You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Natural Law Trust Ebook 11 - 14 - 2020Document83 pagesThe Natural Law Trust Ebook 11 - 14 - 2020Annette Mulkay100% (3)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 2024 YORP Registration FormDocument3 pages2024 YORP Registration FormiKei NotNo ratings yet

- Training Request Form: Section A - Employee InformationDocument4 pagesTraining Request Form: Section A - Employee Informationpj4allNo ratings yet

- PCAR Part 9 Evaluation - An AOC's Quality SystemDocument5 pagesPCAR Part 9 Evaluation - An AOC's Quality SystemJohn KevinNo ratings yet

- Aud Theory CompiledDocument495 pagesAud Theory Compiledaperez1105100% (1)

- Mandaue Galleon Trade v. IsidtoDocument2 pagesMandaue Galleon Trade v. IsidtoWendell Leigh OasanNo ratings yet

- Kinds of Taxes: Income SourceDocument18 pagesKinds of Taxes: Income SourceXie LicyayoNo ratings yet

- Region Xi Orientation On Memorandum Circular 2021-054Document40 pagesRegion Xi Orientation On Memorandum Circular 2021-054keith tanueco100% (2)

- 264 - 2023-02-10 - B. Favre Motion To Dismiss Amended Complaint W MemorandumDocument33 pages264 - 2023-02-10 - B. Favre Motion To Dismiss Amended Complaint W MemorandumUSA TODAY NetworkNo ratings yet

- Assignment #1 (Group) Group#1: Investment Regulation in IndonesiaDocument3 pagesAssignment #1 (Group) Group#1: Investment Regulation in IndonesiaZalal PaneNo ratings yet

- Case XeroxDocument3 pagesCase XeroxZalal PaneNo ratings yet

- Understanding The Microeconomy and The Role of Government: Part Two Part ThreeDocument34 pagesUnderstanding The Microeconomy and The Role of Government: Part Two Part ThreeZalal PaneNo ratings yet

- Key Learning Zalal Bakti 5th WeekDocument1 pageKey Learning Zalal Bakti 5th WeekZalal PaneNo ratings yet

- Syllabus of Managerial Economics Batch 3-2020Document7 pagesSyllabus of Managerial Economics Batch 3-2020Zalal PaneNo ratings yet

- Demand & Supply - MM Sesi 3Document21 pagesDemand & Supply - MM Sesi 3Zalal PaneNo ratings yet

- People Powering Contemporary Supply ChainsDocument20 pagesPeople Powering Contemporary Supply ChainsZalal PaneNo ratings yet

- Factors of A Successful PPPDocument13 pagesFactors of A Successful PPPDawn SimNo ratings yet

- Trail Balance As On 31-3-10Document9 pagesTrail Balance As On 31-3-10Uday AkbariNo ratings yet

- Osinbajo 60 PointsDocument8 pagesOsinbajo 60 PointsAbimbola OyarinuNo ratings yet

- Business Law Term PaperDocument1 pageBusiness Law Term Paperjpelland1No ratings yet

- KSEF Strucutred Electronic Invoice Dec2022 enDocument158 pagesKSEF Strucutred Electronic Invoice Dec2022 enfebeb26145No ratings yet

- White Knight Hotel St. Anne Business Permit 2022Document3 pagesWhite Knight Hotel St. Anne Business Permit 2022Jesus PinedaNo ratings yet

- Ke Government Gazette Dated 1999 05 21 No 28 PDFDocument32 pagesKe Government Gazette Dated 1999 05 21 No 28 PDFroy_revieNo ratings yet

- Form No 49BDocument5 pagesForm No 49BVedant DistributorsNo ratings yet

- Redevelopment of Toronto Waterfront: Planning and Management of World CitiesDocument14 pagesRedevelopment of Toronto Waterfront: Planning and Management of World CitiesbibekNo ratings yet

- Nism Series 8 Pay SlipDocument2 pagesNism Series 8 Pay SlipHritik SharmaNo ratings yet

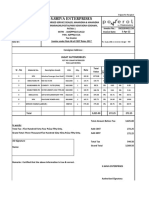

- S.Shiva Enterprises: Jagat AutomobilesDocument2 pagesS.Shiva Enterprises: Jagat AutomobilesS.SHIVA ENTERPRISESNo ratings yet

- Contemp ReviewerDocument7 pagesContemp ReviewerMark Louie CunananNo ratings yet

- The New Rich in AsiaDocument31 pagesThe New Rich in AsiaIrdinaNo ratings yet

- Insurance Regulatory and Development Authority of India (IRDA) - UPSC NotesDocument2 pagesInsurance Regulatory and Development Authority of India (IRDA) - UPSC NotesAam aadmiNo ratings yet

- Construction Company Registration RequirementsDocument4 pagesConstruction Company Registration RequirementsMunusamy RajiNo ratings yet

- IRCTC Retiring RoomDocument1 pageIRCTC Retiring RoomGSAIBABANo ratings yet

- Italy Visa Application Center - Annaba Appointment LetterDocument2 pagesItaly Visa Application Center - Annaba Appointment Letteryouneschouf93No ratings yet

- CAVALCANTE & LOTTA - Middle-Level Bureaucrats - Profile, Trajectory and PerformanceDocument308 pagesCAVALCANTE & LOTTA - Middle-Level Bureaucrats - Profile, Trajectory and PerformanceTiago BrandãoNo ratings yet

- Private Sector Banks Comparative Analysis 1HFY22Document12 pagesPrivate Sector Banks Comparative Analysis 1HFY22Tushar Mohan0% (1)

- 27th January Current Affairs 2022Document17 pages27th January Current Affairs 2022john powerNo ratings yet

- OLFU GBERMIC Chapter-1Document8 pagesOLFU GBERMIC Chapter-1Hannah LopezNo ratings yet