You might also like

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Actvity 4 in Auditing 4 - Biological AssetsDocument3 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Implement Strategy StructureDocument21 pagesImplement Strategy StructurePaupau100% (1)

- Activity - Derivatives and Hedging Accounting (PFRS 9)Document8 pagesActivity - Derivatives and Hedging Accounting (PFRS 9)PaupauNo ratings yet

- Activity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)Document1 pageActivity - Translation of Foreign Currency Financial Statements (PAS 21 & PAS 29)PaupauNo ratings yet

- Accounting for Cash, Receivables and InventoriesDocument12 pagesAccounting for Cash, Receivables and InventoriesPaupau100% (1)

- Assessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerDocument12 pagesAssessment No. 6 MAS 06 Standard Costing Multiple Choice Problems: Choose The Letter of The Correct AnswerPaupauNo ratings yet

- Audit 4 - Audit in Specialized IndustryDocument7 pagesAudit 4 - Audit in Specialized IndustryPaupauNo ratings yet

- Assignment On PCF and Bank ReconDocument2 pagesAssignment On PCF and Bank ReconPaupauNo ratings yet

- Activity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0Document6 pagesActivity - Consolidated Financial Statement - Part 2 (1) (REVIEWER MIDTERM0PaupauNo ratings yet

- AFAR ReviewDocument11 pagesAFAR ReviewPaupauNo ratings yet

- Activity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Document12 pagesActivity - Consolidated Financial Statement, Part 1 (REVIEWER MIDTERM)Paupau0% (1)

- Activity On Application ControlDocument5 pagesActivity On Application ControlPaupauNo ratings yet

- Activity 2 Audit On CISDocument4 pagesActivity 2 Audit On CISPaupauNo ratings yet

- Special Purpose Audit Procedures and ReportsDocument6 pagesSpecial Purpose Audit Procedures and ReportsPaupauNo ratings yet

- Answer in Prelim Exam E4.Document12 pagesAnswer in Prelim Exam E4.PaupauNo ratings yet

- Activity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Document11 pagesActivity - Home Office, Branch Accounting & Business Combination (REVIEWER MIDTERM)Paupau100% (1)

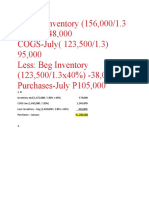

- Ending Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000Document1 pageEnding Inventory (156,000/1.3 x40%) P48,000 COGS-July (123,500/1.3) 95,000 Less: Beg Inventory (123,500/1.3x40%) - 38,000 Purchases-July P105,000PaupauNo ratings yet

- Activity 3 - CAATsDocument4 pagesActivity 3 - CAATsPaupauNo ratings yet

- Estimated transaction price methods and entries for consignment salesDocument7 pagesEstimated transaction price methods and entries for consignment salesPaupauNo ratings yet

- Answers - Partnership AccountingDocument14 pagesAnswers - Partnership AccountingPaupauNo ratings yet

- Actvity 4 in Auditing 4 - Biological AssetsDocument2 pagesActvity 4 in Auditing 4 - Biological AssetsPaupauNo ratings yet

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- Answer in Act. 2 For Cash-receivables-InventoriesDocument10 pagesAnswer in Act. 2 For Cash-receivables-InventoriesPaupauNo ratings yet

- MAS-04 Relevant CostingDocument10 pagesMAS-04 Relevant CostingPaupauNo ratings yet

- Management Accounting Techniques CompilationDocument40 pagesManagement Accounting Techniques CompilationGracelle Mae Oraller100% (1)

- 6 Business StrategyDocument27 pages6 Business StrategyPaupauNo ratings yet

- PAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesDocument9 pagesPAULA GOZUN - Activity 2 Accounting For Cash-receivables-InventoriesPaupauNo ratings yet

- Activity - Consolidated Financial Statement Part 1Document10 pagesActivity - Consolidated Financial Statement Part 1PaupauNo ratings yet

- Assessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerDocument12 pagesAssessment No. 4 MAS-04 Relevant Costing I. Multiple Choice Theory: Choose The Letter of The Best AnswerPaupauNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Scribd Letter To Donald Tusk Regarding EU and UK Trade Deal After Brexit.Document1 pageScribd Letter To Donald Tusk Regarding EU and UK Trade Deal After Brexit.morganistNo ratings yet

- Accounting Equation and Double Entry BookkeepingDocument29 pagesAccounting Equation and Double Entry BookkeepingArvin ToraldeNo ratings yet

- Cash Management ModelsDocument2 pagesCash Management ModelsyukesrajaNo ratings yet

- Almc - Cash Position - 11may2021Document246 pagesAlmc - Cash Position - 11may2021ACYATAN & CO., CPAs 2020No ratings yet

- Regulatory Framework of Merchant BankingDocument12 pagesRegulatory Framework of Merchant BankingKirti Khattar60% (5)

- National Research Foundation to Boost India's Research OutputDocument48 pagesNational Research Foundation to Boost India's Research OutputR JayalathNo ratings yet

- Nike FY05 06 CR Report CDocument162 pagesNike FY05 06 CR Report CShehzad Ashraf100% (1)

- 2 Break-Even Analysis - AssignmentDocument2 pages2 Break-Even Analysis - AssignmentNamanNo ratings yet

- Https:/pipipl In/brochure PDFDocument15 pagesHttps:/pipipl In/brochure PDFCreative IdeasNo ratings yet

- Agriculture and Allied SectorDocument24 pagesAgriculture and Allied SectorAbhishek MishraNo ratings yet

- RandS Module1Document6 pagesRandS Module1Lingahan EricaNo ratings yet

- PL 108-27 Jobs and Growth Tax Relief Reconciliation Act of 2003Document18 pagesPL 108-27 Jobs and Growth Tax Relief Reconciliation Act of 2003Tax HistoryNo ratings yet

- NO Page Number: 1 Executive Summary 1-2Document26 pagesNO Page Number: 1 Executive Summary 1-2AMITaXWINo ratings yet

- DCF Model of Bharti Airtel: AssumptionsDocument4 pagesDCF Model of Bharti Airtel: AssumptionsHARSHIL RATHINo ratings yet

- KFC Matrics in PakistanDocument3 pagesKFC Matrics in PakistanSuleman Iqbal BhattiNo ratings yet

- Internship Program.: ProposalDocument5 pagesInternship Program.: ProposalstrangerNo ratings yet

- Full N Final by Ajay PDFDocument85 pagesFull N Final by Ajay PDFAjay RajbharNo ratings yet

- Customer FocusDocument17 pagesCustomer Focussanjai yadavNo ratings yet

- Bagmati PTMPDocument108 pagesBagmati PTMPPraveen BhandariNo ratings yet

- Demonetisation The Nielsen ViewDocument4 pagesDemonetisation The Nielsen ViewShriram SNo ratings yet

- Hyderabad Metropolitan Water Supply and Sewerage BoardDocument1 pageHyderabad Metropolitan Water Supply and Sewerage BoardKhalid KhanNo ratings yet

- History of Competition LawDocument17 pagesHistory of Competition LawshubhamNo ratings yet

- CIR v. Algue, Inc., G.R. No. L-28896Document1 pageCIR v. Algue, Inc., G.R. No. L-28896fay garneth buscato100% (2)

- Audit Cum Risk Compliance Officer, Provisional ResultDocument15 pagesAudit Cum Risk Compliance Officer, Provisional ResultWAQAS AHMEDNo ratings yet

- AE211 Final ExamDocument10 pagesAE211 Final ExamMariette Alex AgbanlogNo ratings yet

- Vitality-Case Analysis: Vitality Health Enterprises IncDocument5 pagesVitality-Case Analysis: Vitality Health Enterprises IncChristina Williams0% (1)

- Depreciation MethodsDocument25 pagesDepreciation Methodsluvy acerdenNo ratings yet

- Understanding How To Identify Emerging Issues Will Assist Tourism and Hospitality Organisations To Be More SuccessfulDocument5 pagesUnderstanding How To Identify Emerging Issues Will Assist Tourism and Hospitality Organisations To Be More SuccessfulvalentinaNo ratings yet

- Summary SIA Ch.13 - Expenditure CycleDocument3 pagesSummary SIA Ch.13 - Expenditure CycleAthiyya Nabila AyuNo ratings yet

- Fa IiiDocument76 pagesFa Iiirishav agarwalNo ratings yet