You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 14 AdjustmentsssDocument7 pages14 AdjustmentsssZaheer Ahmed SwatiNo ratings yet

- FS For GR IR Automatic ClearingDocument10 pagesFS For GR IR Automatic ClearingHridya PrasadNo ratings yet

- Audit of Hospital - Mcom Part II ProjectDocument28 pagesAudit of Hospital - Mcom Part II ProjectKunal KapoorNo ratings yet

- Specimen Examen F3 AccaDocument21 pagesSpecimen Examen F3 AccaGNo ratings yet

- Core Banking Solutions: Andhra Pradesh Grameena Vikas Bank Head Office, WarangalDocument8 pagesCore Banking Solutions: Andhra Pradesh Grameena Vikas Bank Head Office, WarangalleenardniNo ratings yet

- FNDACT2 Corporations PDFDocument11 pagesFNDACT2 Corporations PDFEl YangNo ratings yet

- Chapter 11: Inventory Cost Flow Cost Formula PAS 2, Paragraph 25 States That The Cost of Inventory Should Be A. Fifo B. Weighted AverageDocument7 pagesChapter 11: Inventory Cost Flow Cost Formula PAS 2, Paragraph 25 States That The Cost of Inventory Should Be A. Fifo B. Weighted AverageYami HeatherNo ratings yet

- Oracle Financial Tables DescriptionDocument15 pagesOracle Financial Tables Descriptionrv90470No ratings yet

- Problem 2-3B: Name: Section: ScoreDocument10 pagesProblem 2-3B: Name: Section: ScoreAlba LunaNo ratings yet

- Nov 2023Document7 pagesNov 2023applybizzNo ratings yet

- Valuation Concepts and MethodsDocument5 pagesValuation Concepts and MethodsYami HeatherNo ratings yet

- BPI v. Court of Appeals 255 SCRA 571 G.R. No. 116792 March 29 1996Document2 pagesBPI v. Court of Appeals 255 SCRA 571 G.R. No. 116792 March 29 1996Hurjae Soriano Lubag100% (4)

- Financial AccountingDocument2 pagesFinancial AccountingYami HeatherNo ratings yet

- Lower of Cost Net Realizable ValueDocument1 pageLower of Cost Net Realizable ValueYami HeatherNo ratings yet

- IFRS 15 SolutionsDocument8 pagesIFRS 15 SolutionsYami HeatherNo ratings yet

- IFRS 15 Examples and ExercisesDocument10 pagesIFRS 15 Examples and ExercisesYami Heather0% (1)

- How To Rescue Someone From Drowning?Document13 pagesHow To Rescue Someone From Drowning?Yami HeatherNo ratings yet

- Volleyball Rules and PrinciplesDocument8 pagesVolleyball Rules and PrinciplesYami HeatherNo ratings yet

- Govac Chap 6Document5 pagesGovac Chap 6Yami HeatherNo ratings yet

- Fair Value VS Fair Market ValueDocument4 pagesFair Value VS Fair Market ValueYami HeatherNo ratings yet

- CFAS and ACC RulesDocument72 pagesCFAS and ACC RulesYami HeatherNo ratings yet

- Ap10 Conceptual FrameworkDocument16 pagesAp10 Conceptual FrameworkYami HeatherNo ratings yet

- Govacct ReviewerDocument4 pagesGovacct ReviewerYami HeatherNo ratings yet

- Economics and Financial Accounting Module: By: Mrs. Shubhangi DixitDocument68 pagesEconomics and Financial Accounting Module: By: Mrs. Shubhangi DixitGladwin JosephNo ratings yet

- Intro To Accounting Ch. 2Document5 pagesIntro To Accounting Ch. 2Bambang HasmaraningtyasNo ratings yet

- Chapter 6: Accounting For RetailingDocument5 pagesChapter 6: Accounting For RetailingDanh PhanNo ratings yet

- Banking Transaction Financial Accounting Entries - SAP Account Posting - FICO (Financial Accounting and Controlling) - STechiesDocument5 pagesBanking Transaction Financial Accounting Entries - SAP Account Posting - FICO (Financial Accounting and Controlling) - STechiesAnandNo ratings yet

- CHA Certification Study Guide Volume IDocument483 pagesCHA Certification Study Guide Volume IReda KeraghelNo ratings yet

- The Shareholders Are General Agents of The Business. Pre-Emptive RightDocument20 pagesThe Shareholders Are General Agents of The Business. Pre-Emptive RightSaeym SegoviaNo ratings yet

- Liabilities Part 2Document4 pagesLiabilities Part 2Jay LloydNo ratings yet

- Bop & International Economics LinkagesDocument77 pagesBop & International Economics LinkagesGaurav Kumar100% (2)

- Problems 2:: Date Particulars/ Description Ref. Debit CreditDocument3 pagesProblems 2:: Date Particulars/ Description Ref. Debit CreditShajadul BijoyNo ratings yet

- Solutions To Exercises - Chap 3Document27 pagesSolutions To Exercises - Chap 3InciaNo ratings yet

- Chapter 4 - Admission of A PartnerDocument110 pagesChapter 4 - Admission of A Partnerakshaya sangeethaNo ratings yet

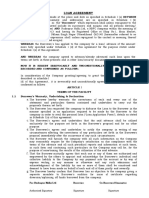

- Loan Agreement: For Rudrapur Nidhi LTD Borrower Co-Borrower/Guarantor Signature SignatureDocument7 pagesLoan Agreement: For Rudrapur Nidhi LTD Borrower Co-Borrower/Guarantor Signature SignatureMiddha Law Firm Rudrapur100% (1)

- 1 ch07 Cash - Warren Reeve WajibDocument40 pages1 ch07 Cash - Warren Reeve WajibAdilaNo ratings yet

- Accounting Principles: The Recording ProcessDocument55 pagesAccounting Principles: The Recording ProcessRabie HarounNo ratings yet

- Advance AccountingDocument5 pagesAdvance AccountingChristopher PriceNo ratings yet

- L3 - ABFA1163 FA II (Student)Document14 pagesL3 - ABFA1163 FA II (Student)Xue YikNo ratings yet

- 7110 s11 QP 21Document20 pages7110 s11 QP 21mstudy123456No ratings yet

- Lecture NoteDocument30 pagesLecture NoteHana YusriNo ratings yet