You might also like

- Taxation ReviewerDocument19 pagesTaxation ReviewerjwualferosNo ratings yet

- Module 3 - Value Added TaxDocument113 pagesModule 3 - Value Added TaxAllan C. MarquezNo ratings yet

- Percentage TaxesDocument6 pagesPercentage TaxesCarmela JimenezNo ratings yet

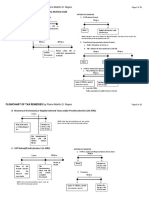

- Flowchart of Tax Remedies I. Remedies UnDocument12 pagesFlowchart of Tax Remedies I. Remedies UnKevin Ken Sison Ganchero100% (2)

- ZHINENG Qigong Breathing Exercises ZBEDocument12 pagesZHINENG Qigong Breathing Exercises ZBELong Le100% (4)

- Taxation of Individuals QuizzerDocument37 pagesTaxation of Individuals QuizzerCharry Ramos62% (13)

- Create LawDocument200 pagesCreate Lawtara bajarlaNo ratings yet

- TRAIN Law Lecture by Dr. Lim PDFDocument12 pagesTRAIN Law Lecture by Dr. Lim PDFAnonymous 8SUSyvGc3d100% (1)

- Managing Birs Tax Assessment FreeebookDocument88 pagesManaging Birs Tax Assessment FreeebookJohn Patrick Guillen100% (1)

- Vi. Securities Regulation Code (RA 8799)Document14 pagesVi. Securities Regulation Code (RA 8799)ARIS100% (1)

- 1 Income Tax ReviewerDocument69 pages1 Income Tax ReviewerPrincess Galang100% (1)

- RA 10963 TRAIN Law SummaryDocument74 pagesRA 10963 TRAIN Law Summaryrandyblanza2014100% (5)

- Taxation Law - NIRC Vs TRAINDocument3 pagesTaxation Law - NIRC Vs TRAINGemma F. Tiama100% (2)

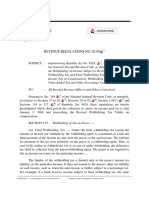

- RR 12-1999Document21 pagesRR 12-1999anorith8867% (6)

- TRAIN Vs CREATEDocument6 pagesTRAIN Vs CREATEleejongsukNo ratings yet

- Corporation TRAIN and CREATE LawDocument8 pagesCorporation TRAIN and CREATE LawdgdeguzmanNo ratings yet

- SGV - CREATE Bill Dec 14 2020Document64 pagesSGV - CREATE Bill Dec 14 2020Bien Bowie A. Cortez100% (2)

- TAX REMEDIES AND FILING REQUIREMENTSDocument11 pagesTAX REMEDIES AND FILING REQUIREMENTSNingning Carios100% (1)

- Improperly Accumulated Earnings TaxDocument4 pagesImproperly Accumulated Earnings TaxSophia OñateNo ratings yet

- SGV and Co Presentation On TRAIN LawDocument48 pagesSGV and Co Presentation On TRAIN LawPortCalls100% (8)

- Taxation Law Updates by Atty. OrtegaDocument21 pagesTaxation Law Updates by Atty. Ortegavillanueva9guapster9100% (1)

- Bachelor of Science in Accountancy: Program Curriculum Ay 2020 - 2021Document10 pagesBachelor of Science in Accountancy: Program Curriculum Ay 2020 - 2021AZGH HOSPITAL /Cyberdyne PhilippinesNo ratings yet

- BIR Ruling (DA-005-07) (Travel Agencies) PDFDocument4 pagesBIR Ruling (DA-005-07) (Travel Agencies) PDFAl Marvin0% (1)

- Annexes TOS Effective October 2022Document37 pagesAnnexes TOS Effective October 2022Rhad Estoque100% (12)

- VolvoTD70 Service Manual EngineDocument110 pagesVolvoTD70 Service Manual EngineHeikki Alakontiola87% (47)

- Feu Estate TaxDocument17 pagesFeu Estate Taxlouise carino100% (1)

- Income Taxation QuizzerDocument41 pagesIncome Taxation QuizzerMarriz Tan100% (4)

- JBDimaampao - Train Law and Tax UpdatesDocument19 pagesJBDimaampao - Train Law and Tax UpdateshlcameroNo ratings yet

- VAT 101: Understanding Value Added TaxDocument13 pagesVAT 101: Understanding Value Added TaxKara Clark100% (1)

- Withholding Taxes SeminarDocument99 pagesWithholding Taxes SeminarLeilani Delgado Moselina0% (1)

- MCQ REVIEW: TAXATION PRINCIPLESDocument21 pagesMCQ REVIEW: TAXATION PRINCIPLESJill Ante100% (1)

- Taxation Under The Train Law: 1 - PageDocument30 pagesTaxation Under The Train Law: 1 - PageMae50% (2)

- BLT Final Pre-Boards NCPARDocument12 pagesBLT Final Pre-Boards NCPARlorenceabad07No ratings yet

- Tax2 - Ch1-5 Estate Taxes ReviewerDocument8 pagesTax2 - Ch1-5 Estate Taxes ReviewerMaia Castañeda100% (15)

- Tax Law Review Course OverviewDocument14 pagesTax Law Review Course OverviewEduard Riparip100% (2)

- CPAR TAX - Other Percentage Taxes PDFDocument13 pagesCPAR TAX - Other Percentage Taxes PDFJohn Carlo CruzNo ratings yet

- General Principles of Taxation June 2019 College of LawDocument89 pagesGeneral Principles of Taxation June 2019 College of LawJoanna Marie100% (1)

- RR 2-98Document136 pagesRR 2-98hizelaryaNo ratings yet

- PAS-PFRS FinalDocument107 pagesPAS-PFRS FinalPaul Christian H. BelaosNo ratings yet

- PFRS For Small Entities Illustrative FS (Early Adoption)Document55 pagesPFRS For Small Entities Illustrative FS (Early Adoption)Jake Aseo Bertulfo50% (2)

- Key amendments in the Tax Code under the CREATE billDocument2 pagesKey amendments in the Tax Code under the CREATE billJean TomugdanNo ratings yet

- RR 2-98Document85 pagesRR 2-98Elaine LatonioNo ratings yet

- CPA Board Exam Quizzer Vol. 2Document13 pagesCPA Board Exam Quizzer Vol. 2John Mahatma AgripaNo ratings yet

- RR 2-98Document3 pagesRR 2-98mnyng100% (3)

- For Domestic Corporations: 1. Salient Features of The CREATE LawDocument6 pagesFor Domestic Corporations: 1. Salient Features of The CREATE LawJean Tomugdan100% (1)

- Fish Processing CGDocument41 pagesFish Processing CGmelisasumbilon100% (1)

- TAX REMEDIES by Sababan Reviewer 2008 EdDocument11 pagesTAX REMEDIES by Sababan Reviewer 2008 Edolaydyosa95% (20)

- BIR Revenue Regulations No. 2-98Document93 pagesBIR Revenue Regulations No. 2-98Maan EspinosaNo ratings yet

- TAX First Preboard 2021Document10 pagesTAX First Preboard 2021Ser Crz JyNo ratings yet

- CFM56 3Document148 pagesCFM56 3manmohan100% (1)

- Tax: TRAIN Illustrative Problems: Long Problem With FormsDocument23 pagesTax: TRAIN Illustrative Problems: Long Problem With FormsNooroddenNo ratings yet

- Katalog Baylan Vodomjer 1-2Document1 pageKatalog Baylan Vodomjer 1-2Edin Dervishi100% (1)

- Condensate Drain Calculation - Lab AHU PDFDocument1 pageCondensate Drain Calculation - Lab AHU PDFAltaf KhanNo ratings yet

- AMLA Summary: Key Provisions and Definitions of the Philippine Anti-Money Laundering ActDocument61 pagesAMLA Summary: Key Provisions and Definitions of the Philippine Anti-Money Laundering ActJames CantorneNo ratings yet

- G.R. No 198799, G.R. No. 229722, G.R. No. 189218Document2 pagesG.R. No 198799, G.R. No. 229722, G.R. No. 189218MACNo ratings yet

- Gross Incom TaxationDocument32 pagesGross Incom TaxationSummer ClaronNo ratings yet

- Tax Remedies Final 4 SlidesDocument35 pagesTax Remedies Final 4 SlidesMisterpogi TalagaNo ratings yet

- MCQ On TaxationDocument24 pagesMCQ On TaxationZed AbantasNo ratings yet

- TAX-CPAR Lecture Filing and Penalties Version 2Document23 pagesTAX-CPAR Lecture Filing and Penalties Version 2YamateNo ratings yet

- Taxation Module 3 5Document57 pagesTaxation Module 3 5Ma VyNo ratings yet

- BOARD OF ACCOUNTANCY ResolutionDocument9 pagesBOARD OF ACCOUNTANCY ResolutionKristine Loide A. Timtim-Rojas100% (1)

- CREATE Act lowers taxes to support Philippine businessesDocument3 pagesCREATE Act lowers taxes to support Philippine businesseskaren mariz manaNo ratings yet

- CREATE ManualDocument98 pagesCREATE ManualGenny JovellanosNo ratings yet

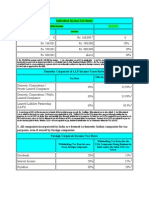

- Individual and Corporate Income Tax Rates in IndiaDocument3 pagesIndividual and Corporate Income Tax Rates in IndiaKhalid QuadriNo ratings yet

- Regular Income Taxation - Regular CorporationDocument9 pagesRegular Income Taxation - Regular Corporationdelacruzrojohn600No ratings yet

- CombinepdfDocument39 pagesCombinepdfLoise MorenoNo ratings yet

- Chapter 5 - Corporate Income TaxDocument25 pagesChapter 5 - Corporate Income Taxtkldiablo1211No ratings yet

- Red Biotechnology ProjectDocument5 pagesRed Biotechnology ProjectMahendrakumar ManiNo ratings yet

- Banking Question PapersDocument12 pagesBanking Question Papersmohak khinNo ratings yet

- Designing a Chlorobenzene PlantDocument13 pagesDesigning a Chlorobenzene PlantAram Nasih MuhammadNo ratings yet

- CP107 Vol II-ERT 2B - 12-Dec 2019 (PA) - 3Document209 pagesCP107 Vol II-ERT 2B - 12-Dec 2019 (PA) - 3NghiaNo ratings yet

- Organozinc CompoundDocument8 pagesOrganozinc Compoundamanuel tafeseNo ratings yet

- Dycaico Vs SssDocument1 pageDycaico Vs SssGladys Bustria OrlinoNo ratings yet

- Applications of Proton Exchange Membrane Fuel CellDocument20 pagesApplications of Proton Exchange Membrane Fuel CellRiri SasyNo ratings yet

- Formula Costo SandblastingDocument20 pagesFormula Costo SandblastingSerch VillaNo ratings yet

- Covid19 - Attendance Book, Visitors Book, Field AuditDocument7 pagesCovid19 - Attendance Book, Visitors Book, Field AuditmakhalNo ratings yet

- Comparative Study of Soaps of Hul P Amp G Godrej Nirma and Johnson Amp Johnson 130410234307 Phpapp01 PDFDocument71 pagesComparative Study of Soaps of Hul P Amp G Godrej Nirma and Johnson Amp Johnson 130410234307 Phpapp01 PDFdheeraj agarwalNo ratings yet

- Can You Distinguish Neutral, Formal and Informal Among The Following Groups of WordsDocument3 pagesCan You Distinguish Neutral, Formal and Informal Among The Following Groups of WordsВікторія РудаNo ratings yet

- Acidified Foods Guidance 2010-08-02 (Clean)Document39 pagesAcidified Foods Guidance 2010-08-02 (Clean)Victor SchneiderNo ratings yet

- The Bone DreamingDocument3 pagesThe Bone DreamingastrozzNo ratings yet

- De Thi Thu Vao 10 Mon Tieng Anh Quan Dong Da Ha NoiDocument5 pagesDe Thi Thu Vao 10 Mon Tieng Anh Quan Dong Da Ha NoiTrang VuongNo ratings yet

- EKS 17 Miniature Piston Pump SpecificationsDocument1 pageEKS 17 Miniature Piston Pump SpecificationsdujobozinovicNo ratings yet

- Anxiety DisordersDocument40 pagesAnxiety Disordersamal abdulrahmanNo ratings yet

- Monnal T50 VentilatorsDocument2 pagesMonnal T50 VentilatorsInnovate IndiaNo ratings yet

- 17EEX01-FUNDAMENTALS OF FIBRE OPTICS AND LASER INSTRUMENTATION SyllabusDocument2 pages17EEX01-FUNDAMENTALS OF FIBRE OPTICS AND LASER INSTRUMENTATION SyllabusJayakumar ThangavelNo ratings yet

- Anatomía Relacional de Los Músculos MiméticosDocument5 pagesAnatomía Relacional de Los Músculos MiméticosLizeth Conde OrozcoNo ratings yet

- TDS Wabo Elastodec EDocument3 pagesTDS Wabo Elastodec EaomareltayebNo ratings yet

- SPE 35687 Environmentally Safe Burner For Offshore Well Testing OperationsDocument12 pagesSPE 35687 Environmentally Safe Burner For Offshore Well Testing OperationsTheNourEldenNo ratings yet

- Wood Gas Generator or NLDocument94 pagesWood Gas Generator or NLToddharrisNo ratings yet

- BurgerKing Versus McDonaldsDocument4 pagesBurgerKing Versus McDonaldsmarkus johannessenNo ratings yet