You might also like

- How to Stop Corruption ?: A Study of the Effects and Solutions of Corruption on Economic Development of IndiaFrom EverandHow to Stop Corruption ?: A Study of the Effects and Solutions of Corruption on Economic Development of IndiaNo ratings yet

- Allison 2021Document43 pagesAllison 2021daniloNo ratings yet

- EIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptFrom EverandEIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptNo ratings yet

- De Andrés, P., Gimeno, R., & Mateos de Cabo, R. (2021) - The Gender Gap in Bank Credit Access. Journal of Corporate Finance, 71, 101782.Document18 pagesDe Andrés, P., Gimeno, R., & Mateos de Cabo, R. (2021) - The Gender Gap in Bank Credit Access. Journal of Corporate Finance, 71, 101782.Ruth Mateos de CaboNo ratings yet

- Uncovering the Dirty Truth: The Devastating Impact of Corruption on American Politics"From EverandUncovering the Dirty Truth: The Devastating Impact of Corruption on American Politics"No ratings yet

- Corruption in International Business: Types, Measures, Causes, ConsequencesDocument27 pagesCorruption in International Business: Types, Measures, Causes, ConsequenceslolNo ratings yet

- The Relationship Between Access To Finance and Job Growth With A Highlight On Credit ReportingDocument2 pagesThe Relationship Between Access To Finance and Job Growth With A Highlight On Credit ReportingClarence TongNo ratings yet

- Journal of Corporate Finance: Rajabrata Banerjee, Kartick Gupta, Chandrasekhar KrishnamurtiDocument29 pagesJournal of Corporate Finance: Rajabrata Banerjee, Kartick Gupta, Chandrasekhar Krishnamurtidimpi singhNo ratings yet

- Does Corruption Hinder or Boost Firm Investment? A Vietnamese PerspectiveDocument5 pagesDoes Corruption Hinder or Boost Firm Investment? A Vietnamese PerspectiveaijbmNo ratings yet

- Political & Economic Risk Consultancy SurveyDocument5 pagesPolitical & Economic Risk Consultancy SurveyHornbook RuleNo ratings yet

- Tugas Metpen Haniatun PDFDocument30 pagesTugas Metpen Haniatun PDFHaniatun HanieNo ratings yet

- Advances in Measuring Corruption in The Field: Sandra Sequeira London School of EconomicsDocument37 pagesAdvances in Measuring Corruption in The Field: Sandra Sequeira London School of EconomicsFlorin Marius PopaNo ratings yet

- Corruption in Civil Engineering: Lebanese American University School of EngineeringDocument19 pagesCorruption in Civil Engineering: Lebanese American University School of EngineeringahmadNo ratings yet

- Bhasin UnethicalCACultureatSatyam IJBSR July2016 PDFDocument26 pagesBhasin UnethicalCACultureatSatyam IJBSR July2016 PDFSeema ChaturvediNo ratings yet

- Corruption in Asia and Effects On Third World CountryDocument14 pagesCorruption in Asia and Effects On Third World Countrylunacy101No ratings yet

- Corruption's Impact on Income Inequality in BangladeshDocument6 pagesCorruption's Impact on Income Inequality in BangladeshIkramul HoqueNo ratings yet

- Bfi WP 2022-04Document77 pagesBfi WP 2022-04Caique MeloNo ratings yet

- Las Consecuencias No Deseadas de #MeToo Evidencia de Colaboraciones de InvestigaciónDocument84 pagesLas Consecuencias No Deseadas de #MeToo Evidencia de Colaboraciones de InvestigaciónJMNo ratings yet

- Informality, Corruption and Inequality: A LinkageDocument35 pagesInformality, Corruption and Inequality: A LinkageKoeinam GallagherNo ratings yet

- Financial Literacy and Fraud Detection, Kel 4Document17 pagesFinancial Literacy and Fraud Detection, Kel 4Angellina LamambaNo ratings yet

- Bribery Survey Report FinalDocument7 pagesBribery Survey Report FinalManish PrasadNo ratings yet

- 1 Running Head: Corruption Behaviors and Multinational OrganizationDocument8 pages1 Running Head: Corruption Behaviors and Multinational OrganizationJessyNo ratings yet

- J Worlddev 2014 10 008Document19 pagesJ Worlddev 2014 10 008abtraore083No ratings yet

- WP 232 UpdatedDocument92 pagesWP 232 Updatedspringfield12No ratings yet

- Best 3Document15 pagesBest 3Tahir DestaNo ratings yet

- Articulo en Ingles de EconomiaDocument24 pagesArticulo en Ingles de EconomiaBryanNo ratings yet

- Corruption in Indonesia: Does Grease Hypothesis HoldDocument9 pagesCorruption in Indonesia: Does Grease Hypothesis HoldLinaNo ratings yet

- Corruption and Income Inequality in BangladeshDocument23 pagesCorruption and Income Inequality in BangladeshIkramul HoqueNo ratings yet

- TERM PAPER ON Bribery ImpactDocument23 pagesTERM PAPER ON Bribery ImpactAbbas Ansari100% (1)

- 15) Corruption and Capital GrowthDocument13 pages15) Corruption and Capital GrowthChee MinNo ratings yet

- BHASIN DebacleofSatyam Wulfenia 2016Document40 pagesBHASIN DebacleofSatyam Wulfenia 2016P. S. Jhedu & AssociatesNo ratings yet

- 01 Ijmres 10032020Document9 pages01 Ijmres 10032020International Journal of Management Research and Emerging SciencesNo ratings yet

- Malaysia Case Study of FraudDocument13 pagesMalaysia Case Study of FraudSimeony SimeNo ratings yet

- 909-Dokumen Artikel Utama-3428-1-10-20221225Document14 pages909-Dokumen Artikel Utama-3428-1-10-20221225Adi SatriyaNo ratings yet

- Corporate and Accounting Fraud: Types, Causes and Fraudster's Business ProfileDocument10 pagesCorporate and Accounting Fraud: Types, Causes and Fraudster's Business Profilenoordin MukasaNo ratings yet

- Zhang 2016Document22 pagesZhang 2016MultazamMansyurAdduryNo ratings yet

- Journal of Contemporary Accounting & Economics: Chandrasekhar Krishnamurti, Syed Shams, Eswaran VelayuthamDocument21 pagesJournal of Contemporary Accounting & Economics: Chandrasekhar Krishnamurti, Syed Shams, Eswaran VelayuthamMario DavilaNo ratings yet

- India's Satyam accounting scandal case studyDocument40 pagesIndia's Satyam accounting scandal case studySultana ChowdhuryNo ratings yet

- The Effect of Social Norms on Bribe OffersDocument18 pagesThe Effect of Social Norms on Bribe OffersrodrigomoroNo ratings yet

- Creative Accounting Practices at Satyam Computers Limited: A Case Study of India's EnronDocument25 pagesCreative Accounting Practices at Satyam Computers Limited: A Case Study of India's EnronNurlinaNo ratings yet

- 135 Article Text 223 1 10 20201125 1Document18 pages135 Article Text 223 1 10 20201125 1anhctt10.gecNo ratings yet

- Psychology of CorruptionDocument4 pagesPsychology of CorruptionLiezel LopegaNo ratings yet

- Online FraudDocument24 pagesOnline FraudJay Ar100% (1)

- Version Conference PMMA 12517Document20 pagesVersion Conference PMMA 12517Aniket SahaNo ratings yet

- History of Corruption in the PhilippinesDocument5 pagesHistory of Corruption in the PhilippinesXenos Mariano Fitness VlogNo ratings yet

- Ejbss 1208 13 Corporateaccountingscandalatsatyam PDFDocument23 pagesEjbss 1208 13 Corporateaccountingscandalatsatyam PDFDebasish SahaNo ratings yet

- AUDRETSCHDocument22 pagesAUDRETSCHDiego Andrés Riaño PinzónNo ratings yet

- Arvin JainDocument51 pagesArvin Jainsaiful deniNo ratings yet

- Corruption, Gender and Credit Constraints - Evidence From South Asian - January 2019 PDFDocument14 pagesCorruption, Gender and Credit Constraints - Evidence From South Asian - January 2019 PDFanalysesNo ratings yet

- A Study On Impact Of11Document28 pagesA Study On Impact Of11bagyaNo ratings yet

- Employee Misallocation: Fraud Statement & InvestigationDocument7 pagesEmployee Misallocation: Fraud Statement & Investigationbelinda dagohoyNo ratings yet

- Is Commercialization of Microfinance Responsible For Over-Indebtedness? The Case of Andhra Pradesh CrisisDocument13 pagesIs Commercialization of Microfinance Responsible For Over-Indebtedness? The Case of Andhra Pradesh CrisisPratik PatilNo ratings yet

- Control InternDocument7 pagesControl InternJEAN PIERRE ALEXANDER PAICO GUEVARANo ratings yet

- Are Women Entrepreneurs Facing Bias in Funding DecisionsDocument13 pagesAre Women Entrepreneurs Facing Bias in Funding DecisionsFadli NoorNo ratings yet

- Corruption FoE Project.Document8 pagesCorruption FoE Project.Aryan RajNo ratings yet

- Barriers Faced by Female Entrepreneurs in the UKDocument12 pagesBarriers Faced by Female Entrepreneurs in the UKpreamNo ratings yet

- KPMG Bribery Survey Report NewDocument20 pagesKPMG Bribery Survey Report NewBalu SukumarNo ratings yet

- Chapter LL - RRLDocument11 pagesChapter LL - RRLJezel roldan0% (2)

- Research Paper On Corruption and Economic GrowthDocument7 pagesResearch Paper On Corruption and Economic GrowthzejasyvkgNo ratings yet

- U.S. Political Corruption and Loan PricingDocument31 pagesU.S. Political Corruption and Loan PricingAla'a AbuhommousNo ratings yet

- Some Incomplete Hypergeometric Functions and IncomDocument17 pagesSome Incomplete Hypergeometric Functions and IncomJosh GonzalesNo ratings yet

- The Impact of Sustainability Practices On Corporate Financial Performance Literature Trends and Future Research PotentialDocument25 pagesThe Impact of Sustainability Practices On Corporate Financial Performance Literature Trends and Future Research PotentialLondonNo ratings yet

- Fintech and Sustainability: A Mini-Review: SSRN Electronic Journal January 2019Document14 pagesFintech and Sustainability: A Mini-Review: SSRN Electronic Journal January 2019Josh GonzalesNo ratings yet

- The incomplete Srivastava's triple hypergeometric functions γHB and ΓHBDocument10 pagesThe incomplete Srivastava's triple hypergeometric functions γHB and ΓHBJosh GonzalesNo ratings yet

- Perturbed Markov Chains and Information NetworksDocument61 pagesPerturbed Markov Chains and Information NetworksJosh GonzalesNo ratings yet

- Exploration of Green Marketing: A Shift From Traditional Marketing To Green Marketing For Sustainable Environment AbstractDocument14 pagesExploration of Green Marketing: A Shift From Traditional Marketing To Green Marketing For Sustainable Environment AbstractJosh GonzalesNo ratings yet

- The Role of Financial Management in Promoting Sustainable Business Practices and DevelopmentDocument22 pagesThe Role of Financial Management in Promoting Sustainable Business Practices and DevelopmentJosh GonzalesNo ratings yet

- The Power of A Hand-Shake in Human-Robot Interactions: October 2018Document7 pagesThe Power of A Hand-Shake in Human-Robot Interactions: October 2018Josh GonzalesNo ratings yet

- Urgen PHD Thesis FinalDocument162 pagesUrgen PHD Thesis FinalJosh GonzalesNo ratings yet

- The Potential and Challenges of Time-Resolved SingDocument33 pagesThe Potential and Challenges of Time-Resolved SingJosh GonzalesNo ratings yet

- Towards Natural Handshakes For Social Robots HumanDocument14 pagesTowards Natural Handshakes For Social Robots HumanJosh GonzalesNo ratings yet

- Robot-To-Human Feedback and Automatic Object Grasping Using An RGB-D Camera-Projector SystemDocument21 pagesRobot-To-Human Feedback and Automatic Object Grasping Using An RGB-D Camera-Projector SystemJosh GonzalesNo ratings yet

- Finance Manager and The Finance Function in Business SustainabilityDocument9 pagesFinance Manager and The Finance Function in Business SustainabilityJosh GonzalesNo ratings yet

- Reasoning About and Harmonizing The Interaction BeDocument101 pagesReasoning About and Harmonizing The Interaction BeJosh GonzalesNo ratings yet

- LiuJH2018PrecamRes InpressDocument14 pagesLiuJH2018PrecamRes InpressJosh GonzalesNo ratings yet

- RGB-D-Based Object Recognition Using Multimodal CoDocument27 pagesRGB-D-Based Object Recognition Using Multimodal CoJosh GonzalesNo ratings yet

- Nonequilibrium Optical Control of Dynamical StatesDocument7 pagesNonequilibrium Optical Control of Dynamical StatesJosh GonzalesNo ratings yet

- On The Perceptual Advantages of Visual SuppressionDocument7 pagesOn The Perceptual Advantages of Visual SuppressionJosh GonzalesNo ratings yet

- Numerical Semigroups From Open IntervalsDocument8 pagesNumerical Semigroups From Open IntervalsJosh GonzalesNo ratings yet

- Reasoning About and Harmonizing The Interaction BeDocument101 pagesReasoning About and Harmonizing The Interaction BeJosh GonzalesNo ratings yet

- Penerapan Finite State Automata Pada Vending Machine Susu Kambing EtawaDocument6 pagesPenerapan Finite State Automata Pada Vending Machine Susu Kambing EtawaFadhlan DzilNo ratings yet

- WM WSM.14.23.ZazaDashnianipublicversionDocument118 pagesWM WSM.14.23.ZazaDashnianipublicversionJosh GonzalesNo ratings yet

- Gender Effects on Math Anxiety and AchievementDocument33 pagesGender Effects on Math Anxiety and AchievementJosh GonzalesNo ratings yet

- Subnanosecond Incubation Times For Electric-Field-Induced Metallization of A Correlated Electron OxideDocument7 pagesSubnanosecond Incubation Times For Electric-Field-Induced Metallization of A Correlated Electron OxideJosh GonzalesNo ratings yet

- Test Anxiety in Adolescent Students Different RespDocument8 pagesTest Anxiety in Adolescent Students Different RespJosh GonzalesNo ratings yet

- EQEC-2019-eb 7 4Document2 pagesEQEC-2019-eb 7 4Josh GonzalesNo ratings yet

- Van Mier Front Psy 2019Document14 pagesVan Mier Front Psy 2019Josh GonzalesNo ratings yet

- Gender, General Anxiety, Math Anxiety and Math Achievement in Early School-Age ChildrenDocument18 pagesGender, General Anxiety, Math Anxiety and Math Achievement in Early School-Age ChildrenJosh GonzalesNo ratings yet

- Students' beliefs about formative assessment in mathDocument16 pagesStudents' beliefs about formative assessment in mathJosh GonzalesNo ratings yet

- A Control-Value Theory Approach: Relationships Between Academic Self-Concept, Interest, and Test Anxiety in Elementary School ChildrenDocument21 pagesA Control-Value Theory Approach: Relationships Between Academic Self-Concept, Interest, and Test Anxiety in Elementary School ChildrenJosh GonzalesNo ratings yet

- Corporation Code Up To 45Document56 pagesCorporation Code Up To 45Jasmine Montero-GaribayNo ratings yet

- Land Bank Vs Ong, 636 SCRA 266Document12 pagesLand Bank Vs Ong, 636 SCRA 266kingNo ratings yet

- FINACC-Homework Exercise 2Document3 pagesFINACC-Homework Exercise 2Jomel BaptistaNo ratings yet

- A Study of Bank Operations and Loans Given by Nawanagar Co-Operative Bank Ltd''.Document70 pagesA Study of Bank Operations and Loans Given by Nawanagar Co-Operative Bank Ltd''.Umang Vora0% (1)

- Accounting What The Numbers Mean 9th Edition Marshall Solutions Manual Full Chapter PDFDocument60 pagesAccounting What The Numbers Mean 9th Edition Marshall Solutions Manual Full Chapter PDFclergypresumerb37al7100% (12)

- Chapter 4 Time Value of Money (Part1)Document41 pagesChapter 4 Time Value of Money (Part1)AbdNo ratings yet

- Barter SystemDocument27 pagesBarter SystemimadNo ratings yet

- Chapter 12 - Credit Agreements PDFDocument7 pagesChapter 12 - Credit Agreements PDFMacdonald PhashaNo ratings yet

- 2019 September IAI PSAK 72Document94 pages2019 September IAI PSAK 72analisa akuntansi100% (1)

- 2203 Week 5 TemplateDocument39 pages2203 Week 5 TemplateHORTENSENo ratings yet

- "What Is " ا: َب ِّ رلا " (THE RIBA) ?Document11 pages"What Is " ا: َب ِّ رلا " (THE RIBA) ?Zaki AlattarNo ratings yet

- Assessment of Causes, Effects and Solutions To Abandoned Building Projects in GhanaDocument13 pagesAssessment of Causes, Effects and Solutions To Abandoned Building Projects in GhanaEsaenwi ThankGodNo ratings yet

- Hoover Digest, 2024, No. 1, FallDocument208 pagesHoover Digest, 2024, No. 1, FallHoover Institution100% (1)

- Research Paper On GoldDocument7 pagesResearch Paper On GoldjayminashahNo ratings yet

- Machine Rates For Selected Forest Harvesting MachinesDocument32 pagesMachine Rates For Selected Forest Harvesting MachinesRuben DarioNo ratings yet

- Fin3003 ProjectDocument3 pagesFin3003 Projectapi-283310076No ratings yet

- Table of Interest Rates-En-2015Document24 pagesTable of Interest Rates-En-2015Doge IronyNo ratings yet

- Assignment On Financial Statement Analysis Berger Paints: School of Management StudiesDocument26 pagesAssignment On Financial Statement Analysis Berger Paints: School of Management StudiesAlkesh Mishra50% (2)

- Introduction of The Study: Meaning and Importance of FinanceDocument69 pagesIntroduction of The Study: Meaning and Importance of FinanceJeevitha MuruganNo ratings yet

- Origins of The French RevolutionDocument44 pagesOrigins of The French RevolutionEric JeanNo ratings yet

- CH 30 Money Growth and InflationDocument51 pagesCH 30 Money Growth and Inflationveroiren100% (1)

- CM2 Bafacr1xDocument18 pagesCM2 Bafacr1xAlly JeongNo ratings yet

- Model of Cash ManagementDocument11 pagesModel of Cash Managementaziz rehanNo ratings yet

- Shape of The MEC CurveDocument3 pagesShape of The MEC CurveYashas Mp100% (2)

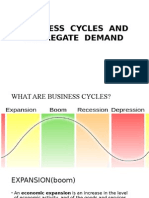

- Understanding Business Cycles and Aggregate DemandDocument40 pagesUnderstanding Business Cycles and Aggregate DemandSnehal Joshi100% (1)

- Arthur Kitson - A Fraudulent StandardDocument262 pagesArthur Kitson - A Fraudulent StandardmrpoissonNo ratings yet

- 4 Sec 186 Laons InvestmentsDocument7 pages4 Sec 186 Laons InvestmentsKumar SwamyNo ratings yet

- Jubilant FoodWorks Q4 FY19 Concall TranscriptDocument17 pagesJubilant FoodWorks Q4 FY19 Concall Transcriptsidd CoolNo ratings yet

- Banks Foreclose on Leasehold Rights of Resort Corporation Due to Loan DefaultDocument8 pagesBanks Foreclose on Leasehold Rights of Resort Corporation Due to Loan DefaultjrNo ratings yet

- Credit PerformanceDocument39 pagesCredit PerformanceMd Shawfiqul IslamNo ratings yet

- High-Risers: Cabrini-Green and the Fate of American Public HousingFrom EverandHigh-Risers: Cabrini-Green and the Fate of American Public HousingNo ratings yet

- Not a Crime to Be Poor: The Criminalization of Poverty in AmericaFrom EverandNot a Crime to Be Poor: The Criminalization of Poverty in AmericaRating: 4.5 out of 5 stars4.5/5 (37)

- Workin' Our Way Home: The Incredible True Story of a Homeless Ex-Con and a Grieving Millionaire Thrown Together to Save Each OtherFrom EverandWorkin' Our Way Home: The Incredible True Story of a Homeless Ex-Con and a Grieving Millionaire Thrown Together to Save Each OtherNo ratings yet

- When Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfFrom EverandWhen Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfRating: 5 out of 5 stars5/5 (36)

- Poor Economics: A Radical Rethinking of the Way to Fight Global PovertyFrom EverandPoor Economics: A Radical Rethinking of the Way to Fight Global PovertyRating: 4.5 out of 5 stars4.5/5 (263)

- Fucked at Birth: Recalibrating the American Dream for the 2020sFrom EverandFucked at Birth: Recalibrating the American Dream for the 2020sRating: 4 out of 5 stars4/5 (173)

- Charity Detox: What Charity Would Look Like If We Cared About ResultsFrom EverandCharity Detox: What Charity Would Look Like If We Cared About ResultsRating: 4 out of 5 stars4/5 (9)

- Same Kind of Different As Me Movie Edition: A Modern-Day Slave, an International Art Dealer, and the Unlikely Woman Who Bound Them TogetherFrom EverandSame Kind of Different As Me Movie Edition: A Modern-Day Slave, an International Art Dealer, and the Unlikely Woman Who Bound Them TogetherRating: 4 out of 5 stars4/5 (685)

- The Great Displacement: Climate Change and the Next American MigrationFrom EverandThe Great Displacement: Climate Change and the Next American MigrationRating: 4.5 out of 5 stars4.5/5 (32)

- Hillbilly Elegy: A Memoir of a Family and Culture in CrisisFrom EverandHillbilly Elegy: A Memoir of a Family and Culture in CrisisRating: 4 out of 5 stars4/5 (4277)

- The Great Displacement: Climate Change and the Next American MigrationFrom EverandThe Great Displacement: Climate Change and the Next American MigrationRating: 4 out of 5 stars4/5 (19)

- Heartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthFrom EverandHeartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthRating: 4 out of 5 stars4/5 (188)

- Nickel and Dimed: On (Not) Getting By in AmericaFrom EverandNickel and Dimed: On (Not) Getting By in AmericaRating: 4 out of 5 stars4/5 (186)

- The Meth Lunches: Food and Longing in an American CityFrom EverandThe Meth Lunches: Food and Longing in an American CityRating: 5 out of 5 stars5/5 (5)

- Superclass: The Global Power Elite and the World They Are MakingFrom EverandSuperclass: The Global Power Elite and the World They Are MakingRating: 3.5 out of 5 stars3.5/5 (32)

- Nickel and Dimed: On (Not) Getting By in AmericaFrom EverandNickel and Dimed: On (Not) Getting By in AmericaRating: 3.5 out of 5 stars3.5/5 (197)

- When Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfFrom EverandWhen Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfRating: 4 out of 5 stars4/5 (126)

- Alienated America: Why Some Places Thrive While Others CollapseFrom EverandAlienated America: Why Some Places Thrive While Others CollapseRating: 4 out of 5 stars4/5 (35)

- Sons, Daughters, and Sidewalk Psychotics: Mental Illness and Homelessness in Los AngelesFrom EverandSons, Daughters, and Sidewalk Psychotics: Mental Illness and Homelessness in Los AngelesNo ratings yet

- Heartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthFrom EverandHeartland: A Memoir of Working Hard and Being Broke in the Richest Country on EarthRating: 4 out of 5 stars4/5 (269)

- The Injustice of Place: Uncovering the Legacy of Poverty in AmericaFrom EverandThe Injustice of Place: Uncovering the Legacy of Poverty in AmericaRating: 4.5 out of 5 stars4.5/5 (2)

- Dark Days, Bright Nights: Surviving the Las Vegas Storm DrainsFrom EverandDark Days, Bright Nights: Surviving the Las Vegas Storm DrainsNo ratings yet

- Out of the Red: My Life of Gangs, Prison, and RedemptionFrom EverandOut of the Red: My Life of Gangs, Prison, and RedemptionNo ratings yet