You might also like

- Dita Eka Nur Sakina - Tugas P14Document8 pagesDita Eka Nur Sakina - Tugas P14Dita EnsNo ratings yet

- Tugas AKM IIDocument3 pagesTugas AKM IIDaniel TanakaNo ratings yet

- Tugas Kel 3 (P14.2, P14.4)Document7 pagesTugas Kel 3 (P14.2, P14.4)Alexandra AmadeaNo ratings yet

- Tugas Ch.14Document6 pagesTugas Ch.14Chupa HesNo ratings yet

- Name: Solution Problem: P14-2, Issuance and Retirement of Bonds Course: DateDocument8 pagesName: Solution Problem: P14-2, Issuance and Retirement of Bonds Course: DateRegina PutriNo ratings yet

- Exercise 14Document11 pagesExercise 14dwitaNo ratings yet

- Answers - Chapter 2 Vol 2 RvsedDocument13 pagesAnswers - Chapter 2 Vol 2 Rvsedjamflox100% (3)

- Agricultural Development Bank Limited: Unaudited Financial Results (Quarterly)Document3 pagesAgricultural Development Bank Limited: Unaudited Financial Results (Quarterly)sanjiv sahNo ratings yet

- Audited Financials Dec 2022Document1 pageAudited Financials Dec 2022EdwinNo ratings yet

- Unaudited Financial Results (Quarterly)Document1 pageUnaudited Financial Results (Quarterly)Rubin PoudelNo ratings yet

- 804 20210830 142718Document2 pages804 20210830 142718Sarath KumarNo ratings yet

- Ia 3 ZZZZDocument4 pagesIa 3 ZZZZPRE GNNo ratings yet

- Sol. Man. Chapter 10 Investments in Debt Securities Ia Part 1a 2020 EditionDocument34 pagesSol. Man. Chapter 10 Investments in Debt Securities Ia Part 1a 2020 EditionMizza Moreno CantilaNo ratings yet

- 002 Lease-Accouting-2Document2 pages002 Lease-Accouting-2caparvez25No ratings yet

- 1 - 433 - 1 - Cash Flow Statement 2016 2017Document1 page1 - 433 - 1 - Cash Flow Statement 2016 2017Avnit kumarNo ratings yet

- Chapter 3 Bonds Payable Other ConceptsDocument20 pagesChapter 3 Bonds Payable Other ConceptsThalia Rhine AberteNo ratings yet

- Ashwin 2070Document2 pagesAshwin 2070nayanghimireNo ratings yet

- Agricultural Development Bank Limited: Unaudited Financial Results (Quarterly) ProvisionalDocument3 pagesAgricultural Development Bank Limited: Unaudited Financial Results (Quarterly) ProvisionalaNo ratings yet

- 313 314 Financing Cycle CORNEL-MannelleDocument3 pages313 314 Financing Cycle CORNEL-MannelleFaker MejiaNo ratings yet

- Jamuna Bank Limited: Report Name: Statement of Affairs ConsolidatedDocument5 pagesJamuna Bank Limited: Report Name: Statement of Affairs Consolidatedarman_277276271No ratings yet

- Tugas AKM 2 Proportional MetodeDocument3 pagesTugas AKM 2 Proportional MetodeSheny WulandariNo ratings yet

- Paquiz, Katrina Assignment On Bonds PayableDocument1 pagePaquiz, Katrina Assignment On Bonds PayableKatrina PaquizNo ratings yet

- ACCO 20053 Lecture Notes 6 - Notes ReceivableDocument7 pagesACCO 20053 Lecture Notes 6 - Notes ReceivableVincent Luigil AlceraNo ratings yet

- Jamuna Bank: Dailv Statement of AffairsDocument14 pagesJamuna Bank: Dailv Statement of AffairsArman Hossain WarsiNo ratings yet

- Prob.2 Classroom Discussion BP OCDocument4 pagesProb.2 Classroom Discussion BP OCWenjunNo ratings yet

- Rastriya Banijya Bank Limited Singhdurbar Plaza, Kathmandu Unaudited Financial Results (Quarterly) As at 1St Quarter of Fiscal Year 2008-09Document1 pageRastriya Banijya Bank Limited Singhdurbar Plaza, Kathmandu Unaudited Financial Results (Quarterly) As at 1St Quarter of Fiscal Year 2008-09gonenp1No ratings yet

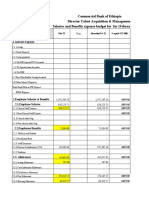

- Commercial Bank of Ethiopia Director Talent Acquisition & Management Salaries and Benefits Expense Budget For For (February 31,2023)Document19 pagesCommercial Bank of Ethiopia Director Talent Acquisition & Management Salaries and Benefits Expense Budget For For (February 31,2023)melat mideksaNo ratings yet

- Source: Bureau of The TreasuryDocument1 pageSource: Bureau of The TreasurypeejayNo ratings yet

- Intermediate Accounting 2Document4 pagesIntermediate Accounting 2MARRIETTE JOY ABADNo ratings yet

- Financial+Statements Ceres+Gardening+CompanyDocument13 pagesFinancial+Statements Ceres+Gardening+Companysiri pallaviNo ratings yet

- Problem 11-7 Given:: Date Payment 10% Interest Principal Present ValueDocument2 pagesProblem 11-7 Given:: Date Payment 10% Interest Principal Present ValueDominic RomeroNo ratings yet

- Chapter 3 Problem 6 LenzierDocument25 pagesChapter 3 Problem 6 LenzierJohn Lenzier TurtorNo ratings yet

- 9TH Bonds Payable Part IIDocument8 pages9TH Bonds Payable Part IIAnthony DyNo ratings yet

- Chapter 3 Problem 6 LenzierDocument25 pagesChapter 3 Problem 6 LenzierJohn Lenzier TurtorNo ratings yet

- UBL Annual Report 2018-79Document1 pageUBL Annual Report 2018-79IFRS LabNo ratings yet

- PT. Great River International TBK.: Summary of Financial StatementDocument1 pagePT. Great River International TBK.: Summary of Financial StatementroxasNo ratings yet

- Loan ReceivableDocument10 pagesLoan ReceivableClyde SaladagaNo ratings yet

- Receipts and Payments AccountDocument2 pagesReceipts and Payments AccountUmapathi MNo ratings yet

- Balance Sheet Bien HechoDocument21 pagesBalance Sheet Bien HechoRicardo PuyolNo ratings yet

- Bab VII - Soal2 Dan Solusi No. 7.07 N 7.08Document8 pagesBab VII - Soal2 Dan Solusi No. 7.07 N 7.08Adilla KhulaidahNo ratings yet

- FINACC3 Bonds Payable Practice Problem 3Document6 pagesFINACC3 Bonds Payable Practice Problem 3Khevin AlvaradoNo ratings yet

- Receivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesDocument3 pagesReceivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesGlance BautistaNo ratings yet

- Acc 106/dec 2019/quiz 2Document2 pagesAcc 106/dec 2019/quiz 2NURAIN HANIS BINTI ARIFFNo ratings yet

- The Bank of Punjab: Interim Condensed Balance Sheet As at September 30, 2008Document13 pagesThe Bank of Punjab: Interim Condensed Balance Sheet As at September 30, 2008Javed MuhammadNo ratings yet

- Pertemuan 1 - Shareholder EquityDocument11 pagesPertemuan 1 - Shareholder EquityIvonie NursalimNo ratings yet

- Problem 6: For Classroom Discussion: Requirement (A)Document6 pagesProblem 6: For Classroom Discussion: Requirement (A)Nikky Bless LeonarNo ratings yet

- Bhaivav Laxmi Ma Galla Bhandar7677Document14 pagesBhaivav Laxmi Ma Galla Bhandar7677Ravi KarnaNo ratings yet

- Bashyal Emporium7677Document6 pagesBashyal Emporium7677Ravi KarnaNo ratings yet

- Allowance For ImpairmentDocument1 pageAllowance For ImpairmentMae MarinoNo ratings yet

- Bonds Payable Issued at A PremiumDocument6 pagesBonds Payable Issued at A PremiumCris Ann Marie ESPAnOLANo ratings yet

- Report Saldo Update 01.11.23Document1 pageReport Saldo Update 01.11.23zaid.elfauzyNo ratings yet

- 21 Problems - and - Answers - Reclassification - of - Financial - AssetDocument30 pages21 Problems - and - Answers - Reclassification - of - Financial - AssetSheila Grace BajaNo ratings yet

- NotesDocument1 pageNotesAyesha AminNo ratings yet

- Chapter 14 - Homework AnswerDocument10 pagesChapter 14 - Homework AnswerSaja AlbarjesNo ratings yet

- Sol. Man. - Chapter 3 Bonds Payable Other ConceptsDocument21 pagesSol. Man. - Chapter 3 Bonds Payable Other ConceptsJasmine Nouvel Soriaga Cruz86% (7)

- Problem 10-8 (Banco)Document7 pagesProblem 10-8 (Banco)Roy Mitz Aggabao Bautista VNo ratings yet

- So Lieu Tai Chinh HAGL - Copy3.Document6 pagesSo Lieu Tai Chinh HAGL - Copy3.Dao HuynhNo ratings yet

- Bonds Payable-Between Interest Dates and SerialDocument4 pagesBonds Payable-Between Interest Dates and SerialJohn Williever GonzalezNo ratings yet

- Business ForecastingDocument6 pagesBusiness ForecastingRahat Mahmud ShoebNo ratings yet

- Bahan Ajar Hutang WeselDocument8 pagesBahan Ajar Hutang Weselcalsey azzahraNo ratings yet

- OutputDocument6 pagesOutputANNISANo ratings yet

- Bahan Ajar Dividen EpsDocument7 pagesBahan Ajar Dividen Epscalsey azzahraNo ratings yet

- Bahan Ajar Hutang WeselDocument8 pagesBahan Ajar Hutang Weselcalsey azzahraNo ratings yet

- Tugas 2.1 Lab AKMDocument1 pageTugas 2.1 Lab AKMcalsey azzahraNo ratings yet

- Flynn Design AgencyDocument4 pagesFlynn Design Agencycalsey azzahraNo ratings yet

- Latihan 1Document1 pageLatihan 1calsey azzahraNo ratings yet

- Calsey Azzahra 0302519005Document2 pagesCalsey Azzahra 0302519005calsey azzahraNo ratings yet