You might also like

- International Journal of Educational Research: April 2010Document8 pagesInternational Journal of Educational Research: April 2010Dini AprianiNo ratings yet

- International Journal of Educational Research: January 2010Document8 pagesInternational Journal of Educational Research: January 2010risaNo ratings yet

- Bakker Et al2011IJER TmLboundariesDocument8 pagesBakker Et al2011IJER TmLboundariesproduksi5202No ratings yet

- Bakker Et Al2011IJER TmLboundariesDocument7 pagesBakker Et Al2011IJER TmLboundariesFadli IhsanNo ratings yet

- Hasil Review Jurnal InternasionalDocument6 pagesHasil Review Jurnal Internasionaldewi ambarNo ratings yet

- ES 2011 1 VinckDocument21 pagesES 2011 1 Vinckbherrera1No ratings yet

- Tension Space Analysis: Exploring Community Requirements For Networked Urban ScreensDocument19 pagesTension Space Analysis: Exploring Community Requirements For Networked Urban ScreensAliaa Ahmed ShemariNo ratings yet

- 1 The Role of Mathematics and Modeling in A CompetenDocument9 pages1 The Role of Mathematics and Modeling in A CompetenNothing NameNo ratings yet

- PR 234Document16 pagesPR 234PrinceNo ratings yet

- Made in Criticalland - Ward-WilkieDocument7 pagesMade in Criticalland - Ward-Wilkieprem_chandranNo ratings yet

- Explainable Artificial IntelligenceDocument17 pagesExplainable Artificial IntelligenceigfucaNo ratings yet

- BCCDJMNW2011EODocument33 pagesBCCDJMNW2011EOranim najibNo ratings yet

- AkkermanBronkhorstZitter EducationalDesignResearchDocument22 pagesAkkermanBronkhorstZitter EducationalDesignResearchfabianoramos.educNo ratings yet

- Why Do We Need Ontology For Agent-Based ModelsDocument15 pagesWhy Do We Need Ontology For Agent-Based ModelsKhalil ChihaNo ratings yet

- Augmented Reality in Education An Overview of Twenty Five Years of ResearchDocument30 pagesAugmented Reality in Education An Overview of Twenty Five Years of Researcheslam.ragab202070No ratings yet

- Business Skills for Engineers and TechnologistsFrom EverandBusiness Skills for Engineers and TechnologistsRating: 3 out of 5 stars3/5 (1)

- WRITING ONE-ICTinELT-HocklyDudeneyDocument11 pagesWRITING ONE-ICTinELT-HocklyDudeneyEndy HamiltonNo ratings yet

- The Ethics of Computing: ACM Computing Surveys February 2016Document39 pagesThe Ethics of Computing: ACM Computing Surveys February 2016Daniel braveNo ratings yet

- E-Research Is A Fad: Scholarship 2.0, Cyberinfrastructure, and IT GovernanceDocument10 pagesE-Research Is A Fad: Scholarship 2.0, Cyberinfrastructure, and IT GovernanceRachmansyah IINo ratings yet

- Le Rôle Des Scénarios Et Des Démonstrateurs Dans La Promotion D'une Compréhension Partagée Dans Les Projets D'innovationDocument22 pagesLe Rôle Des Scénarios Et Des Démonstrateurs Dans La Promotion D'une Compréhension Partagée Dans Les Projets D'innovationcuriosityNo ratings yet

- A Review of Sociotechnical Systems TheoryTIESDocument50 pagesA Review of Sociotechnical Systems TheoryTIESAnandu S KrishnaNo ratings yet

- Unit IIIDocument27 pagesUnit IIITarun MittalNo ratings yet

- SSRN Id1731948Document39 pagesSSRN Id1731948MIKAELA BEATRICE LOPEZNo ratings yet

- Professional ResponsibilityDocument15 pagesProfessional ResponsibilitysafsaniaalyaNo ratings yet

- Andreeva - One Solution For Semantic Data Integration in LogisticsDocument13 pagesAndreeva - One Solution For Semantic Data Integration in LogisticsMarkus SchattenNo ratings yet

- GOODMAN - Understanding Interaction Design PracticesDocument11 pagesGOODMAN - Understanding Interaction Design Practicesuatolipo95No ratings yet

- VLEsDillernbourg Pierre 2002aDocument18 pagesVLEsDillernbourg Pierre 2002aSANDRA MILENA CAMELO PINILLANo ratings yet

- E-Science - Open, Social and Virtual Techno - Claudia KoschtialDocument192 pagesE-Science - Open, Social and Virtual Techno - Claudia KoschtialmaeslorNo ratings yet

- Assessment For Learning in Primary Technology ClasDocument10 pagesAssessment For Learning in Primary Technology ClasYunita SafitriNo ratings yet

- User Experience and The Idea of Design in HCI: Lecture Notes in Computer Science January 2006Document15 pagesUser Experience and The Idea of Design in HCI: Lecture Notes in Computer Science January 2006Priceless TechnologiesNo ratings yet

- PSI PaperDocument29 pagesPSI PaperHuyen T. T. NguyenNo ratings yet

- Towards A Theory of Ecosystems: Strategic Management Journal March 2018Document41 pagesTowards A Theory of Ecosystems: Strategic Management Journal March 2018Sasha KingNo ratings yet

- The-Interdisciplinarity-of-the-Information-Science VERDocument37 pagesThe-Interdisciplinarity-of-the-Information-Science VERRoberto BarbosaNo ratings yet

- Formal Mathematics For MathematiciansDocument4 pagesFormal Mathematics For MathematiciansDevrush RedlifeNo ratings yet

- 2010 Mechatronics More Questions Than AnswersDocument15 pages2010 Mechatronics More Questions Than AnswersnileshsawNo ratings yet

- KT I PDFDocument17 pagesKT I PDFLiza KhanamNo ratings yet

- Professional ResponsibilityDocument12 pagesProfessional ResponsibilitylolNo ratings yet

- Concepts For Modeling Enterprise ArchitecturesDocument22 pagesConcepts For Modeling Enterprise Architecturesmeifta fitria kuntaryNo ratings yet

- Social DesignDocument59 pagesSocial DesignHelen Rocio MartínezNo ratings yet

- Linton - 2017 - Emerging Technology Supply ChainsDocument3 pagesLinton - 2017 - Emerging Technology Supply ChainsJacobo CordobaNo ratings yet

- BenMartin PDFDocument17 pagesBenMartin PDFMaria Conceiçao da CostaNo ratings yet

- What Is Design Thinking and Why Is It Important?: Review of Educational Research September 2012Document20 pagesWhat Is Design Thinking and Why Is It Important?: Review of Educational Research September 2012Profe DanielNo ratings yet

- Ai Na Sala de AulaDocument13 pagesAi Na Sala de AulaMaralto MaraltooNo ratings yet

- Ethicsandtechnologydesign AlbrechtslundDocument11 pagesEthicsandtechnologydesign AlbrechtslundmghaseghNo ratings yet

- Bio-Inspired, Flexible Structures and Materials: August 2014Document17 pagesBio-Inspired, Flexible Structures and Materials: August 2014Josielyn ArrezaNo ratings yet

- A Cognitive Approach To Manage The Complexity of Digital Twin SystemsDocument12 pagesA Cognitive Approach To Manage The Complexity of Digital Twin Systemsgeng qinNo ratings yet

- dtw2016 Edison Datascience FW v05Document8 pagesdtw2016 Edison Datascience FW v05Kassahu alebelNo ratings yet

- What Is Design ThinkingDocument20 pagesWhat Is Design ThinkingPrathamesh PittuleNo ratings yet

- Technological Forecasting & Social Change: Munan Li, Alan L. Porter, Arho SuominenDocument12 pagesTechnological Forecasting & Social Change: Munan Li, Alan L. Porter, Arho SuominenJoão Guzmán GutiérrezNo ratings yet

- Learning Sciences and Learning Engineering A Natural or Artificial DistinctionDocument18 pagesLearning Sciences and Learning Engineering A Natural or Artificial Distinctionsbai.hanae.uh2No ratings yet

- An Introduction To Communicating ScienceDocument21 pagesAn Introduction To Communicating SciencezaraNo ratings yet

- Understanding The Digital Divide A Literature SurvDocument40 pagesUnderstanding The Digital Divide A Literature SurvAnindhita ParasdyaNo ratings yet

- Engineering Education and Importance of Humanities and SciencesDocument10 pagesEngineering Education and Importance of Humanities and SciencestigersayoojNo ratings yet

- Beyond Models and Metaphors Complexity Theory, Systems Thinking and - Bousquet & CurtisDocument21 pagesBeyond Models and Metaphors Complexity Theory, Systems Thinking and - Bousquet & CurtisEra B. LargisNo ratings yet

- Isms in Information Science Constructivism Collec PDFDocument24 pagesIsms in Information Science Constructivism Collec PDFThiagoNo ratings yet

- Handbook of Research On Educational Communications and Technology, 3rd EditionDocument5 pagesHandbook of Research On Educational Communications and Technology, 3rd EditionJason UnderwoodNo ratings yet

- A Manifesto For Web SciencDocument6 pagesA Manifesto For Web SciencΑλέξανδρος ΓεωργίουNo ratings yet

- The Emotional Content of The Physical Space-LibreDocument13 pagesThe Emotional Content of The Physical Space-LibrevickycamilleriNo ratings yet

- The Future Book or The Future of The Book: January 2021Document7 pagesThe Future Book or The Future of The Book: January 2021alexNo ratings yet

- Book Review Book Review: February 2021Document3 pagesBook Review Book Review: February 2021alexNo ratings yet

- Contoh Template CV Dalam Bahasa InggrisDocument1 pageContoh Template CV Dalam Bahasa InggrisPegy SaputroNo ratings yet

- Groundnut Paper: April 2021Document5 pagesGroundnut Paper: April 2021alexNo ratings yet

- Book Review: April 2021Document5 pagesBook Review: April 2021alexNo ratings yet

- In Defense of The PaperDocument10 pagesIn Defense of The PaperalexNo ratings yet

- In Defense of The PaperDocument10 pagesIn Defense of The PaperalexNo ratings yet

- Letter To The Editor: April 2021Document4 pagesLetter To The Editor: April 2021alexNo ratings yet

- Letter To The Editor: Indian Journal of Pain April 2021Document3 pagesLetter To The Editor: Indian Journal of Pain April 2021alexNo ratings yet

- Blacklisted Journal Publishers and Their Respective JournalsDocument4 pagesBlacklisted Journal Publishers and Their Respective JournalsReza FadhilaNo ratings yet

- Book PDF: Vandana SinghDocument2 pagesBook PDF: Vandana SinghalexNo ratings yet

- 895 KW 1,200 HP: Gross HorsepowerDocument14 pages895 KW 1,200 HP: Gross HorsepowerJudy WrightNo ratings yet

- Management of CashDocument14 pagesManagement of Cashfrw dm100% (1)

- Final Blackbook On Role of AdvertisingDocument62 pagesFinal Blackbook On Role of AdvertisingArjun Choudhary50% (6)

- Fundamentals of Retailing and Shopper MarketingDocument40 pagesFundamentals of Retailing and Shopper MarketingErose StNo ratings yet

- Coca Cola Marketing PlanDocument9 pagesCoca Cola Marketing PlanraghavbansalNo ratings yet

- Sale AgreementDocument5 pagesSale AgreementAdvocate Ladiil100% (1)

- Summer TitlesDocument13 pagesSummer TitlesManish SantaniNo ratings yet

- Business ProposalDocument9 pagesBusiness ProposalJimron Brix AlcalaNo ratings yet

- SAP SD Interview QuestionsDocument23 pagesSAP SD Interview Questionskanhaiya_priyadarshi100% (1)

- POM II Final Report On SCM of Flipkart PDFDocument18 pagesPOM II Final Report On SCM of Flipkart PDFraazNo ratings yet

- Hbo Quiz 1Document1 pageHbo Quiz 1PRINCESS HONEYLET SIGESMUNDONo ratings yet

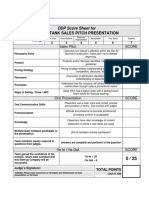

- Shark Tank DDP Sales Pitch RubricDocument1 pageShark Tank DDP Sales Pitch Rubricapi-308044486No ratings yet

- Factors Considered For The Tooling Decision On Derive The Process ParameterDocument2 pagesFactors Considered For The Tooling Decision On Derive The Process ParameterMithun RajNo ratings yet

- 01 Intro To ServicesDocument59 pages01 Intro To ServicesOmkar ParshuramNo ratings yet

- History of MarkettingDocument7 pagesHistory of MarkettingFranckkMnster0% (1)

- Shraddha Kaushik: Marketing ManagementDocument86 pagesShraddha Kaushik: Marketing ManagementSunil JoshiNo ratings yet

- MBA - Strategic Management + AnswersDocument24 pagesMBA - Strategic Management + AnswersOlusegun Olasunkanmi PatNo ratings yet

- Final Marketing Strategy ICICIDocument36 pagesFinal Marketing Strategy ICICIAbhishek MishraNo ratings yet

- Automobile Bill of Sale - AS ISDocument9 pagesAutomobile Bill of Sale - AS ISFindLegalFormsNo ratings yet

- My Revision Notes - AQA A Level Business PDFDocument469 pagesMy Revision Notes - AQA A Level Business PDFreneexxj100% (3)

- Chapter - 6 Pillers of Marketing (STPD)Document82 pagesChapter - 6 Pillers of Marketing (STPD)Book wormNo ratings yet

- Terms and Conditions AggrementDocument16 pagesTerms and Conditions AggrementfuadNo ratings yet

- A Game Plan For Success in Data AnalyticsDocument118 pagesA Game Plan For Success in Data AnalyticsRudi CelebesNo ratings yet

- Amazon Strategic AnalysisDocument44 pagesAmazon Strategic AnalysisBradley Paynter83% (6)

- NestleDocument24 pagesNestleBaleissaNo ratings yet

- Proctor & Gamble Company: Case AnalysisDocument17 pagesProctor & Gamble Company: Case AnalysisSaurabh Antapurkar100% (1)

- GROUP 2 - IS Application at Operational LevelDocument68 pagesGROUP 2 - IS Application at Operational LevelBayu Widhi RespatiNo ratings yet

- UWIN BIE13 s23Document23 pagesUWIN BIE13 s23elearninglsprNo ratings yet

- Pending Order Root CauseDocument7 pagesPending Order Root CauseRahma MaulidaNo ratings yet

- Chapter 1 - Introduction To CBDocument26 pagesChapter 1 - Introduction To CBSagar100% (1)

- Marketing Plan - Ruwan LakmalDocument10 pagesMarketing Plan - Ruwan Lakmalsam rosNo ratings yet