You might also like

- Group Assignment CompletedDocument68 pagesGroup Assignment CompletedHengyi LimNo ratings yet

- Linking Anthropology: History ClothingDocument5 pagesLinking Anthropology: History ClothingSajid Mohy Ul DinNo ratings yet

- IQ OQ PQ Validation Guideline DocumentsDocument2 pagesIQ OQ PQ Validation Guideline DocumentsBIMO KUKUHNo ratings yet

- Asm1 - HRM - Ha Thi VanDocument18 pagesAsm1 - HRM - Ha Thi VanVân HàNo ratings yet

- Moderating Effects of Founders' Role On The Influence of Internationalization On IPO Performance of Listed Companies in ThailandDocument18 pagesModerating Effects of Founders' Role On The Influence of Internationalization On IPO Performance of Listed Companies in ThailandJosé Luis Polo AndradeNo ratings yet

- 2019, Simon GaoDocument29 pages2019, Simon GaominnvalNo ratings yet

- Exploring Intellectual Capital Disclosure As A Mediator For The Relationship Between IPO Firm-Specific Characteristics and UnderpricingDocument18 pagesExploring Intellectual Capital Disclosure As A Mediator For The Relationship Between IPO Firm-Specific Characteristics and UnderpricingYanuar NugrohoNo ratings yet

- Determinants of Stock Prices in Dhaka Stock Exchange (DSE)Document10 pagesDeterminants of Stock Prices in Dhaka Stock Exchange (DSE)Allen AlfredNo ratings yet

- Association Between Firm CharacteristicsDocument33 pagesAssociation Between Firm Characteristicschavala allen kadamsNo ratings yet

- Assessing Market Attractiveness For MA Purposes - 31 - August 2012 - Final - For - Submission2Document26 pagesAssessing Market Attractiveness For MA Purposes - 31 - August 2012 - Final - For - Submission2Nabil KtifiNo ratings yet

- Macroeconomic Factors and Initial Public Offerings (Ipos) in MalaysiaDocument27 pagesMacroeconomic Factors and Initial Public Offerings (Ipos) in Malaysiasyeda uzmaNo ratings yet

- Grad Project Final SubmissionDocument25 pagesGrad Project Final SubmissionDina AlfawalNo ratings yet

- Economic Analysis of Ipo Underpricing in Stock MarDocument8 pagesEconomic Analysis of Ipo Underpricing in Stock MarRishita RajNo ratings yet

- Impacts of Earnings Quality and Debt Maturity on Investment Efficiency in VietnamDocument11 pagesImpacts of Earnings Quality and Debt Maturity on Investment Efficiency in VietnamMuhammad AzeemNo ratings yet

- The Relationship Between Information Transparency and The Informativeness of Accounting EarningsDocument10 pagesThe Relationship Between Information Transparency and The Informativeness of Accounting EarningsHuyen Trang PhamNo ratings yet

- Factors Affecting The Initial Return of Initial PuDocument13 pagesFactors Affecting The Initial Return of Initial PuReact EmotNo ratings yet

- Determinants of Share Prices at Karachi Stock Exchange: March 2019Document11 pagesDeterminants of Share Prices at Karachi Stock Exchange: March 2019anon_294717796No ratings yet

- An Empirical Examination of IPO Underpricing Between High-Technology and Non-High-Technology Firms in TaiwanDocument32 pagesAn Empirical Examination of IPO Underpricing Between High-Technology and Non-High-Technology Firms in TaiwanAhmadi AliNo ratings yet

- The Factors That Affect Shares' ReturnDocument13 pagesThe Factors That Affect Shares' ReturnCahMbelingNo ratings yet

- Effect of R D Investment On Performance of BankingDocument6 pagesEffect of R D Investment On Performance of BankingSh. Khurram AbidNo ratings yet

- Review of Accounting, Finance and GovernanceDocument17 pagesReview of Accounting, Finance and GovernanceImi MaximNo ratings yet

- Purpose: What Are They Researching, 2-What Is The Core and Embedded Questions They Are Trying To Answer, 3-What Are The Hypotheses They Are Trying To Test or Prove and 4-WhyDocument7 pagesPurpose: What Are They Researching, 2-What Is The Core and Embedded Questions They Are Trying To Answer, 3-What Are The Hypotheses They Are Trying To Test or Prove and 4-Whyazade azamiNo ratings yet

- Financial CrisisDocument9 pagesFinancial CrisisAnimeshNo ratings yet

- The Rise and Fall of Multinational Enterprises in Vietnam: Survival Analysis Using Census Data During 2000-2011Document32 pagesThe Rise and Fall of Multinational Enterprises in Vietnam: Survival Analysis Using Census Data During 2000-2011Naufal Taufiq AmmarNo ratings yet

- Cost of Capital - The Effect To The Firm Value and Profitability Empirical Evidences in Case of Personal Goods (Textile) Sector of KSE 100 IndexDocument7 pagesCost of Capital - The Effect To The Firm Value and Profitability Empirical Evidences in Case of Personal Goods (Textile) Sector of KSE 100 IndexKanganFatimaNo ratings yet

- Firm characteristics impact on voluntary disclosure in EgyptDocument11 pagesFirm characteristics impact on voluntary disclosure in Egyptmuhridho alaminNo ratings yet

- Idris, Ekundayo, Yunusa - Firm Attributes and Share Price FluctuationDocument16 pagesIdris, Ekundayo, Yunusa - Firm Attributes and Share Price FluctuationDavidNo ratings yet

- New Evidence On The Determinants of Foreign Direct Investments in Emerging Markets A Panel Data ApproachDocument8 pagesNew Evidence On The Determinants of Foreign Direct Investments in Emerging Markets A Panel Data ApproachEditor IJTSRDNo ratings yet

- Factors Influencing Stock Return in Coal Mining Sub-Sector Registered in Indonesia Stock Exchange in Period of 2011 To 2015Document8 pagesFactors Influencing Stock Return in Coal Mining Sub-Sector Registered in Indonesia Stock Exchange in Period of 2011 To 2015Anonymous izrFWiQNo ratings yet

- Factors Affecting Firm Competitiveness: Evidence From An Emerging MarketDocument10 pagesFactors Affecting Firm Competitiveness: Evidence From An Emerging MarketAnirudh H munjamaniNo ratings yet

- SSRN Id1000851Document44 pagesSSRN Id1000851SyedMuzammilAliNo ratings yet

- The Impact of Effective Investor Relations On Market Value Vineet AgarwalDocument24 pagesThe Impact of Effective Investor Relations On Market Value Vineet AgarwalAbhishek GuptaNo ratings yet

- The Impact of Stringent Insider Trading Laws and Institutional Quality On CostDocument11 pagesThe Impact of Stringent Insider Trading Laws and Institutional Quality On CostJuan Diego Veintimilla PanduroNo ratings yet

- Accounting Disclosures, Accounting Quality and Conditional and Unconditional ConservatismDocument39 pagesAccounting Disclosures, Accounting Quality and Conditional and Unconditional ConservatismNaglikar NagarajNo ratings yet

- Paper 2 - WirawanDocument12 pagesPaper 2 - WirawanJara TakuzawaNo ratings yet

- 10 1007@BF02885725Document9 pages10 1007@BF02885725gogayin869No ratings yet

- Final Literature ReviewDocument21 pagesFinal Literature ReviewAhsan IqbalNo ratings yet

- Market and Transaction Multiples' Accuracy in The European Equity MarketDocument8 pagesMarket and Transaction Multiples' Accuracy in The European Equity MarketShivam NagpalNo ratings yet

- Base PaperDocument17 pagesBase PaperMahwish AyubNo ratings yet

- Earning Response Coefficients and The Financial Risks of China Commercial BanksDocument11 pagesEarning Response Coefficients and The Financial Risks of China Commercial BanksShelly ImoNo ratings yet

- Article No5 Survival of The Fittest Post SEBI Era Final ShuklaDocument28 pagesArticle No5 Survival of The Fittest Post SEBI Era Final ShuklaKurapati VenkatkrishnaNo ratings yet

- Does Disclosure Regulation Reduce IPO UnderpricingDocument65 pagesDoes Disclosure Regulation Reduce IPO UnderpricingchethansoNo ratings yet

- The Effect of Bonds Rating, Profitability, Leverage, and Firm Size On Yield To Maturity Corporate BondsDocument10 pagesThe Effect of Bonds Rating, Profitability, Leverage, and Firm Size On Yield To Maturity Corporate BondsAnonymous izrFWiQNo ratings yet

- Causal Relation Between Stock Market Performance and Firm Investment in China: Mediating Role of Information AsymmetryDocument13 pagesCausal Relation Between Stock Market Performance and Firm Investment in China: Mediating Role of Information AsymmetrylaluaNo ratings yet

- FDI and Domestic FirmsDocument6 pagesFDI and Domestic FirmstallalbasahelNo ratings yet

- Corporate Governance and IPO Underpricing: Evidence From The Italian MarketDocument39 pagesCorporate Governance and IPO Underpricing: Evidence From The Italian MarketminnvalNo ratings yet

- Analysis of Internal and External FactorDocument10 pagesAnalysis of Internal and External FactorPhạm Thành ĐạtNo ratings yet

- Stock Market Liquidity and FirDocument11 pagesStock Market Liquidity and FirverenNo ratings yet

- (15-19) A Study of Merger and Acquisition of Selected Telecom Companies Outside IndiaDocument5 pages(15-19) A Study of Merger and Acquisition of Selected Telecom Companies Outside IndiaFatima AliNo ratings yet

- The Use of Voluntary Disclosure in Determining The Quality of Financial Statements: Evidence From The Nigeria Listed CompaniesDocument18 pagesThe Use of Voluntary Disclosure in Determining The Quality of Financial Statements: Evidence From The Nigeria Listed CompaniesReginaNo ratings yet

- The Mediating Role of Debt and Dividend Policy On The Effect Profitability Toward Stock PriceDocument10 pagesThe Mediating Role of Debt and Dividend Policy On The Effect Profitability Toward Stock PriceAAMINA ZAFARNo ratings yet

- Earnings and Cash Flow Performances Surrounding IpoDocument20 pagesEarnings and Cash Flow Performances Surrounding IpoRizki AmeliaNo ratings yet

- Research Work Halimat-OriginalDocument83 pagesResearch Work Halimat-Originalibrodan681No ratings yet

- EPU ICC Innovation FMA 2016Document60 pagesEPU ICC Innovation FMA 2016tanviNo ratings yet

- Science - 5 Corporate Aggregate Disclosure Practices in JordanDocument21 pagesScience - 5 Corporate Aggregate Disclosure Practices in JordanJullyaa CyNo ratings yet

- Sumber Skripsi - Analysis of Financial Distress Cross Counries Using MacroeconomicDocument12 pagesSumber Skripsi - Analysis of Financial Distress Cross Counries Using MacroeconomicAlvira FajriNo ratings yet

- Ding 2014Document8 pagesDing 2014Phuong Quyen PhamNo ratings yet

- Factors Affecting Price To Earnings Ratio (P/E) : Evidence From The Emerging MarketDocument11 pagesFactors Affecting Price To Earnings Ratio (P/E) : Evidence From The Emerging MarketWajiha TahaNo ratings yet

- Corporate Sustainability Disclosure and Market Valuation in A Middle Eastern Nation Evidence From Listed Firms On The Tehran Stock Exchange SensitiveDocument25 pagesCorporate Sustainability Disclosure and Market Valuation in A Middle Eastern Nation Evidence From Listed Firms On The Tehran Stock Exchange SensitiveXue Meng LuNo ratings yet

- Assidi, Soufiene (2020)Document12 pagesAssidi, Soufiene (2020)Bony BonyNo ratings yet

- The Nexus of Intellectual CapiDocument21 pagesThe Nexus of Intellectual CapiEkta MehtaNo ratings yet

- Chapter OneDocument6 pagesChapter OneHenry BitrusNo ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- Submission Date: 10-Mar-2021 07:58AM (UTC-0800) Submission ID: 1529370323 File Name: Essay - Docx (29.22K) Word Count: 1371 Character Count: 8583Document7 pagesSubmission Date: 10-Mar-2021 07:58AM (UTC-0800) Submission ID: 1529370323 File Name: Essay - Docx (29.22K) Word Count: 1371 Character Count: 8583Sajid Mohy Ul DinNo ratings yet

- Recent Advances in Liquid Organic Hydrogen Carriers: An Alcohol-Based Hydrogen EconomyDocument15 pagesRecent Advances in Liquid Organic Hydrogen Carriers: An Alcohol-Based Hydrogen EconomySajid Mohy Ul Din100% (1)

- ChartDocument1 pageChartSajid Mohy Ul DinNo ratings yet

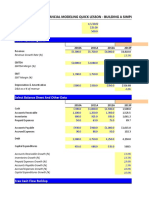

- Wall Street Prep - Financial Modeling Quick Lesson - Building A Simple Discounted Cash Flow ModelDocument6 pagesWall Street Prep - Financial Modeling Quick Lesson - Building A Simple Discounted Cash Flow ModelSajid Mohy Ul DinNo ratings yet

- Intrinsic and Extrinsic Motivation For University Staff Satisfaction: Confirmatory Composite Analysis and Confirmatory Factor AnalysisDocument27 pagesIntrinsic and Extrinsic Motivation For University Staff Satisfaction: Confirmatory Composite Analysis and Confirmatory Factor AnalysisSajid Mohy Ul DinNo ratings yet

- Surroca PDFDocument28 pagesSurroca PDFGuillem CasolivaNo ratings yet

- Insurance Activity and Economic Performance: Fresh Evidence From Asymmetric Panel Causality TestsDocument20 pagesInsurance Activity and Economic Performance: Fresh Evidence From Asymmetric Panel Causality TestsSajid Mohy Ul DinNo ratings yet

- Wall Street Prep - Financial Modeling Quick Lesson - Building A Simple Discounted Cash Flow ModelDocument6 pagesWall Street Prep - Financial Modeling Quick Lesson - Building A Simple Discounted Cash Flow ModelSajid Mohy Ul DinNo ratings yet

- The Impact of Corporate Social Responsibility On Firms' Financial Performance in South AfricaDocument23 pagesThe Impact of Corporate Social Responsibility On Firms' Financial Performance in South AfricaSajid Mohy Ul DinNo ratings yet

- Student Teacher Challenges Using The Cognitive Load Theory As An Explanatory Lens PDFDocument16 pagesStudent Teacher Challenges Using The Cognitive Load Theory As An Explanatory Lens PDFSajid Mohy Ul DinNo ratings yet

- SHWMDocument24 pagesSHWMVineet RathoreNo ratings yet

- An Inter Disciplinary Review of The Literature On Mental Illness Disclosure in The Workplace Implications For Human Resource ManagementDocument38 pagesAn Inter Disciplinary Review of The Literature On Mental Illness Disclosure in The Workplace Implications For Human Resource ManagementSajid Mohy Ul DinNo ratings yet

- Colloids and Surfaces A: Physicochemical and Engineering AspectsDocument10 pagesColloids and Surfaces A: Physicochemical and Engineering AspectsSajid Mohy Ul DinNo ratings yet

- In The University of Chakwal: Form of Application For The Use of Candidates For AppointmentDocument6 pagesIn The University of Chakwal: Form of Application For The Use of Candidates For AppointmentSajid Mohy Ul DinNo ratings yet

- A Theoretical Basis For Innovation, Institutions and Insurance Penetration NexusDocument13 pagesA Theoretical Basis For Innovation, Institutions and Insurance Penetration NexusSajid Mohy Ul DinNo ratings yet

- File000001 999062024Document1 pageFile000001 999062024Sajid Mohy Ul DinNo ratings yet

- Mobile Banking A Potential CADocument32 pagesMobile Banking A Potential CASajid Mohy Ul DinNo ratings yet

- Insurance Growth Nexus A Comparative Analysis With Multiple Insurance Proxies PDFDocument20 pagesInsurance Growth Nexus A Comparative Analysis With Multiple Insurance Proxies PDFSajid Mohy Ul DinNo ratings yet

- Can 2017Document29 pagesCan 2017Sajid Mohy Ul DinNo ratings yet

- U.S. Ssecurity Ppolicy Iin Ssouth Aasia Since 9/11 - Cchallenges Aand Implications Ffor Tthe FfutureDocument16 pagesU.S. Ssecurity Ppolicy Iin Ssouth Aasia Since 9/11 - Cchallenges Aand Implications Ffor Tthe FfutureSajid Mohy Ul DinNo ratings yet

- Marceau 2009Document36 pagesMarceau 2009Sajid Mohy Ul DinNo ratings yet

- And 1992Document14 pagesAnd 1992Sajid Mohy Ul DinNo ratings yet

- Jacob 2008Document37 pagesJacob 2008Sajid Mohy Ul DinNo ratings yet

- (Doi 10.1007/978-981!10!8147-7 - 4) Tan, Lee-Ming Lau Poh Hock, Evan Tang, Chor Foon - Finance & Economics Readings - Management of Mobile Financial Services-Review and Way ForwardDocument19 pages(Doi 10.1007/978-981!10!8147-7 - 4) Tan, Lee-Ming Lau Poh Hock, Evan Tang, Chor Foon - Finance & Economics Readings - Management of Mobile Financial Services-Review and Way ForwardSajid Mohy Ul DinNo ratings yet

- Frequency Changes in AC Systems Connected To DC Grids: Impact of AC vs. DC Side EventsDocument5 pagesFrequency Changes in AC Systems Connected To DC Grids: Impact of AC vs. DC Side EventsSajid Mohy Ul DinNo ratings yet

- Study On Technologies For Financial Inclusion in BRICSDocument17 pagesStudy On Technologies For Financial Inclusion in BRICSSajid Mohy Ul DinNo ratings yet

- Ijse 05 2017 0194Document23 pagesIjse 05 2017 0194Sajid Mohy Ul DinNo ratings yet

- Financial Inclusion HarnessinDocument9 pagesFinancial Inclusion HarnessinSajid Mohy Ul DinNo ratings yet

- Introduction To Business Analytics: Alka Vaidya NibmDocument41 pagesIntroduction To Business Analytics: Alka Vaidya NibmPrabhat SinghNo ratings yet

- Chapter 9 Lecture - Student VersionDocument51 pagesChapter 9 Lecture - Student VersionIsaac SpoonNo ratings yet

- Shuja - Assignment 2 - Product DevelopmentDocument80 pagesShuja - Assignment 2 - Product DevelopmentShuja SafdarNo ratings yet

- Notice of Ruling Following July 18, 2012 Further Case Management ConferenceDocument6 pagesNotice of Ruling Following July 18, 2012 Further Case Management ConferenceTeamMichaelNo ratings yet

- Central Bank V CADocument31 pagesCentral Bank V CAlawNo ratings yet

- Binmaley School of FisheriesDocument5 pagesBinmaley School of FisheriesNathan SorianoNo ratings yet

- Marquez vs. Secretary of Labor, G.R. No. 80685 (March 16, 1989)Document1 pageMarquez vs. Secretary of Labor, G.R. No. 80685 (March 16, 1989)Jolynne Anne GaticaNo ratings yet

- JETNET Iq Pulse - April 8 2021Document12 pagesJETNET Iq Pulse - April 8 2021Raja Churchill DassNo ratings yet

- Deed of Sale Real PropertyDocument2 pagesDeed of Sale Real PropertyAndrew M. AcederaNo ratings yet

- FPT ShopDocument25 pagesFPT ShopNhư MaiNo ratings yet

- Congratulations!: Your In-Principle Approval LetterDocument2 pagesCongratulations!: Your In-Principle Approval LetterAquib ShaikhNo ratings yet

- JP Morgan Industrials ConferenceDocument19 pagesJP Morgan Industrials ConferenceJames BrianNo ratings yet

- Multiple Nuclei TheoryDocument16 pagesMultiple Nuclei TheoryAura Puteri PelangiNo ratings yet

- 18bba033 OAPDocument49 pages18bba033 OAPBhoomi MeghwaniNo ratings yet

- Aon UK Stewardship CodeDocument143 pagesAon UK Stewardship CodevladshevtsovNo ratings yet

- Introduction To Enterprise SystemsDocument51 pagesIntroduction To Enterprise Systemsvarsha bansodeNo ratings yet

- Account Statement From 20 Apr 2022 To 4 May 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 20 Apr 2022 To 4 May 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRajkumar GopalanNo ratings yet

- RWJ Chapter 1 Introduction To Corporate FinanceDocument21 pagesRWJ Chapter 1 Introduction To Corporate FinanceAshekin Mahadi100% (1)

- Local Tax Double Taxation CaseDocument1 pageLocal Tax Double Taxation CaseEmmanuel YrreverreNo ratings yet

- Fire Insurance Claim - HomeworkDocument18 pagesFire Insurance Claim - Homeworknikhilcoke7No ratings yet

- Valuing Using DCF, Not Getting Misleaded by PE.-rohit ChouhanDocument4 pagesValuing Using DCF, Not Getting Misleaded by PE.-rohit ChouhanRenju ReghuNo ratings yet

- HR Data Analysis Assessment QuestionsDocument2 pagesHR Data Analysis Assessment QuestionsKIng KumarNo ratings yet

- Sanction LetterDocument2 pagesSanction LetterVS NaiduNo ratings yet

- Proforma Invoice: Ser. No. HS Code Detail Description of Machineries Model Q'Ty Unit Price (USD$) Total Amount (USD$)Document3 pagesProforma Invoice: Ser. No. HS Code Detail Description of Machineries Model Q'Ty Unit Price (USD$) Total Amount (USD$)OLIYADNo ratings yet

- Detroit HR PPT SatDocument21 pagesDetroit HR PPT Sat006 CyrusNo ratings yet

- Wisdom Wings Of: Summer Placement Brochure 2019-21Document44 pagesWisdom Wings Of: Summer Placement Brochure 2019-21Shivansh SinghNo ratings yet

- Axis CTF FillableDocument1 pageAxis CTF FillablemayankNo ratings yet

- Franchise Accounting - DoneDocument3 pagesFranchise Accounting - DoneJymldy EnclnNo ratings yet