You might also like

- Q-6 Spr-08 (Yahya Limited) Q ADocument2 pagesQ-6 Spr-08 (Yahya Limited) Q AiamneonkingNo ratings yet

- Microsoft ValuationDocument4 pagesMicrosoft ValuationcorvettejrwNo ratings yet

- Microsoft Vs Intuit ValuationDocument4 pagesMicrosoft Vs Intuit ValuationcorvettejrwNo ratings yet

- MFA Test 1 SolutionDocument4 pagesMFA Test 1 SolutionMuhammad ImranNo ratings yet

- Management Accounting: Page 1 of 6Document70 pagesManagement Accounting: Page 1 of 6Ahmed Raza MirNo ratings yet

- Group B&D Case 19 FonderiaDocument12 pagesGroup B&D Case 19 FonderiaVinithi ThongkampalaNo ratings yet

- Latihan Soal Week 8Document6 pagesLatihan Soal Week 8Natasya Prashta WidyadhariNo ratings yet

- To Calculate Equity Value Through DCF Analysis: DATA INPUTS - Those Highlighted Are Those GivenDocument4 pagesTo Calculate Equity Value Through DCF Analysis: DATA INPUTS - Those Highlighted Are Those GivenYash ModiNo ratings yet

- Investment Outlays at Time 0Document3 pagesInvestment Outlays at Time 0jualNo ratings yet

- Cost and Management Accounting: Page 1 of 8Document8 pagesCost and Management Accounting: Page 1 of 8Ibtehaj KayaniNo ratings yet

- Plywood Project Report by Yogesh AgrawalDocument22 pagesPlywood Project Report by Yogesh AgrawalYOGESH AGRAWALNo ratings yet

- Island Power (IPWR) Incremental Earning Forecast For The Project (Purchasing Machine Outright) From The Year 2017-2022Document4 pagesIsland Power (IPWR) Incremental Earning Forecast For The Project (Purchasing Machine Outright) From The Year 2017-2022Ruma RashydNo ratings yet

- Ca Inter Cost Management Accounting Test 2 Unscheduled Solution 598020012022Document14 pagesCa Inter Cost Management Accounting Test 2 Unscheduled Solution 598020012022Deppanshu KhandelwalNo ratings yet

- Complete Investment Appraisal - 2Document7 pagesComplete Investment Appraisal - 2Reagan SsebbaaleNo ratings yet

- Smaller Plant 1996 1997 1998 1999Document9 pagesSmaller Plant 1996 1997 1998 1999Ehtisham AkhtarNo ratings yet

- NPV Lesson 2Document5 pagesNPV Lesson 2Barack MikeNo ratings yet

- Group 5Document16 pagesGroup 5Amelia AndrianiNo ratings yet

- P8Document17 pagesP8ShivamNo ratings yet

- Tutorial 2 Manufacturing Account 2 AnswerDocument15 pagesTutorial 2 Manufacturing Account 2 AnswerNG JIA LUNGNo ratings yet

- Business Finance Decision Suggested Solution Test # 2: Answer - 1Document4 pagesBusiness Finance Decision Suggested Solution Test # 2: Answer - 1Syed Muhammad Kazim RazaNo ratings yet

- Financial Slide For ReportDocument6 pagesFinancial Slide For ReportTuan Noridham Tuan LahNo ratings yet

- Advanced Corporate Finance Case 2Document3 pagesAdvanced Corporate Finance Case 2Adrien PortemontNo ratings yet

- Statement - I Cost of Project Particulars Sl. No. Ref. Annex Total CostDocument15 pagesStatement - I Cost of Project Particulars Sl. No. Ref. Annex Total Costsohalsingh1No ratings yet

- Essay FIN202Document5 pagesEssay FIN202thaindnds180468No ratings yet

- 2022 12 01 Answer Key Additional M6 M7Document15 pages2022 12 01 Answer Key Additional M6 M7Niger RomeNo ratings yet

- Exercises On Joint Cost and By-ProductsDocument2 pagesExercises On Joint Cost and By-ProductsVixen Aaron EnriquezNo ratings yet

- Altman Z Score CalculatorDocument2 pagesAltman Z Score CalculatorSelva Bavani SelwaduraiNo ratings yet

- Case 5Document12 pagesCase 5JIAXUAN WANGNo ratings yet

- Acquisition Cash FlowDocument3 pagesAcquisition Cash Flowkaeya alberichNo ratings yet

- Process costing: ﺻ ﻔ ﺣ ﺔ ا ﻟﺑ ﺎ ﺣ ث ا ﻟ ﻌ ﻠ ﻣ ﻲ ﻋ ﻼ ء ﻣ ﺣ ﺳ ن ﺷ ﺣ م ﺗﻠ ﻛ ر ا م @aliasreiDocument14 pagesProcess costing: ﺻ ﻔ ﺣ ﺔ ا ﻟﺑ ﺎ ﺣ ث ا ﻟ ﻌ ﻠ ﻣ ﻲ ﻋ ﻼ ء ﻣ ﺣ ﺳ ن ﺷ ﺣ م ﺗﻠ ﻛ ر ا م @aliasreiDr. M. SamyNo ratings yet

- Materi Untuk Tugas Topik 2Document11 pagesMateri Untuk Tugas Topik 2Violen AmeliaNo ratings yet

- Chapter 9 Divisional Transfer Pricing Nov2020 1Document90 pagesChapter 9 Divisional Transfer Pricing Nov2020 1Priyanka LunavatNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document6 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Income StatementDocument2 pagesIncome StatementChille Nchimunya BwalyaNo ratings yet

- A. Generate The Cumulative (Non-Discounted) After-Tax Cash Flow DiagramDocument13 pagesA. Generate The Cumulative (Non-Discounted) After-Tax Cash Flow DiagramHaziq Hakimi100% (1)

- CTA LEVEL 2 FT - Financial Accounting Test 2 2021 - SolutionDocument3 pagesCTA LEVEL 2 FT - Financial Accounting Test 2 2021 - SolutioncuthbertNo ratings yet

- Instructor: Assumptions / InputsDocument17 pagesInstructor: Assumptions / InputsJoAnna MonfilsNo ratings yet

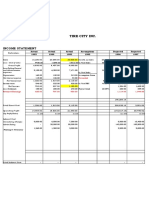

- Tire City IncDocument18 pagesTire City IncSoumyajitNo ratings yet

- Joint Product & By-Product ExamplesDocument15 pagesJoint Product & By-Product ExamplesMuhammad azeemNo ratings yet

- Discounted Cash Flows at WACCDocument11 pagesDiscounted Cash Flows at WACCapi-15357496No ratings yet

- Management AccountingDocument6 pagesManagement AccountingBornyNo ratings yet

- Ch16 HW3Document3 pagesCh16 HW3boerd77No ratings yet

- Deltron Company's Break Even Analysis Particulars Amount: PV RatioDocument7 pagesDeltron Company's Break Even Analysis Particulars Amount: PV RatiorajyalakshmiNo ratings yet

- P1 Solution Dec 2018Document6 pagesP1 Solution Dec 2018Awal ShekNo ratings yet

- Profit and Loss ProjectionDocument1 pageProfit and Loss ProjectionAbel GetachewNo ratings yet

- Barotiwala EnerDocument11 pagesBarotiwala EnerAshish MishraNo ratings yet

- 4 2006 Dec ADocument5 pages4 2006 Dec Aapi-19836745No ratings yet

- Is Fishing Non Motorized BangkaDocument4 pagesIs Fishing Non Motorized BangkaAnonymous EvbW4o1U7No ratings yet

- Particulars P1 P2Document4 pagesParticulars P1 P2sanket pareekNo ratings yet

- CoffeeCube SampleDocument13 pagesCoffeeCube Samplelthanhhuyen15No ratings yet

- Pma Test 1 2022Document6 pagesPma Test 1 2022Janielle LambertNo ratings yet

- Balance Sheet: Sources of FundsDocument8 pagesBalance Sheet: Sources of FundschandrajitkNo ratings yet

- Universiti Utara Malaysia Bwff2043 Advanced Financial Management (Group A) SECOND SEMESTER SESSION 2019/2020 (A192)Document10 pagesUniversiti Utara Malaysia Bwff2043 Advanced Financial Management (Group A) SECOND SEMESTER SESSION 2019/2020 (A192)Hirosha VejianNo ratings yet

- Corporate Valuation: Group - 2Document6 pagesCorporate Valuation: Group - 2RiturajPaulNo ratings yet

- ACB 10203 Tutorial Cost Allocation With SolutionDocument5 pagesACB 10203 Tutorial Cost Allocation With SolutionainfarhanaNo ratings yet

- S-2022 SolDocument9 pagesS-2022 SolMuhammad NawazNo ratings yet

- Abans QuarterlyDocument14 pagesAbans QuarterlyGFMNo ratings yet

- f5 Worksheet BPPDocument19 pagesf5 Worksheet BPPYashna SohawonNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Past Paper HW Auto IndustriesDocument1 pagePast Paper HW Auto IndustriesShehrozSTNo ratings yet

- Solution Ifrs 16 QuizDocument6 pagesSolution Ifrs 16 QuizShehrozSTNo ratings yet

- Solutions of Revision Session by AMK Sept 2020 AttemptDocument13 pagesSolutions of Revision Session by AMK Sept 2020 AttemptShehrozSTNo ratings yet

- Standard Costing Practice Questions FinalDocument5 pagesStandard Costing Practice Questions FinalShehrozSTNo ratings yet

- Standard Costing Homework Questions FinalDocument2 pagesStandard Costing Homework Questions FinalShehrozSTNo ratings yet

- Solutions Consolidation-FormattedDocument22 pagesSolutions Consolidation-FormattedShehrozSTNo ratings yet

- Past Paper HW Auto IndustriesDocument1 pagePast Paper HW Auto IndustriesShehrozSTNo ratings yet

- Solutions IAS 1 For SEPT ATTEMPT FinalDocument25 pagesSolutions IAS 1 For SEPT ATTEMPT FinalShehrozSTNo ratings yet

- ROSE LTD Spring18Q6Document4 pagesROSE LTD Spring18Q6ShehrozSTNo ratings yet

- Syllabus Changes For Acca Qualification Exams:: Guidance For Students Impacted by June 2020 Exam CancellationsDocument23 pagesSyllabus Changes For Acca Qualification Exams:: Guidance For Students Impacted by June 2020 Exam CancellationsAmjad Ali100% (1)

- Financial Accounting and Reporting Ii: Examinable SupplementDocument30 pagesFinancial Accounting and Reporting Ii: Examinable SupplementShehrozSTNo ratings yet

- Internship Report On Bank Islami by Owais ShafiqueDocument300 pagesInternship Report On Bank Islami by Owais ShafiqueOwais ShafiqueNo ratings yet

- Variance IQ FileDocument34 pagesVariance IQ FileShehrozSTNo ratings yet

- Variance IQ FileDocument34 pagesVariance IQ FileShehrozSTNo ratings yet

- Shortcut For TOCsDocument2 pagesShortcut For TOCsShehrozSTNo ratings yet

- Sample CVDocument1 pageSample CVShehrozSTNo ratings yet

- Standard Costing Homework Questions FinalDocument2 pagesStandard Costing Homework Questions FinalShehrozSTNo ratings yet

- Solution Ifrs 16 QuizDocument6 pagesSolution Ifrs 16 QuizShehrozSTNo ratings yet

- Sir Saud Tariq: 13 Important Revision Questions On Each TopicDocument29 pagesSir Saud Tariq: 13 Important Revision Questions On Each TopicShehrozST100% (1)

- Standard Costing Practice Questions FinalDocument5 pagesStandard Costing Practice Questions FinalShehrozSTNo ratings yet

- Quiz - 01 - Solution - 15th December 2018Document5 pagesQuiz - 01 - Solution - 15th December 2018ShehrozSTNo ratings yet

- Shortcut For Substanive ProceduresDocument1 pageShortcut For Substanive ProceduresShehrozSTNo ratings yet

- Cost and Management Accounting Quiz - 1Document3 pagesCost and Management Accounting Quiz - 1ShehrozSTNo ratings yet

- Updated ULTIMATE INDUCTION GUIDEDocument15 pagesUpdated ULTIMATE INDUCTION GUIDEShehrozSTNo ratings yet

- GIFT - CAF 8 Master Questions With Solutions & Marks - Caf 8 Sir Saud Tariq ST AcademyDocument36 pagesGIFT - CAF 8 Master Questions With Solutions & Marks - Caf 8 Sir Saud Tariq ST AcademyShehrozSTNo ratings yet

- Suggested Answers Certificate in Accounting and Finance - Autumn 2016Document7 pagesSuggested Answers Certificate in Accounting and Finance - Autumn 2016ShehrozSTNo ratings yet

- CMA CAF-8 Important TheoryDocument14 pagesCMA CAF-8 Important TheoryShehrozSTNo ratings yet

- Grand Mock CMA CAF 8 With Solution Sir Saud Tariq ST AcademyDocument15 pagesGrand Mock CMA CAF 8 With Solution Sir Saud Tariq ST AcademyShehrozST100% (2)

- Chapter 1 - Inventory Valuation: Caf-08 Cma Complete TheoryDocument8 pagesChapter 1 - Inventory Valuation: Caf-08 Cma Complete TheoryShehrozSTNo ratings yet

- CafDocument5 pagesCaftokeeer100% (1)

- Full Download Operations Management Sustainability and Supply Chain Management Canadian 2nd Edition Heizer Solutions Manual PDF Full ChapterDocument23 pagesFull Download Operations Management Sustainability and Supply Chain Management Canadian 2nd Edition Heizer Solutions Manual PDF Full Chapterrengtressful5ysnt100% (20)

- A Descriptive Analysis of Consumer'S Adoption of E-WalletsDocument19 pagesA Descriptive Analysis of Consumer'S Adoption of E-WalletsAndrea TugotNo ratings yet

- Lone Pine CafeDocument4 pagesLone Pine CafeRahul TiwariNo ratings yet

- SL - No. Company Building Name Unit No. Floor NoDocument25 pagesSL - No. Company Building Name Unit No. Floor Novijay kumar anantNo ratings yet

- Deed of Assignment With AssumptionDocument3 pagesDeed of Assignment With AssumptionJecky Delos ReyesNo ratings yet

- A CAT Corp MRP SolnDocument12 pagesA CAT Corp MRP Solnakshay kushNo ratings yet

- Implementation of CMMS Software For A Maintenance Plan in A Manufacturing IndustryDocument4 pagesImplementation of CMMS Software For A Maintenance Plan in A Manufacturing IndustryZegera MgendiNo ratings yet

- Final Output OjTDocument8 pagesFinal Output OjTMatthew FerrerNo ratings yet

- Marine Insurance (Chapter 08)Document16 pagesMarine Insurance (Chapter 08)Abu Muhammad Hatem TohaNo ratings yet

- Sms Legalnotice 6093535-27788993Document2 pagesSms Legalnotice 6093535-27788993Prince AbhiNo ratings yet

- PhilipsVsMatsushit Case AnalysisDocument7 pagesPhilipsVsMatsushit Case AnalysisGaurav RanjanNo ratings yet

- Business Simulation Games Report DPDocument6 pagesBusiness Simulation Games Report DPaashutosh guptaNo ratings yet

- Executive Summary: Sources and Application of FundsDocument6 pagesExecutive Summary: Sources and Application of FundsJimmy DagupanNo ratings yet

- A Personal Selling Strategy: DevelopingDocument14 pagesA Personal Selling Strategy: DevelopingAdeesh KakkarNo ratings yet

- Check List For Various Noc's: ../affidavit For Consent To Establish ../affidavit For Consent To Operate PDFDocument23 pagesCheck List For Various Noc's: ../affidavit For Consent To Establish ../affidavit For Consent To Operate PDFshubham kumarNo ratings yet

- Building Permit ChecklistDocument1 pageBuilding Permit Checklistar desNo ratings yet

- Directions: Complete The Financial Report Worksheet To Help You With Your Calculations To CreateDocument8 pagesDirections: Complete The Financial Report Worksheet To Help You With Your Calculations To CreateAshley GoletNo ratings yet

- ScreeningDocument28 pagesScreeningMaria SetianingsihNo ratings yet

- Chap 1Document30 pagesChap 1ሻሎም ሃፒ ታዲNo ratings yet

- Finals in GbermicDocument2 pagesFinals in GbermicElizabeth CanadaNo ratings yet

- BR - MGK PrintingDocument2 pagesBR - MGK Printingsourav84No ratings yet

- Criteria For Supplier Selection: A Literature Review: ArticleDocument6 pagesCriteria For Supplier Selection: A Literature Review: ArticleMohammed ShahinNo ratings yet

- DTI Ratio SpreadsDocument7 pagesDTI Ratio SpreadsFranklin HallNo ratings yet

- Project Timeline de Pus Planned Jos: Q1 January FebruaryDocument20 pagesProject Timeline de Pus Planned Jos: Q1 January FebruaryAlexandruDanielNo ratings yet

- SLT eBill-00372777690152ImageDocument1 pageSLT eBill-00372777690152ImageDushshantha Gayashan0% (1)

- Calasanz V CIRDocument6 pagesCalasanz V CIRevelyn b t.No ratings yet

- The Toilet Paper Entrepreneur PDFDocument198 pagesThe Toilet Paper Entrepreneur PDFMarco Gómez Caballero83% (6)

- Sr. Acc Suroor ResumeDocument2 pagesSr. Acc Suroor ResumeVaibhav VermaNo ratings yet

- Daily Market ReportDocument7 pagesDaily Market ReportPriya RathoreNo ratings yet

- 10 - Chapter 3 Security in M CommerceDocument39 pages10 - Chapter 3 Security in M CommercehariharankalyanNo ratings yet