You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- 04 Activity 1 - AgnoDocument2 pages04 Activity 1 - AgnoJen DeloyNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- 04 Quiz 1 - Ca2Document8 pages04 Quiz 1 - Ca2Jen DeloyNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- 09 TASK PERFORMANCE 1 - GovDocument2 pages09 TASK PERFORMANCE 1 - GovJen DeloyNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- 04 Case Problem - SheDocument13 pages04 Case Problem - SheJen DeloyNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Instructions: Compose A Belief About Love, Which Must Be Based On Their Personal ExperienceDocument1 pageInstructions: Compose A Belief About Love, Which Must Be Based On Their Personal ExperienceJen DeloyNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- 07 Quiz 1 - SCMDocument1 page07 Quiz 1 - SCMJen DeloyNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- 07 Task Performance 1 - AuditDocument5 pages07 Task Performance 1 - AuditJen DeloyNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- 07 Task Performance 1 - FinmarDocument2 pages07 Task Performance 1 - FinmarJen DeloyNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- 11 TP 1 - GovDocument2 pages11 TP 1 - GovJen Deloy100% (1)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- 02 Checkpoint Activity 1 Case Analyses: Accrual For Accounting Case 1Document1 page02 Checkpoint Activity 1 Case Analyses: Accrual For Accounting Case 1Jen DeloyNo ratings yet

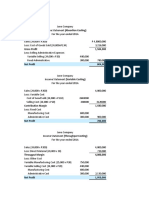

- Net Cash Flow From Operating Activities 1,222,000Document1 pageNet Cash Flow From Operating Activities 1,222,000Jen DeloyNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- 01 Elms Activity 2 Ia3Document1 page01 Elms Activity 2 Ia3Jen DeloyNo ratings yet

- 02 Activity 1 - FinmarDocument1 page02 Activity 1 - FinmarJen DeloyNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Solution:: Purchases, Cash Basis P 2,850,000Document2 pagesSolution:: Purchases, Cash Basis P 2,850,000Jen Deloy50% (2)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- 01 Elms Activity 1 - Ia3Document1 page01 Elms Activity 1 - Ia3Jen DeloyNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- TPBALANCESHEET DeloyDocument1 pageTPBALANCESHEET DeloyJen DeloyNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Case Study Research DesignDocument12 pagesCase Study Research DesignOrsua Janine AprilNo ratings yet

- An Investigation Into The Use of GAMA Water Tunnel For Visualization of Vortex Breakdown On The Delta WingDocument7 pagesAn Investigation Into The Use of GAMA Water Tunnel For Visualization of Vortex Breakdown On The Delta WingEdy BudimanNo ratings yet

- Making LoveDocument5 pagesMaking LoveapplecommentNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Podar School HomeworkDocument7 pagesPodar School Homeworkerr64wxh100% (1)

- List HargaDocument28 pagesList HargaFitra noviandaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Bai Tap On Tap Unit 123Document8 pagesBai Tap On Tap Unit 123Le VanNo ratings yet

- SafewayDocument7 pagesSafewayapi-671978278No ratings yet

- The Ultimate Closed SicilianDocument180 pagesThe Ultimate Closed SicilianJorge Frank Ureña100% (4)

- Mat Lab Interview QuestionsDocument2 pagesMat Lab Interview QuestionsSiddu Shiva KadiwalNo ratings yet

- (Lib-Ebooks Com) 240820202341 PDFDocument193 pages(Lib-Ebooks Com) 240820202341 PDFDr. Hisham Abdul MajeedNo ratings yet

- Irjece: Human Computer Interaction Direct ManipulationDocument4 pagesIrjece: Human Computer Interaction Direct ManipulationgigibowonseetNo ratings yet

- Expressions - House & Home Idioms in EnglishDocument3 pagesExpressions - House & Home Idioms in EnglishKathy SolisNo ratings yet

- 2 Obstacle Avoiding Robot PDFDocument7 pages2 Obstacle Avoiding Robot PDFRaj AryanNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Respiratory SystemDocument9 pagesRespiratory Systemtheglobalnursing89% (9)

- Writing Skill - B1.Khung Trình Đ Chung Châu Âu (CEFR)Document4 pagesWriting Skill - B1.Khung Trình Đ Chung Châu Âu (CEFR)dongxugioNo ratings yet

- R 480200Document6 pagesR 480200Shubhi JainNo ratings yet

- Sort Notes PJDocument8 pagesSort Notes PJPurushottam Choudhary0% (1)

- Vice President Procurement Supply Chain in Dallas TX Resume Gary McKownDocument3 pagesVice President Procurement Supply Chain in Dallas TX Resume Gary McKownGarymckownNo ratings yet

- ISLaw ComputationDocument6 pagesISLaw ComputationNurlailah Ali100% (1)

- Week 3Document9 pagesWeek 3LOVELY MAE GLUDONo ratings yet

- (SOLUTION) Chapter 3 - P3-5Document7 pages(SOLUTION) Chapter 3 - P3-5Nguyễn Quỳnh AnhNo ratings yet

- Larranaga V CADocument15 pagesLarranaga V CAKhay AnnNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- FPGA and PLD SurveyDocument29 pagesFPGA and PLD SurveykavitaNo ratings yet

- Verbyla Et Al. - 2013Document6 pagesVerbyla Et Al. - 2013Johnny Jala QuirozNo ratings yet

- Piano 2023 2024 Grade 6Document13 pagesPiano 2023 2024 Grade 6Lucas Moreira0% (1)

- Legacy - Wasteland AlmanacDocument33 pagesLegacy - Wasteland AlmanacВлад «Befly» Мирошниченко100% (3)

- 123 AP / 0123 TS: Intermediate Public Examinations - 2024Document3 pages123 AP / 0123 TS: Intermediate Public Examinations - 2024srinivasveeravalli123aNo ratings yet

- Oktoberfest ReportDocument28 pagesOktoberfest ReportUvin RanaweeraNo ratings yet

- Matlab TutorialDocument182 pagesMatlab TutorialSajjad Pasha MohammadNo ratings yet

- Week 2 Reflection Sept 6 To Sept 10Document2 pagesWeek 2 Reflection Sept 6 To Sept 10api-534401949No ratings yet