You might also like

- Get Free Spins Get Free Coins Coin Master GeneratorDocument3 pagesGet Free Spins Get Free Coins Coin Master GeneratorUnknown11No ratings yet

- 7-1B Systems of Linear Equations GraphingDocument23 pages7-1B Systems of Linear Equations GraphingDimas HakriNo ratings yet

- Employee Offboarding Checklist 1679881966Document4 pagesEmployee Offboarding Checklist 1679881966Novianti Alit RahayuNo ratings yet

- Ac 160Document12 pagesAc 160kanbouchNo ratings yet

- Decentralized Autonomous Organization The Book of DAO Business in the Next Generation Strategies of the Couch CEO The Healthcare and Insurance Industries Gone Blockchain 2022: Digital money, Crypto Blockchain Bitcoin Altcoins Ethereum litecoin, #1From EverandDecentralized Autonomous Organization The Book of DAO Business in the Next Generation Strategies of the Couch CEO The Healthcare and Insurance Industries Gone Blockchain 2022: Digital money, Crypto Blockchain Bitcoin Altcoins Ethereum litecoin, #1No ratings yet

- Blockchain Case StudiesDocument5 pagesBlockchain Case StudiesSri K.Gangadhar Rao Assistant ProfessorNo ratings yet

- Common Core Grade 5 Math Printable WorksheetsDocument3 pagesCommon Core Grade 5 Math Printable WorksheetsJessicaNo ratings yet

- Fintech ReportDocument24 pagesFintech ReportAnvesha TyagiNo ratings yet

- Resource Allocation Failure Service Degraded PDFDocument11 pagesResource Allocation Failure Service Degraded PDFyacine bouazniNo ratings yet

- Smart Stamp DutyDocument12 pagesSmart Stamp DutyYudhis YudhistiraNo ratings yet

- Implementing Blockchain Application, Do You Think Blockchain Will Eventually Gain Popularity in The Shipping Industry?Document3 pagesImplementing Blockchain Application, Do You Think Blockchain Will Eventually Gain Popularity in The Shipping Industry?Ahmed FathyNo ratings yet

- Will Blockchain Change The Future of Finance and Accounting?Document3 pagesWill Blockchain Change The Future of Finance and Accounting?khushboosingh25junNo ratings yet

- BlockchainDocument8 pagesBlockchainSuhanNo ratings yet

- B17 BlockchainApplicationInInsurance ArticleDocument5 pagesB17 BlockchainApplicationInInsurance ArticleKashish MehtaNo ratings yet

- Fraud Prevention in Taxation System of Pakistan Using Blockchain TechnologyDocument5 pagesFraud Prevention in Taxation System of Pakistan Using Blockchain TechnologyHassan AbbasNo ratings yet

- Blockchain and The Future of Audit by Ernst & YoungDocument5 pagesBlockchain and The Future of Audit by Ernst & YoungRanganathan PKNo ratings yet

- Roland Berger Blockchain A Promising Technology For The Belgian Public AdministrDocument16 pagesRoland Berger Blockchain A Promising Technology For The Belgian Public AdministrKamal TabajaNo ratings yet

- EditedDocument2 pagesEditedcaro wainainaNo ratings yet

- A Novel Approach For Invoice Management Using BlockchainDocument5 pagesA Novel Approach For Invoice Management Using BlockchainInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Blockchain Technology Application For Value-Added Tax SystemsDocument27 pagesBlockchain Technology Application For Value-Added Tax SystemsGeysa Pratama EriatNo ratings yet

- The Futurist - XIMBDocument3 pagesThe Futurist - XIMBRuchi AgrawalNo ratings yet

- Technology Advancement Likely To Heavily Impact How Taxpayers Interact With Tax Authorities in The FutureDocument2 pagesTechnology Advancement Likely To Heavily Impact How Taxpayers Interact With Tax Authorities in The FutureRohullah RafatNo ratings yet

- Blockchain Maritime IshanDocument3 pagesBlockchain Maritime IshanNaveen KenchanagoudarNo ratings yet

- Applying Blockchain To Trade FinanceDocument5 pagesApplying Blockchain To Trade FinanceVikram SuranaNo ratings yet

- Blockchain After BitcoinDocument6 pagesBlockchain After BitcoinStephen TanNo ratings yet

- Impacts of Blockchain On Accounting Profession.: Name 1Document9 pagesImpacts of Blockchain On Accounting Profession.: Name 1fredNo ratings yet

- Blockchain in The Cyber World: What Is A BlockchainDocument4 pagesBlockchain in The Cyber World: What Is A BlockchainSumit SharmaNo ratings yet

- 5421 17976 1 PBDocument23 pages5421 17976 1 PBBonya SusatyoNo ratings yet

- Assigment - 2 Ramesh Chandra SinghDocument21 pagesAssigment - 2 Ramesh Chandra SinghRameshchandra SinghNo ratings yet

- Ta558909 Fair Taxation Special ReportDocument4 pagesTa558909 Fair Taxation Special ReportsyahrilNo ratings yet

- Blockchain For Construction WhitepaperDocument12 pagesBlockchain For Construction WhitepaperMaeNo ratings yet

- Blockchain NFTA Information Sheet - Standards - Org.au OurOrganisation Events DocumentsDocument4 pagesBlockchain NFTA Information Sheet - Standards - Org.au OurOrganisation Events DocumentsyezdiarwNo ratings yet

- Diving Into Blockchain Use Cases - Wholesale Energy Trading - Cleantech GroupDocument4 pagesDiving Into Blockchain Use Cases - Wholesale Energy Trading - Cleantech GroupregonzalNo ratings yet

- Block ChainDocument11 pagesBlock Chainrupak05No ratings yet

- Business Trends - Application of Blockchain Technology in The Petrochemical IndustryDocument6 pagesBusiness Trends - Application of Blockchain Technology in The Petrochemical IndustryrubenpeNo ratings yet

- It Audit Fundamentals What To Audit? Format Journal 1. Abstract Past Tense, Short Summary of The Whole Paper 2. Intro General ObjectiveDocument8 pagesIt Audit Fundamentals What To Audit? Format Journal 1. Abstract Past Tense, Short Summary of The Whole Paper 2. Intro General ObjectiveMaan RetulinNo ratings yet

- A2 Business Times 7-19Document1 pageA2 Business Times 7-19Price LangNo ratings yet

- Business Management: Executive Summary 3Document19 pagesBusiness Management: Executive Summary 3pamelaNo ratings yet

- Deloitte - BlockchainDocument4 pagesDeloitte - BlockchainRaj KrishnaNo ratings yet

- Banking Is Only The Beginning - BlockchainDocument26 pagesBanking Is Only The Beginning - BlockchainValerie GheroldNo ratings yet

- 1 SMDocument12 pages1 SMiamrov29No ratings yet

- University of The Cumberlands Final Paper ITS 832 - Info Tech in A Global EconomyDocument10 pagesUniversity of The Cumberlands Final Paper ITS 832 - Info Tech in A Global EconomySrinivas AdityaNo ratings yet

- CouldDocument8 pagesCoulddhoniNo ratings yet

- Six Technologies Changing FinanceDocument4 pagesSix Technologies Changing FinanceSameer KalamkarNo ratings yet

- Blockchain in Oil and Gas IndustryDocument4 pagesBlockchain in Oil and Gas IndustrySingh JINo ratings yet

- Tax Law, SubhamDocument9 pagesTax Law, SubhamSugam AgrawalNo ratings yet

- 10 YaymanFInalDocument16 pages10 YaymanFInallukitocareerNo ratings yet

- Block ChainDocument6 pagesBlock Chainsaksham guptaNo ratings yet

- Lec 6Document46 pagesLec 6Samuel RomanyNo ratings yet

- Record ManagementDocument2 pagesRecord Managementswakrit banikNo ratings yet

- Dani's TaxDocument5 pagesDani's TaxNatnhael WondafrashNo ratings yet

- Current Tax Emerging Trends in KenyaDocument2 pagesCurrent Tax Emerging Trends in KenyaMashel MichNo ratings yet

- بشير 7Document23 pagesبشير 7Basheer Yousif IsmailNo ratings yet

- BlockchainDocument3 pagesBlockchainIssacNo ratings yet

- Koinswap WhitepaperDocument25 pagesKoinswap WhitepaperRizen btrNo ratings yet

- The Relevance of E-Commerce Tax Application in Indonesia: Based On The Perspective of Taxation ExpertDocument15 pagesThe Relevance of E-Commerce Tax Application in Indonesia: Based On The Perspective of Taxation ExpertAdeel KhalidNo ratings yet

- Cloud Accounting A New Business Model in A Challenging ContextDocument7 pagesCloud Accounting A New Business Model in A Challenging ContextmohammedelamenNo ratings yet

- In Ps Blockchain Noexp PDFDocument32 pagesIn Ps Blockchain Noexp PDFMurali DharanNo ratings yet

- Block Chain and Logistics Sector: How Will Blockchain Technologies Affect The Logistics?Document2 pagesBlock Chain and Logistics Sector: How Will Blockchain Technologies Affect The Logistics?dsdsdNo ratings yet

- Blockchain The Road Ahead With Context To Indian Economy: National Journal of Multidisciplinary Research and DevelopmentDocument4 pagesBlockchain The Road Ahead With Context To Indian Economy: National Journal of Multidisciplinary Research and DevelopmentYash ModiNo ratings yet

- Tokenization 1697136521Document5 pagesTokenization 1697136521Grisha KarunasNo ratings yet

- SSRN Id3517142Document35 pagesSSRN Id3517142Ian KwepuNo ratings yet

- The Utility of Blockchain Technology in Our SocietyDocument9 pagesThe Utility of Blockchain Technology in Our SocietyJeffrey SalasNo ratings yet

- Introductio 1Document16 pagesIntroductio 1Pulkit GeraNo ratings yet

- BlockchainDocument8 pagesBlockchainlintangNo ratings yet

- FINAL The Blockchain Technology (1) - AS - 2019!10!01docxDocument2 pagesFINAL The Blockchain Technology (1) - AS - 2019!10!01docxPanayiotis AntoniadesNo ratings yet

- Three Imperatives For Taxing The Digital Economy: by Kevin Dancey, Chief Executive Officer, IFAC - February 15, 2019Document2 pagesThree Imperatives For Taxing The Digital Economy: by Kevin Dancey, Chief Executive Officer, IFAC - February 15, 2019Đỗ MaiNo ratings yet

- The Future of The Arm's-Length Principle: Lena AngvikDocument5 pagesThe Future of The Arm's-Length Principle: Lena AngvikĐỗ MaiNo ratings yet

- Big Tech Changed Everything For International Tax: Josh WhiteDocument6 pagesBig Tech Changed Everything For International Tax: Josh WhiteĐỗ MaiNo ratings yet

- N0.8 - CIAT's Transfer Pricing "Cocktail" Provides Solutions For Transactional Net Margin Method OveruseDocument5 pagesN0.8 - CIAT's Transfer Pricing "Cocktail" Provides Solutions For Transactional Net Margin Method OveruseĐỗ MaiNo ratings yet

- Dimsey CaseDocument1 pageDimsey CaseĐỗ MaiNo ratings yet

- Cambridge International A Level: Mathematics 9709/32 May/June 2020Document13 pagesCambridge International A Level: Mathematics 9709/32 May/June 2020redwanNo ratings yet

- 4 Breakout, Technical Analysis ScannerDocument4 pages4 Breakout, Technical Analysis ScannerDeepak KansalNo ratings yet

- CP2600-OP, A20 DS 1-0-2 (Cat12 CPE)Document2 pagesCP2600-OP, A20 DS 1-0-2 (Cat12 CPE)hrga hrgaNo ratings yet

- C++ For Safety-Critical SystemsDocument5 pagesC++ For Safety-Critical SystemstestNo ratings yet

- MT6571 Android V2 ScatterDocument5 pagesMT6571 Android V2 ScatteranthonyNo ratings yet

- Qa Tester JDDocument3 pagesQa Tester JDIonutz AsafteiNo ratings yet

- Fireclass Overview Presentation PDFDocument34 pagesFireclass Overview Presentation PDFRamon Mendoza PantojaNo ratings yet

- Bugreport 2015 08 22 22 55 05Document4,142 pagesBugreport 2015 08 22 22 55 05Gelson Raizer AlvesNo ratings yet

- Implementin Iso 12646Document14 pagesImplementin Iso 12646HectorJulianRellosoNuñezNo ratings yet

- Solution Manual For Miller and Freunds P PDFDocument4 pagesSolution Manual For Miller and Freunds P PDFKuttyNo ratings yet

- Neration of Various SignalsDocument5 pagesNeration of Various SignalsPREMKUMAR JOHNNo ratings yet

- Global Work Cell Phone PolicyDocument7 pagesGlobal Work Cell Phone Policyshaquan josephsNo ratings yet

- Essential FVS: A User's Guide To The Forest Vegetation SimulatorDocument244 pagesEssential FVS: A User's Guide To The Forest Vegetation SimulatorherciloodoricoNo ratings yet

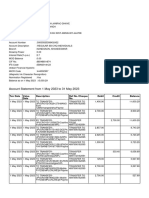

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027No ratings yet

- Chapter 3 Arithmetic For ComputersDocument49 pagesChapter 3 Arithmetic For ComputersicedalbertNo ratings yet

- Templates in Text and Chat - 327d21 PDFDocument3 pagesTemplates in Text and Chat - 327d21 PDFKRYSTEL WENDY LAHOMNo ratings yet

- Ajp 13Document6 pagesAjp 13Ganesh EkambeNo ratings yet

- Etec 404Document11 pagesEtec 404Akhilesh ChaudhryNo ratings yet

- IMBA Courses For Fall 2018Document1 pageIMBA Courses For Fall 2018Indrajeet BarveNo ratings yet

- Sunil Chandra: Career ObjectiveDocument3 pagesSunil Chandra: Career ObjectiveAnonymous yGyIJSNo ratings yet

- Logcat Prev CSC LogDocument278 pagesLogcat Prev CSC LogDarkzin ProNo ratings yet

- RGB Color Codes ChartDocument6 pagesRGB Color Codes ChartHermawan UsNo ratings yet

- 3D Metrology: Forth Dimension DisplaysDocument4 pages3D Metrology: Forth Dimension DisplaysNathan DrakeNo ratings yet

- BJTDocument23 pagesBJTEd JudgeNo ratings yet