You might also like

- Calendula EbookDocument12 pagesCalendula EbookCeciliaNo ratings yet

- BLADED - Theory Manual PDFDocument134 pagesBLADED - Theory Manual PDFdavidlokito100% (2)

- How To Start A Patio Installation Business: A Complete Patio & Concrete Installation Business PlanFrom EverandHow To Start A Patio Installation Business: A Complete Patio & Concrete Installation Business PlanRating: 3 out of 5 stars3/5 (1)

- Administration and Supervisory Uses of Test and Measurement - Coronado, Juliet N.Document23 pagesAdministration and Supervisory Uses of Test and Measurement - Coronado, Juliet N.Juliet N. Coronado89% (9)

- BW Query GuidelinesDocument10 pagesBW Query GuidelinesyshriniNo ratings yet

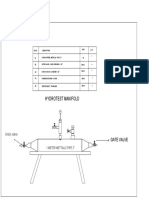

- Hydrotest manifold components listDocument1 pageHydrotest manifold components listMubeen NavazNo ratings yet

- 41-How To Calculate Air Temp in Unconditioned SpacesDocument3 pages41-How To Calculate Air Temp in Unconditioned Spacesalmig200No ratings yet

- Final TFC Round 1 and 2Document8 pagesFinal TFC Round 1 and 2AMRUT PATELNo ratings yet

- Samples For Loanshyd-1Document3 pagesSamples For Loanshyd-1dpkraja100% (1)

- 11 112020 CupidDocument13 pages11 112020 Cupidravi.youNo ratings yet

- Tata Elxsi FY20 Q4 Earnings Conference Call Summary - CEO Discusses Financial Performance and Impact of COVID-19Document17 pagesTata Elxsi FY20 Q4 Earnings Conference Call Summary - CEO Discusses Financial Performance and Impact of COVID-19Ashutosh GuptaNo ratings yet

- q3 Fy23 Earnings Call TranscriptDocument21 pagesq3 Fy23 Earnings Call TranscriptSohail AlamNo ratings yet

- Earning's Call - MoldtekDocument18 pagesEarning's Call - MoldtekArijit MukherjeeNo ratings yet

- Valiant Q3FY24 15 02 2024 12 00HrsDocument11 pagesValiant Q3FY24 15 02 2024 12 00Hrsmannkumarsingh6No ratings yet

- GHCL Limited - : 1 P - (FaxDocument30 pagesGHCL Limited - : 1 P - (FaxShyam SunderNo ratings yet

- Apxotex Concall Q2FY23Document23 pagesApxotex Concall Q2FY23Vivek RamNo ratings yet

- Transcript Schaeffler India Limited-Earnings Conference Call-19Apr-2023Document19 pagesTranscript Schaeffler India Limited-Earnings Conference Call-19Apr-2023JBNo ratings yet

- "Alkem Laboratories Limited Q3 FY2020 Earnings Conference Call" February 07, 2020Document20 pages"Alkem Laboratories Limited Q3 FY2020 Earnings Conference Call" February 07, 2020GurjeevNo ratings yet

- SFM Script for Balaji Amines Q4 Earnings CallDocument3 pagesSFM Script for Balaji Amines Q4 Earnings CallANAGHA B N 2127034No ratings yet

- Clt32tab199cat1323 20211119193457Document13 pagesClt32tab199cat1323 20211119193457Sunil Sandeep & Co.No ratings yet

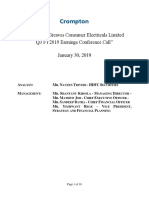

- "Crompton Greaves Consumer Electricals Limited Q2 FY2019 Earnings Conference Call" October 26, 2018Document18 pages"Crompton Greaves Consumer Electricals Limited Q2 FY2019 Earnings Conference Call" October 26, 2018NatNo ratings yet

- Q1FY21Document18 pagesQ1FY21Err DatabaseNo ratings yet

- Concall Feb 22Document23 pagesConcall Feb 22dhrivsitlani29No ratings yet

- Cosmo Films Q4FY20 - Conference - Call - TranscriptDocument14 pagesCosmo Films Q4FY20 - Conference - Call - TranscriptSam vermNo ratings yet

- Y 2011 Earnings Call - Jindal Saw Dt-13 May'11: OperatorDocument33 pagesY 2011 Earnings Call - Jindal Saw Dt-13 May'11: OperatorSandeep Aanand ShawNo ratings yet

- Conference Call Transcript (Company Update)Document21 pagesConference Call Transcript (Company Update)Shyam SunderNo ratings yet

- Sagar Cements LimitedDocument16 pagesSagar Cements Limitedmealokranjan9937No ratings yet

- GIL Q3 2011 TranscriptDocument15 pagesGIL Q3 2011 TranscriptJakeNo ratings yet

- SONA BLW Precision Forgings Ltd. (Sona Comstar) : Q1 FY22 Earnings Conference Call TranscriptDocument24 pagesSONA BLW Precision Forgings Ltd. (Sona Comstar) : Q1 FY22 Earnings Conference Call TranscriptVishal PrasadNo ratings yet

- Transcript of Conference Call (Company Update)Document15 pagesTranscript of Conference Call (Company Update)Shyam SunderNo ratings yet

- Industrial Gears, Power TransmissionDocument7 pagesIndustrial Gears, Power TransmissionSreenadhVNo ratings yet

- Transcript Earning Call 08-09Q2Document32 pagesTranscript Earning Call 08-09Q2shwetaforeNo ratings yet

- "GTPL Hathway Limited Annual FY 2019 & Q4 FY2019 Results Conference Call" April 16, 2019Document17 pages"GTPL Hathway Limited Annual FY 2019 & Q4 FY2019 Results Conference Call" April 16, 2019Sun TanNo ratings yet

- 762a3e60-b605-4fab-bb7d-b312425106dfDocument16 pages762a3e60-b605-4fab-bb7d-b312425106dfArjun BiswasNo ratings yet

- Racl Gear TechDocument10 pagesRacl Gear Techravi.youNo ratings yet

- Mahindra & Mahindra Limited Q3 FY-22 Earnings Conference CallDocument14 pagesMahindra & Mahindra Limited Q3 FY-22 Earnings Conference CallBharathNo ratings yet

- Sunil Kumar JainDocument15 pagesSunil Kumar Jainsahil.goelNo ratings yet

- "Crompton Greaves Consumer Electricals Limited Q3 FY2019 Earnings Conference Call" January 30, 2019Document18 pages"Crompton Greaves Consumer Electricals Limited Q3 FY2019 Earnings Conference Call" January 30, 2019NatNo ratings yet

- Transcript Earnings CallDocument16 pagesTranscript Earnings Callgaurav gargNo ratings yet

- Aarti IndustriesDocument33 pagesAarti IndustriesVijay CNo ratings yet

- CG Consumer Electricals Q1FY18Document18 pagesCG Consumer Electricals Q1FY18Nikhil JohriNo ratings yet

- Dixon Technologies (India) LTD.: Sub: Transcript of The Q4 FY 2022 Earnings Conference Call Held On May 30, 2022Document15 pagesDixon Technologies (India) LTD.: Sub: Transcript of The Q4 FY 2022 Earnings Conference Call Held On May 30, 2022pratheekNo ratings yet

- Chairman's SpeechDocument6 pagesChairman's SpeechskumarcwacaNo ratings yet

- E.Transcript (Q3-FY 21)Document25 pagesE.Transcript (Q3-FY 21)beza manojNo ratings yet

- (English (Auto-Generated) ) JTL Infra LTD Q3 FY24 Earnings Concall (DownSub - Com)Document55 pages(English (Auto-Generated) ) JTL Infra LTD Q3 FY24 Earnings Concall (DownSub - Com)himansu routNo ratings yet

- 20161111_SRF_EarningsCall_SRF_IN_2017-01-03T15_13_23_EARNINGDocument15 pages20161111_SRF_EarningsCall_SRF_IN_2017-01-03T15_13_23_EARNINGgeniusmeetNo ratings yet

- Transcript Regarding Investors' Conference Call (Company Update)Document25 pagesTranscript Regarding Investors' Conference Call (Company Update)Shyam SunderNo ratings yet

- Annual Report - Hyderabad Industries - 2009-2010Document24 pagesAnnual Report - Hyderabad Industries - 2009-2010siruslara6491No ratings yet

- "Sheela Foam Limited Q3 FY17 Results Conference Call": February 03, 2017Document18 pages"Sheela Foam Limited Q3 FY17 Results Conference Call": February 03, 2017bhishmaNo ratings yet

- Pricol Q4 FY21 earnings call transcriptDocument22 pagesPricol Q4 FY21 earnings call transcriptVishal PrasadNo ratings yet

- Page Earning Call Feb 2020 PDFDocument18 pagesPage Earning Call Feb 2020 PDFRakesh JhunjhunwallaNo ratings yet

- Sunteck Transcript Q1 FY 2023Document10 pagesSunteck Transcript Q1 FY 2023KIPL BLACKSWANNo ratings yet

- KEI Industries Q4 FY2018 Earnings Call SummaryDocument17 pagesKEI Industries Q4 FY2018 Earnings Call SummarygauravinflamesNo ratings yet

- zmAiUi2KLRRfS8nxn3WaDocument17 pageszmAiUi2KLRRfS8nxn3WainvestfortestNo ratings yet

- Greaves Concall TranscriptDocument15 pagesGreaves Concall Transcriptnadekaramit9122No ratings yet

- "Sobha Limited Q3 FY2019 Earnings Conference Call" February 06, 2019Document20 pages"Sobha Limited Q3 FY2019 Earnings Conference Call" February 06, 2019ajitNo ratings yet

- Aarti IndustriesDocument15 pagesAarti IndustriesHimanshu GoyalNo ratings yet

- Concall Aug 22Document26 pagesConcall Aug 22dhrivsitlani29No ratings yet

- Annual Report InsightsDocument36 pagesAnnual Report InsightsChaminda Devan MuthuhettiNo ratings yet

- Intimation Regarding Call TranscriptDocument18 pagesIntimation Regarding Call TranscriptMan Mohan KalitaNo ratings yet

- Clean Science Q3 Earnings Call Highlights Growth and New Product LaunchesDocument28 pagesClean Science Q3 Earnings Call Highlights Growth and New Product Launchesbeza manojNo ratings yet

- BSE Limited. Phiroze Jeejeebhoy Towers, Mumbai - 400 001Document20 pagesBSE Limited. Phiroze Jeejeebhoy Towers, Mumbai - 400 001ravi.youNo ratings yet

- FM Assignment: Amrutha Sajeevfm-1951MBA, BATCH-18Document8 pagesFM Assignment: Amrutha Sajeevfm-1951MBA, BATCH-18Sasidharan Sajeev ChathathuNo ratings yet

- Dalmia Bharat Limited Quarter and Year Ended Earnings 31st March 2019 Conference CallDocument17 pagesDalmia Bharat Limited Quarter and Year Ended Earnings 31st March 2019 Conference CallJagannath DNo ratings yet

- Bodal Chemicals LTD.: Sec/20-21/49 Date: 17-08-2020Document13 pagesBodal Chemicals LTD.: Sec/20-21/49 Date: 17-08-2020annanyaNo ratings yet

- Ashok Leyland Conference Call Transcript Q2 2013Document13 pagesAshok Leyland Conference Call Transcript Q2 2013ash147No ratings yet

- Jagran Prakashan Transcript Q4FY20Document23 pagesJagran Prakashan Transcript Q4FY20Sam vermNo ratings yet

- PartDetails 000030011+Document1 pagePartDetails 000030011+Mubeen NavazNo ratings yet

- Seydelmann High Eff Cutter Extra QuietDocument11 pagesSeydelmann High Eff Cutter Extra QuietMubeen NavazNo ratings yet

- Websites To Elevate Your Job SearchDocument9 pagesWebsites To Elevate Your Job SearchMubeen NavazNo ratings yet

- Acronyms 1704399993Document108 pagesAcronyms 1704399993Mubeen NavazNo ratings yet

- Company Overview: Norden Machinery ABDocument21 pagesCompany Overview: Norden Machinery ABMubeen NavazNo ratings yet

- Zodiac Authorized Sales & Service:: AngolaDocument44 pagesZodiac Authorized Sales & Service:: AngolaMubeen NavazNo ratings yet

- Beeah 740632828Document40 pagesBeeah 740632828Mubeen NavazNo ratings yet

- TD Ma Ose Centrifugal Separator 2012 06 en 171179Document4 pagesTD Ma Ose Centrifugal Separator 2012 06 en 171179Mubeen NavazNo ratings yet

- ASP Vulcan Seals FDA SealsDocument22 pagesASP Vulcan Seals FDA SealsMubeen NavazNo ratings yet

- TOMRA R1 and T9 With MultiPac AirDocument6 pagesTOMRA R1 and T9 With MultiPac AirMubeen NavazNo ratings yet

- Renewable Energy-DigitalDocument33 pagesRenewable Energy-DigitalMubeen NavazNo ratings yet

- TOMRA T9 With EasyPacDocument5 pagesTOMRA T9 With EasyPacMubeen NavazNo ratings yet

- Seminar Planner: Thursday 4 March 2021: 9.40am - 10.10am Opening KeynoteDocument8 pagesSeminar Planner: Thursday 4 March 2021: 9.40am - 10.10am Opening KeynoteMubeen NavazNo ratings yet

- Blue Yonder Inventory Optimization Solution SheetDocument2 pagesBlue Yonder Inventory Optimization Solution SheetMubeen Navaz0% (1)

- WMS Accelerator AutoScheduler Boosts Inventory, Capacity & OTIFDocument1 pageWMS Accelerator AutoScheduler Boosts Inventory, Capacity & OTIFMubeen NavazNo ratings yet

- Yakult ProfileDocument36 pagesYakult ProfileMubeen NavazNo ratings yet

- INTERNATIONAL INDIAN SCHOOL AL JUBAIL IISJ ProspectusDocument7 pagesINTERNATIONAL INDIAN SCHOOL AL JUBAIL IISJ ProspectusMubeen NavazNo ratings yet

- 92 SCOPE PRO Attendee VirtualEventBrochure 01262021Document16 pages92 SCOPE PRO Attendee VirtualEventBrochure 01262021Mubeen NavazNo ratings yet

- Yakult ProfileDocument36 pagesYakult ProfileMubeen NavazNo ratings yet

- Company Profile: Nutritional & Fortified Dry Food Powder ProductsDocument10 pagesCompany Profile: Nutritional & Fortified Dry Food Powder ProductsMubeen NavazNo ratings yet

- Morning Template 16x9Document5 pagesMorning Template 16x9arnatia09No ratings yet

- 10 October 2010 Calendar ClassicDocument1 page10 October 2010 Calendar ClassicammoderoNo ratings yet

- IISJ Admission Notification 2021-22Document1 pageIISJ Admission Notification 2021-22Mubeen NavazNo ratings yet

- Customer Facing TimeDocument11 pagesCustomer Facing TimeMubeen NavazNo ratings yet

- Poster Juz 1 - EDocument1 pagePoster Juz 1 - EMubeen NavazNo ratings yet

- Student Registration Portal GuideDocument2 pagesStudent Registration Portal GuideshakeelahmadjsrNo ratings yet

- An Introduction To Royal DSMDocument35 pagesAn Introduction To Royal DSMRafikul RahemanNo ratings yet

- BDA-811-en TITANIUM PUTTY (Ti) HARDENER - SDS10485 - ENDocument9 pagesBDA-811-en TITANIUM PUTTY (Ti) HARDENER - SDS10485 - ENMubeen NavazNo ratings yet

- Enjoy Worldwide!: Gelato From TraditionDocument14 pagesEnjoy Worldwide!: Gelato From TraditionMubeen NavazNo ratings yet

- 2.e-Learning Chapter 910Document23 pages2.e-Learning Chapter 910ethandanfordNo ratings yet

- Few Words About Digital Protection RelayDocument5 pagesFew Words About Digital Protection RelayVasudev AgrawalNo ratings yet

- Yatendra Kumar Sharma ResumeDocument3 pagesYatendra Kumar Sharma ResumeDheeraj SharmaNo ratings yet

- India: Soil Types, Problems & Conservation: Dr. SupriyaDocument25 pagesIndia: Soil Types, Problems & Conservation: Dr. SupriyaManas KaiNo ratings yet

- Grammar Notes-February2017 - by Aslinda RahmanDocument41 pagesGrammar Notes-February2017 - by Aslinda RahmanNadia Anuar100% (1)

- Chapter 2 Research and DesignDocument24 pagesChapter 2 Research and Designalvin salesNo ratings yet

- M HNDTL SCKT Imp BP RocDocument2 pagesM HNDTL SCKT Imp BP RocAhmed Abd El RahmanNo ratings yet

- BRTU-2000 Remote Terminal Unit for High Voltage NetworksDocument2 pagesBRTU-2000 Remote Terminal Unit for High Voltage NetworksLaurentiuNo ratings yet

- Water Booster Pump Calculations - Plumbing Engineering - Eng-TipsDocument3 pagesWater Booster Pump Calculations - Plumbing Engineering - Eng-TipsNeal JohnsonNo ratings yet

- Internship Report On Incepta PharmaceutiDocument31 pagesInternship Report On Incepta PharmaceutihhaiderNo ratings yet

- Bajaj Internship ReportDocument69 pagesBajaj Internship ReportCoordinator ABS100% (2)

- Cloud Computing For Industrial Automation Systems - A ComprehensiveDocument4 pagesCloud Computing For Industrial Automation Systems - A ComprehensiveJason FloydNo ratings yet

- NJMC Lca FinalDocument47 pagesNJMC Lca Finalr_gelpiNo ratings yet

- Kaseya Performance and Best Practices Guide: Authors: Jacques Eagle Date: Thursday, April 29, 2010Document34 pagesKaseya Performance and Best Practices Guide: Authors: Jacques Eagle Date: Thursday, April 29, 2010markdavidboydNo ratings yet

- 4 Types and Methods of Speech DeliveryDocument2 pages4 Types and Methods of Speech DeliveryKylie EralinoNo ratings yet

- Organic Vapour List PDFDocument1 pageOrganic Vapour List PDFDrGurkirpal Singh MarwahNo ratings yet

- Aptamers in HIV Research Diagnosis and TherapyDocument11 pagesAptamers in HIV Research Diagnosis and TherapymikiNo ratings yet

- Sublime Union: A Womans Sexual Odyssey Guided by Mary Magdalene (Book Two of The Magdalene Teachings) Download Free BookDocument4 pagesSublime Union: A Womans Sexual Odyssey Guided by Mary Magdalene (Book Two of The Magdalene Teachings) Download Free Bookflavia cascarinoNo ratings yet

- Infrastructure Finance Project Design and Appraisal: Professor Robert B.H. Hauswald Kogod School of Business, AUDocument2 pagesInfrastructure Finance Project Design and Appraisal: Professor Robert B.H. Hauswald Kogod School of Business, AUAida0% (1)

- Product Catalog Encoders en IM0038143Document788 pagesProduct Catalog Encoders en IM0038143Eric GarciaNo ratings yet

- Distillation Lab ReportDocument6 pagesDistillation Lab ReportSNo ratings yet

- Unit-3 22es14aDocument77 pagesUnit-3 22es14atejvimathNo ratings yet