ratings yet

- Simple and Compound Interest: Ryan Jeffrey P Curbano, PH.DDocument35 pagesSimple and Compound Interest: Ryan Jeffrey P Curbano, PH.DPrince RiveraNo ratings yet

- Varying Rates: Learning OutcomesDocument12 pagesVarying Rates: Learning OutcomesMay FadlNo ratings yet

- Present Value Compounded More Than Once A YearDocument14 pagesPresent Value Compounded More Than Once A YearAllaine BenitezNo ratings yet

- Engineering Economy Lecture2Document32 pagesEngineering Economy Lecture2Jaed CaraigNo ratings yet

- Ch.4 Math of Finance-1Document19 pagesCh.4 Math of Finance-1hildamezmur9No ratings yet

- Chapter 4Document8 pagesChapter 4ObeydullahKhanNo ratings yet

- REVIEWER For PRE-FINALSDocument5 pagesREVIEWER For PRE-FINALSBeaNo ratings yet

- MathDocument6 pagesMathLyndMargaretteVicencioNo ratings yet

- Unit 4: Mathematics of FinanceDocument34 pagesUnit 4: Mathematics of FinanceDawit MekonnenNo ratings yet

- Compounding More Than Once A YearDocument14 pagesCompounding More Than Once A YearAllaine BenitezNo ratings yet

- Compounding More Than Once A YearDocument7 pagesCompounding More Than Once A Yearprincessnylighte13No ratings yet

- Diploma in Management Studies Business Mathematics BUS003: Learning OutcomesDocument25 pagesDiploma in Management Studies Business Mathematics BUS003: Learning OutcomesgglvNo ratings yet

- HuewwwDocument20 pagesHuewwwWex Senin AlcantaraNo ratings yet

- Topic 4 Mathematics of FinanceDocument66 pagesTopic 4 Mathematics of FinanceAndrew PillayNo ratings yet

- AnnuitiesDocument6 pagesAnnuitiesFaith MagluyanNo ratings yet

- Mathematics of FinanceDocument25 pagesMathematics of FinanceJulianna CortezNo ratings yet

- Mike FM HD 2DDocument148 pagesMike FM HD 2Dzulma siregarNo ratings yet

- Module 11 DepreciationDocument15 pagesModule 11 Depreciationzulma siregarNo ratings yet

- Module 8 Benefit Cost RatioDocument13 pagesModule 8 Benefit Cost Ratiozulma siregarNo ratings yet

- Lesson Plan: CV 4103 Methodology AND Technology OF ConstructionDocument20 pagesLesson Plan: CV 4103 Methodology AND Technology OF Constructionzulma siregarNo ratings yet

- Analisis Produktivitas Alat Berat Quarry Mardinding JuluDocument3 pagesAnalisis Produktivitas Alat Berat Quarry Mardinding Juluzulma siregarNo ratings yet

- Lesson Plan: CV 4103 Methodology AND Technology OF ConstructionDocument20 pagesLesson Plan: CV 4103 Methodology AND Technology OF Constructionzulma siregarNo ratings yet

- Module 4 Present Worth AnalysisDocument38 pagesModule 4 Present Worth Analysiszulma siregarNo ratings yet

- Module 5 Annual Worth AnalysisDocument22 pagesModule 5 Annual Worth Analysiszulma siregarNo ratings yet

- 07 Time Value of Money - BE ExercisesDocument26 pages07 Time Value of Money - BE ExercisesMUNDADA VENKATESH SURESH PGP 2019-21 BatchNo ratings yet

- Dissertation Report SumandeepDocument82 pagesDissertation Report SumandeepSumandeep Kaur Chambial0% (1)

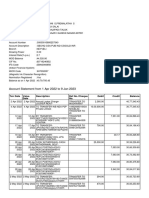

- Account Statement From 1 Apr 2022 To 9 Jan 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 1 Apr 2022 To 9 Jan 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSelva maniNo ratings yet

- Analysis of Financial Performance of Selected Commercial Banks in IndiaDocument18 pagesAnalysis of Financial Performance of Selected Commercial Banks in IndiaSadaf SayedqejklpNo ratings yet

- Why Do You Need A Payment Gateway For WebsiteDocument8 pagesWhy Do You Need A Payment Gateway For WebsiteAshrithaNo ratings yet

- Chime Chapman Go Fund MeDocument2 pagesChime Chapman Go Fund Mekevin.dirst77No ratings yet

- Private Placement Term SheetDocument2 pagesPrivate Placement Term Sheetunoguru100% (1)

- Builder NOC FormatDocument2 pagesBuilder NOC FormatvikrameyeNo ratings yet

- Phil. Deposit Insurance Corp. v. CA and AbadDocument2 pagesPhil. Deposit Insurance Corp. v. CA and AbadKaren Ryl Lozada BritoNo ratings yet

- Daily Cash BookDocument192 pagesDaily Cash BookKrishnakumar Balakrishnan100% (1)

- Chapter 5 DUTYDocument19 pagesChapter 5 DUTYtemedebereNo ratings yet

- H.D.F.C .Standard Life Insurance.Document5 pagesH.D.F.C .Standard Life Insurance.Atharva SaxenaNo ratings yet

- PMC Bank Scam: Banking OperationsDocument10 pagesPMC Bank Scam: Banking Operationssakshi kaul0% (1)

- House Bank ConfigurationDocument3 pagesHouse Bank Configurationcriclover_gNo ratings yet

- Factoring and ForfaitingDocument21 pagesFactoring and ForfaitingDilip RajNo ratings yet

- Resume Petty Cash and Bank ReconcilliationDocument3 pagesResume Petty Cash and Bank ReconcilliationYuliaNo ratings yet

- Dimple Prajapat: Create Modify CancelDocument1 pageDimple Prajapat: Create Modify CancelRAJASTHAN REFRIGERATIONNo ratings yet

- Welcome To Transport Department Government of Telangana - IndiaDocument1 pageWelcome To Transport Department Government of Telangana - IndiaPrakash ReddyNo ratings yet

- Final Project NPA MANAGEMENT IN BANKSDocument88 pagesFinal Project NPA MANAGEMENT IN BANKSmanish223283% (18)

- Dasmariñas Lending Services: Loan Application FormDocument3 pagesDasmariñas Lending Services: Loan Application FormMark RyeNo ratings yet

- Tata Motors Finance Solutions LTD Cardex I (Contract Details)Document4 pagesTata Motors Finance Solutions LTD Cardex I (Contract Details)speed TubeNo ratings yet

- Session 4 International FinanceDocument4 pagesSession 4 International FinanceTumbleweedNo ratings yet

- Intern ReportDocument137 pagesIntern ReportSaifNo ratings yet

- Internship Report On MCB (PIA Society Branch) 2013 by Azka Sumbel, IBITDocument133 pagesInternship Report On MCB (PIA Society Branch) 2013 by Azka Sumbel, IBITAzka Sumbel QM IbNo ratings yet

- Islamic Finance and The Digital Revolution: Vita ArumsariDocument9 pagesIslamic Finance and The Digital Revolution: Vita Arumsaridido edoNo ratings yet

- Did Deutsch-Institut Worldwide: Invoice 55873Document1 pageDid Deutsch-Institut Worldwide: Invoice 55873Celal KuyuNo ratings yet

- Cheque Collection Policy 2020 21Document27 pagesCheque Collection Policy 2020 21Hareesh LNo ratings yet

- Crossing of ChequesDocument5 pagesCrossing of ChequesRavneet KaurNo ratings yet

- FAC1502 Study Unit 8 2021Document27 pagesFAC1502 Study Unit 8 2021edsonNo ratings yet

- Silos vs. PNB PDFDocument24 pagesSilos vs. PNB PDFdanexrainierNo ratings yet