You might also like

- Accidental InsuranceDocument33 pagesAccidental InsuranceHarinarayan PrajapatiNo ratings yet

- Claims Mangement in Life InsuranceDocument68 pagesClaims Mangement in Life InsurancePraveen Rautela100% (1)

- Principles of Insurance Law with Case StudiesFrom EverandPrinciples of Insurance Law with Case StudiesRating: 5 out of 5 stars5/5 (1)

- Project On Claims Management in Life InsuranceDocument69 pagesProject On Claims Management in Life InsuranceAnand ChavanNo ratings yet

- Project Report On MetlifeDocument85 pagesProject Report On MetlifeRadhikaWadhwaNo ratings yet

- Indian Insurance SectorDocument32 pagesIndian Insurance Sectorbanirumi100% (2)

- ASI Insurance PDFDocument5 pagesASI Insurance PDFSARDER JERIN SARAHNo ratings yet

- Accidental InsuranceDocument38 pagesAccidental InsuranceSohail ShaikhNo ratings yet

- Claims Management in Life InsuranceDocument7 pagesClaims Management in Life InsuranceJia GuptaNo ratings yet

- Insurance SectorDocument38 pagesInsurance SectorAjyPriNo ratings yet

- 04 Insurance CompanyDocument38 pages04 Insurance CompanyAnuska JayswalNo ratings yet

- Claims Management in Life InsuranceDocument53 pagesClaims Management in Life InsuranceJitesh100% (3)

- Brief History of Insurance Company in BangladeshDocument6 pagesBrief History of Insurance Company in BangladeshSarjeel Ahsan Niloy100% (2)

- Insurance - A Brief Overview: Chapter-1Document58 pagesInsurance - A Brief Overview: Chapter-1Sreeja Sahadevan75% (4)

- Insurance and Consumer Protection ActDocument40 pagesInsurance and Consumer Protection ActNadeem Malek100% (1)

- Insurance and Risk ManagementDocument9 pagesInsurance and Risk Managementmd fahadNo ratings yet

- Praful ProjectDocument63 pagesPraful Projectvikas yadavNo ratings yet

- A Report On Insurance Industry of NepalDocument7 pagesA Report On Insurance Industry of NepaldeepNo ratings yet

- Assaignment On Insurance DevelopmantDocument17 pagesAssaignment On Insurance DevelopmantShuvro RahmanNo ratings yet

- Insurance Black BookDocument61 pagesInsurance Black BookKunal Charaniya100% (1)

- C C CC CDocument20 pagesC C CC CSona ParthiNo ratings yet

- Insurance & Risk Management JUNE 2022Document11 pagesInsurance & Risk Management JUNE 2022Rajni KumariNo ratings yet

- Chapter - 1Document51 pagesChapter - 1Ankur SheelNo ratings yet

- Insurance Management MOD 3-4Document9 pagesInsurance Management MOD 3-4Sheba Mary SamNo ratings yet

- Executive SummaryDocument25 pagesExecutive SummaryRitika MahenNo ratings yet

- Underwriting of General InsuranceDocument42 pagesUnderwriting of General InsurancevandanaNo ratings yet

- Reliance Life InsuranceDocument98 pagesReliance Life Insuranceagoyal88100% (2)

- Assignment On InsrnceDocument16 pagesAssignment On InsrnceShahriar ShaonNo ratings yet

- Basics of InsuranceDocument20 pagesBasics of InsuranceSunny RajNo ratings yet

- Tata AIG Life InsuranceDocument62 pagesTata AIG Life InsuranceMitul Modi100% (1)

- Life InsuranceDocument55 pagesLife InsuranceNehaNo ratings yet

- Executive Summary: The Fact That The India Is The Emerging Market Is Throwing A Lot of CompetitionDocument11 pagesExecutive Summary: The Fact That The India Is The Emerging Market Is Throwing A Lot of CompetitionBibin PoNo ratings yet

- A Project Report OnDocument54 pagesA Project Report OnMahesh ChennurNo ratings yet

- Investment Opportunities in Insurance Sector: 1. Introduction of Life InsuranceDocument58 pagesInvestment Opportunities in Insurance Sector: 1. Introduction of Life InsuranceBiren DabhiNo ratings yet

- Insurance Company in BD Term PaperDocument19 pagesInsurance Company in BD Term PaperHabibur RahmanNo ratings yet

- Summer Project ReportDocument58 pagesSummer Project ReportRamchandra ChotaliaNo ratings yet

- HDFC Summer Training ProjectDocument86 pagesHDFC Summer Training ProjectDeepak SinghalNo ratings yet

- Rupali Life Insurance Company: A Report OnDocument19 pagesRupali Life Insurance Company: A Report OnHk RockyNo ratings yet

- Main ProjectDocument37 pagesMain ProjectKawalpreet Singh MakkarNo ratings yet

- Industrial Project On Reliance Life Insurance Company LimitedDocument116 pagesIndustrial Project On Reliance Life Insurance Company LimitedTimothy Brown100% (1)

- Complete Project Met Life IndiaDocument98 pagesComplete Project Met Life IndiaRaghu RamNo ratings yet

- A Project Report On Risk Analysis and RiDocument42 pagesA Project Report On Risk Analysis and RiJyoti ShuklaNo ratings yet

- LIC Project FinalDocument40 pagesLIC Project FinalSaroj KumarNo ratings yet

- Chapter 444Document6 pagesChapter 444kaylee dela cruzNo ratings yet

- Summer Training Report-Max New York LifeDocument40 pagesSummer Training Report-Max New York LifeAbhishek LaghateNo ratings yet

- P7Document6 pagesP7pardeshikanchan07No ratings yet

- Channel Development OF Icici Prudential Life Insurance Co. Ltd.-Process & ProblemsDocument45 pagesChannel Development OF Icici Prudential Life Insurance Co. Ltd.-Process & ProblemsPrakash DasNo ratings yet

- Project - Final in The MakingDocument55 pagesProject - Final in The MakingShivansh OhriNo ratings yet

- NavdeepDocument18 pagesNavdeepSnehal LadeNo ratings yet

- Insurance CompaniesDocument22 pagesInsurance CompaniesMoneeb ShahbazNo ratings yet

- A Comparative Study of With Other Global Non-Life Insurance CompaniesDocument10 pagesA Comparative Study of With Other Global Non-Life Insurance CompaniesRohit ChananaNo ratings yet

- Insurance ReportDocument17 pagesInsurance Reportbandana_pandey123100% (1)

- Role of Insurance Companies in Bangladesh EconomyDocument26 pagesRole of Insurance Companies in Bangladesh EconomyAyon ImtiazNo ratings yet

- Insurance Is A Means of Protection From Financial Loss. It Is A Form of Risk ManagementDocument10 pagesInsurance Is A Means of Protection From Financial Loss. It Is A Form of Risk Managementpriya tiwariNo ratings yet

- Insurance Law Unit 1Document9 pagesInsurance Law Unit 1Shivansh MishraNo ratings yet

- Project On Claims Management in Life InsuranceDocument60 pagesProject On Claims Management in Life Insurancepriya_1234563236986% (7)

- Book 9781412944564Document12 pagesBook 9781412944564Raihan RakibNo ratings yet

- A Glimpse of The Role of Insurance Companies in BangladeshDocument10 pagesA Glimpse of The Role of Insurance Companies in BangladeshRaihan RakibNo ratings yet

- SL NoDocument1 pageSL NoRaihan RakibNo ratings yet

- Inventory ModelsDocument3 pagesInventory ModelsRaihan RakibNo ratings yet

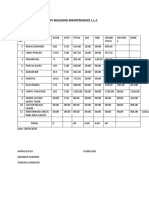

- Company Name: Alrady Building Maintenance L.L.C: TotalDocument3 pagesCompany Name: Alrady Building Maintenance L.L.C: TotalRaihan RakibNo ratings yet

- Affirmative Sentence To Negative SentenceDocument2 pagesAffirmative Sentence To Negative SentenceRaihan RakibNo ratings yet

- A Railway StationDocument4 pagesA Railway StationRaihan RakibNo ratings yet

- My First Day at SchoolDocument2 pagesMy First Day at SchoolRaihan RakibNo ratings yet

- International Compensation System of Multinational CorporationDocument22 pagesInternational Compensation System of Multinational CorporationRaihan RakibNo ratings yet

- Islamic Banking Tijarah Product (Musawamah)Document28 pagesIslamic Banking Tijarah Product (Musawamah)Yasir HameedNo ratings yet

- TortsDocument15 pagesTortsralph_atmosferaNo ratings yet

- 20) Franchise AgreementDocument5 pages20) Franchise AgreementranjnenduNo ratings yet

- DIGEST Manay V Cebu AirDocument1 pageDIGEST Manay V Cebu AirLala PastelleNo ratings yet

- Generic EULA Template: End-User License Agreement ("Agreement")Document2 pagesGeneric EULA Template: End-User License Agreement ("Agreement")NonoyLaurelFernandezNo ratings yet

- Chapter 7 Terms of PaymentDocument20 pagesChapter 7 Terms of Paymentmatthew kobulnickNo ratings yet

- 4BSA RFBT SET A No Answer PDFDocument7 pages4BSA RFBT SET A No Answer PDFLayca Clarice BrimbuelaNo ratings yet

- Japanese Model of Corporate GovernanceDocument16 pagesJapanese Model of Corporate GovernanceRuby Echavez100% (1)

- HEIRS OF LORETO MARAMAG Vs EVA VERNA MARAMAGDocument2 pagesHEIRS OF LORETO MARAMAG Vs EVA VERNA MARAMAGPaulo Villarin100% (1)

- Indeminity and GauranteeDocument26 pagesIndeminity and Gauranteeiamansh44No ratings yet

- IBC Amendments For Dec 2021 ExamDocument17 pagesIBC Amendments For Dec 2021 ExamShruthi SNo ratings yet

- CSB Joint Venture ToolkitDocument15 pagesCSB Joint Venture ToolkitImraan_001100% (1)

- CHAPTER 3 Sec. 1-3Document38 pagesCHAPTER 3 Sec. 1-3R ApigoNo ratings yet

- 3SECTION 2 Propery Rights of A PartnerDocument31 pages3SECTION 2 Propery Rights of A PartnerHarold B. Lacaba100% (1)

- Checklist Circular For Major Realisation / Very Substantial Disposal (Main Board)Document211 pagesChecklist Circular For Major Realisation / Very Substantial Disposal (Main Board)Timothy IpNo ratings yet

- KATHLEEN ObliCon Digests Baylon EndDocument14 pagesKATHLEEN ObliCon Digests Baylon EndDatu TahilNo ratings yet

- Contract Labour FORM XDocument1 pageContract Labour FORM Xhdpanchal86No ratings yet

- PAG-ASA STEEL WORKS, INC. vs. COURT OF APPEALSDocument1 pagePAG-ASA STEEL WORKS, INC. vs. COURT OF APPEALSmaximum jicaNo ratings yet

- Malaysia University of Science and Technology Master of Business AdministrationDocument18 pagesMalaysia University of Science and Technology Master of Business AdministrationE.H.SIANo ratings yet

- Final ExaminationDocument9 pagesFinal ExaminationCharles D. FloresNo ratings yet

- Freeman Shirt Manufacturing, Inc. vs. CIR, G.R. No. L-16561, January 28, 1961, 1 SCRA 353Document5 pagesFreeman Shirt Manufacturing, Inc. vs. CIR, G.R. No. L-16561, January 28, 1961, 1 SCRA 353Anonymous 8PX9c2XWSlNo ratings yet

- Definition of Estate: General Warranty DeedDocument5 pagesDefinition of Estate: General Warranty DeedMamun RashidNo ratings yet

- Olea Vs CA DigestDocument2 pagesOlea Vs CA DigestT Cel MrmgNo ratings yet

- SBI eDFS UndertakingDocument3 pagesSBI eDFS UndertakingVikram SinghNo ratings yet

- Test Bank For Essentials of Business Law and The Legal Environment 13th Edition Richard A Mann Barry S RobertsDocument14 pagesTest Bank For Essentials of Business Law and The Legal Environment 13th Edition Richard A Mann Barry S Robertscarolynwilliamsidyxwtsojp100% (26)

- 14-ATP-Escueta vs. LimDocument2 pages14-ATP-Escueta vs. LimJoesil DianneNo ratings yet

- Marine InsuranceDocument3 pagesMarine InsuranceKirtishbose ChowdhuryNo ratings yet

- Pemeriksaan Akuntansi I (Modul 9)Document19 pagesPemeriksaan Akuntansi I (Modul 9)Sri WulandariNo ratings yet

- GROUP 1 - Sec 53-58Document3 pagesGROUP 1 - Sec 53-58Joris YapNo ratings yet

- Muhammad Saad Saud 02-111192-015 B.LAW AssignmentDocument9 pagesMuhammad Saad Saud 02-111192-015 B.LAW Assignmentmuhammad saad saudNo ratings yet

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (98)

- Learn the Essentials of Business Law in 15 DaysFrom EverandLearn the Essentials of Business Law in 15 DaysRating: 4 out of 5 stars4/5 (13)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorFrom EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorRating: 4.5 out of 5 stars4.5/5 (63)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorFrom EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorRating: 4.5 out of 5 stars4.5/5 (132)

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Ben & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooFrom EverandBen & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooRating: 5 out of 5 stars5/5 (2)

- Contract Law in America: A Social and Economic Case StudyFrom EverandContract Law in America: A Social and Economic Case StudyNo ratings yet

- LLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessFrom EverandLLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessRating: 5 out of 5 stars5/5 (1)

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpFrom EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpRating: 4 out of 5 stars4/5 (228)

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersFrom EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNo ratings yet

- The Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersFrom EverandThe Startup Visa: U.S. Immigration Visa Guide for Startups and FoundersNo ratings yet

- Law of Leverage: The Key to Exponential WealthFrom EverandLaw of Leverage: The Key to Exponential WealthRating: 4.5 out of 5 stars4.5/5 (6)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementFrom EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementRating: 4.5 out of 5 stars4.5/5 (20)

- Nolo's Quick LLC: All You Need to Know About Limited Liability CompaniesFrom EverandNolo's Quick LLC: All You Need to Know About Limited Liability CompaniesRating: 4.5 out of 5 stars4.5/5 (7)

- California Employment Law: An Employer's Guide: Revised and Updated for 2024From EverandCalifornia Employment Law: An Employer's Guide: Revised and Updated for 2024No ratings yet

- A Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsFrom EverandA Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsNo ratings yet

- New York Management Law: The Practical Guide to Employment Law for Business Owners and ManagersFrom EverandNew York Management Law: The Practical Guide to Employment Law for Business Owners and ManagersNo ratings yet

- International Business Law: Cases and MaterialsFrom EverandInternational Business Law: Cases and MaterialsRating: 5 out of 5 stars5/5 (1)

- Business Startup Essentials For Nigerians: Comprehensive Guide For Starting And Profiting From Your BusinessFrom EverandBusiness Startup Essentials For Nigerians: Comprehensive Guide For Starting And Profiting From Your BusinessNo ratings yet