You might also like

- Time Value of Money: Brooks, (2013) Chapters 3, 4Document49 pagesTime Value of Money: Brooks, (2013) Chapters 3, 4DiannaNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- A N D Haksar Glimpses of Sanskrit Literature 1995Document286 pagesA N D Haksar Glimpses of Sanskrit Literature 1995anjaliNo ratings yet

- An MBA in a Book: Everything You Need to Know to Master Business - In One Book!From EverandAn MBA in a Book: Everything You Need to Know to Master Business - In One Book!No ratings yet

- LONG TERM INVESTMENT DECISIONS: TIME VALUE OF MONEY (TVM) REPORTDocument7 pagesLONG TERM INVESTMENT DECISIONS: TIME VALUE OF MONEY (TVM) REPORTMary Ann MarianoNo ratings yet

- List of UK Banks from Bank of England as of May 3rd 2022Document6 pagesList of UK Banks from Bank of England as of May 3rd 2022Javier JiménezNo ratings yet

- Concepts of Value and ReturnDocument38 pagesConcepts of Value and Returnravi anandNo ratings yet

- R05 Time Value of Money IFT Notes PDFDocument28 pagesR05 Time Value of Money IFT Notes PDFAbbas0% (1)

- Lecture 3 - Time Value of MoneyDocument22 pagesLecture 3 - Time Value of MoneyJason LuximonNo ratings yet

- Chapter 4 SolutionsDocument14 pagesChapter 4 Solutionshassan.murad82% (11)

- Finman Modules Chapter 5Document9 pagesFinman Modules Chapter 5Angel ColarteNo ratings yet

- A Project Report On Employees Satisfaction Regarding HDFC BankDocument77 pagesA Project Report On Employees Satisfaction Regarding HDFC Bankvarun_bawa25191578% (23)

- Learning Packet 5 Time Value of MoneyDocument10 pagesLearning Packet 5 Time Value of MoneyPrincess Marie BaldoNo ratings yet

- Module 2 Time Value of MoneyDocument42 pagesModule 2 Time Value of MoneyNani MadhavNo ratings yet

- Module 2 Time Value of Money (1)Document42 pagesModule 2 Time Value of Money (1)rishabsingh2322No ratings yet

- Time Value of Money handoutDocument12 pagesTime Value of Money handoutNipun SathsaraNo ratings yet

- The Time Value of MoneyDocument75 pagesThe Time Value of MoneySanchit AroraNo ratings yet

- Concepts of Value and ReturnDocument38 pagesConcepts of Value and ReturnVaishnav KumarNo ratings yet

- CH 02 Revised Financial Management by IM PandeyDocument38 pagesCH 02 Revised Financial Management by IM PandeyAnjan Kumar100% (6)

- Mathematics For FinanceDocument12 pagesMathematics For FinanceAbhishek PrabhakarNo ratings yet

- Corporate Finance: Time Value of MoneyDocument33 pagesCorporate Finance: Time Value of Moneykamiya_rautelaNo ratings yet

- Chapter 6 Time Value of MoneyDocument39 pagesChapter 6 Time Value of Moneyjhogonnath.saha.65No ratings yet

- Financial Management Time Value of MoneyDocument13 pagesFinancial Management Time Value of MoneyNoelia Mc DonaldNo ratings yet

- Unit 2Document13 pagesUnit 2anas khanNo ratings yet

- CH - 02 - Time Value of MoneyDocument38 pagesCH - 02 - Time Value of MoneyAlwin SebastianNo ratings yet

- Time Value of Money and Return CalculationsDocument38 pagesTime Value of Money and Return Calculationskhushi vaswaniNo ratings yet

- Engineering Economy: Chapter 3: The Time Value of MoneyDocument32 pagesEngineering Economy: Chapter 3: The Time Value of MoneyAhmad Medlej100% (1)

- Module 1 - Time Value of Money Handout For LMS 2020Document8 pagesModule 1 - Time Value of Money Handout For LMS 2020sandeshNo ratings yet

- Chapte R: Value and ReturnDocument38 pagesChapte R: Value and Returnkhushi vaswaniNo ratings yet

- Time Value of MoneyDocument47 pagesTime Value of MoneyPrashant JhakarwarNo ratings yet

- Chap-2-Concepts of Value & Return Managerial FinanceDocument12 pagesChap-2-Concepts of Value & Return Managerial FinanceSoham Savjani100% (2)

- Study Material For Corporate FinanceDocument62 pagesStudy Material For Corporate FinanceAnant JainNo ratings yet

- Financial Management MCQ and ConceptsDocument8 pagesFinancial Management MCQ and Conceptsmohanraokp2279No ratings yet

- R06 Time Value of Money 2017 Level I Notes: WWW - Ift.worldDocument22 pagesR06 Time Value of Money 2017 Level I Notes: WWW - Ift.worldtataNo ratings yet

- Chapter 04 (Final Energy Financial Management)Document19 pagesChapter 04 (Final Energy Financial Management)rathneshkumarNo ratings yet

- CH 02 RevisedDocument38 pagesCH 02 RevisedZia AhmadNo ratings yet

- FinaMan Final TermDocument15 pagesFinaMan Final TermHANNAH ROSS BAELNo ratings yet

- Time Value of MoneyDocument21 pagesTime Value of MoneyNikhil PatilNo ratings yet

- Financial Management Merge NotesDocument145 pagesFinancial Management Merge NotesDoan Ngoc Quynh TienNo ratings yet

- Time Value of MoneyDocument4 pagesTime Value of MoneyTshireletso MphaneNo ratings yet

- Introduction to Financial Modeling BasicsDocument5 pagesIntroduction to Financial Modeling Basicsleul habtamuNo ratings yet

- 302time Value of MoneyDocument69 pages302time Value of MoneypujaadiNo ratings yet

- FA-I CHAPTER FIVE@editedDocument23 pagesFA-I CHAPTER FIVE@editedHussen AbdulkadirNo ratings yet

- FM Unit 4 Lecture Notes - Time Value of MoneyDocument4 pagesFM Unit 4 Lecture Notes - Time Value of MoneyDebbie DebzNo ratings yet

- Math 012 g5 Simple Annnuities 094300Document5 pagesMath 012 g5 Simple Annnuities 094300jbiventotabwNo ratings yet

- Planning and Evaluationl English 4Document40 pagesPlanning and Evaluationl English 4Absa TraderNo ratings yet

- Time Value of Money - TheoryDocument7 pagesTime Value of Money - TheoryNahidul Islam IUNo ratings yet

- Time Value of Money Notes Loan ArmotisationDocument12 pagesTime Value of Money Notes Loan ArmotisationVimbai ChituraNo ratings yet

- Capital Budgeting: Overview: Multiperiod Decision-MakingDocument3 pagesCapital Budgeting: Overview: Multiperiod Decision-MakingckalechaNo ratings yet

- SLM Unit 03 Mbf201Document21 pagesSLM Unit 03 Mbf201Pankaj KumarNo ratings yet

- A Research Paper Presented in Partial Fulfillment of The Requirements For The Course Financial ManagementDocument14 pagesA Research Paper Presented in Partial Fulfillment of The Requirements For The Course Financial ManagementMIEL ALLAN P. GABRIELNo ratings yet

- Bond ValuationDocument35 pagesBond ValuationVijay SinghNo ratings yet

- Topic Review 6 The Time Value of MoneyDocument3 pagesTopic Review 6 The Time Value of MoneyVonreev OntoyNo ratings yet

- 3.time Value of Money..F.MDocument21 pages3.time Value of Money..F.MMarl MwegiNo ratings yet

- Interest Rates and Exchange RatesDocument5 pagesInterest Rates and Exchange RatesPutriNo ratings yet

- 304A Financial Management and Decision MakingDocument67 pages304A Financial Management and Decision MakingSam SamNo ratings yet

- Corporate Finance 1a Time Value for MoneyDocument16 pagesCorporate Finance 1a Time Value for MoneyKIMBERLY MUKAMBANo ratings yet

- Civil Engineering Construction and Graphics QUIZ#02 Topic:: Difference Between Simple and Compound InterestDocument14 pagesCivil Engineering Construction and Graphics QUIZ#02 Topic:: Difference Between Simple and Compound InteresttayyabNo ratings yet

- 3353 TVM Lecture 3Document31 pages3353 TVM Lecture 3herueuxNo ratings yet

- 3b5a3lecture 3 Time Value of MoneyDocument34 pages3b5a3lecture 3 Time Value of MoneyApril MartinezNo ratings yet

- Financial Mathematicg CT 1Document320 pagesFinancial Mathematicg CT 1janekhanNo ratings yet

- NOTES ON TIME VALUE OF MONEYDocument10 pagesNOTES ON TIME VALUE OF MONEYFariya HossainNo ratings yet

- Addiction 101Document5 pagesAddiction 101anjaliNo ratings yet

- Split in The Nationalist Congress Party (NCP) Was Another "Googly"Document3 pagesSplit in The Nationalist Congress Party (NCP) Was Another "Googly"anjaliNo ratings yet

- Split in The Nationalist Congress Party (NCP) Was Another "Googly"Document3 pagesSplit in The Nationalist Congress Party (NCP) Was Another "Googly"anjaliNo ratings yet

- Addiction 101Document5 pagesAddiction 101anjaliNo ratings yet

- Split in The Nationalist Congress Party (NCP) Was Another "Googly"Document3 pagesSplit in The Nationalist Congress Party (NCP) Was Another "Googly"anjaliNo ratings yet

- Split in The Nationalist Congress Party (NCP) Was Another "Googly"Document3 pagesSplit in The Nationalist Congress Party (NCP) Was Another "Googly"anjaliNo ratings yet

- Eviews Guía IDocument945 pagesEviews Guía IWendy Ortiz HurtadoNo ratings yet

- Tr.. - C"'-C TT V/: Unit 56Document7 pagesTr.. - C"'-C TT V/: Unit 56anjaliNo ratings yet

- Split in The Nationalist Congress Party (NCP) Was Another "Googly"Document3 pagesSplit in The Nationalist Congress Party (NCP) Was Another "Googly"anjaliNo ratings yet

- Lecture 3 - Functional Forms of Linear Regression Models - Double Log ModelDocument19 pagesLecture 3 - Functional Forms of Linear Regression Models - Double Log ModelanjaliNo ratings yet

- Split in The Nationalist Congress Party (NCP) Was Another "Googly"Document3 pagesSplit in The Nationalist Congress Party (NCP) Was Another "Googly"anjaliNo ratings yet

- Split in The Nationalist Congress Party (NCP) Was Another "Googly"Document3 pagesSplit in The Nationalist Congress Party (NCP) Was Another "Googly"anjaliNo ratings yet

- Theory Corporate BondDocument19 pagesTheory Corporate BondanjaliNo ratings yet

- Lecture 5 - Functional Forms of Linear Regression Models - Lin-Log ModelDocument6 pagesLecture 5 - Functional Forms of Linear Regression Models - Lin-Log ModelanjaliNo ratings yet

- Lecture 4 - Functional Forms of Linear Regression Models - Log Lin ModelDocument16 pagesLecture 4 - Functional Forms of Linear Regression Models - Log Lin ModelanjaliNo ratings yet

- Lecture 6 - Functional Forms of Linear Regression Models - Reciprocal ModelDocument11 pagesLecture 6 - Functional Forms of Linear Regression Models - Reciprocal ModelanjaliNo ratings yet

- Population: One-Child Policy China PopulationDocument7 pagesPopulation: One-Child Policy China PopulationanjaliNo ratings yet

- Lecture 3 - Functional Forms of Linear Regression Models - Double Log ModelDocument19 pagesLecture 3 - Functional Forms of Linear Regression Models - Double Log ModelanjaliNo ratings yet

- Chapter 8 Time Value of Money - SolutionDocument7 pagesChapter 8 Time Value of Money - SolutionanjaliNo ratings yet

- Lecture 5 - Functional Forms of Linear Regression Models - Lin-Log ModelDocument6 pagesLecture 5 - Functional Forms of Linear Regression Models - Lin-Log ModelanjaliNo ratings yet

- ECONOMETRICS PPT (Shivali and Deepali)Document30 pagesECONOMETRICS PPT (Shivali and Deepali)anjaliNo ratings yet

- Lecture 4 - Functional Forms of Linear Regression Models - Log Lin ModelDocument16 pagesLecture 4 - Functional Forms of Linear Regression Models - Log Lin ModelanjaliNo ratings yet

- (Variables) Life Insurance and The Macroeconomy - Indian ExperienceDocument6 pages(Variables) Life Insurance and The Macroeconomy - Indian ExperienceanjaliNo ratings yet

- Life insurance premiums and inflation rates in India from 2001-2018Document7 pagesLife insurance premiums and inflation rates in India from 2001-2018anjaliNo ratings yet

- Indian Eco Research PaperDocument5 pagesIndian Eco Research PaperanjaliNo ratings yet

- Asian Financial CrisisDocument24 pagesAsian Financial CrisisanjaliNo ratings yet

- Impact of Covid-19 On Data and Analytics For Life Insurance IndustryDocument13 pagesImpact of Covid-19 On Data and Analytics For Life Insurance IndustryanjaliNo ratings yet

- (Variables) Life Insurance Business in India - Analysis of PerformanceDocument9 pages(Variables) Life Insurance Business in India - Analysis of PerformanceanjaliNo ratings yet

- Advanced Accounting Principles ModulesDocument2 pagesAdvanced Accounting Principles ModulesAnamika VatsaNo ratings yet

- SIP-Shape by AMFI PDFDocument60 pagesSIP-Shape by AMFI PDFBiresh SalujaNo ratings yet

- Accounting Oral ExamDocument5 pagesAccounting Oral ExamalmmuuhNo ratings yet

- Fabm3 M3Document23 pagesFabm3 M3Jolina GabaynoNo ratings yet

- RTP May 2018 New Gr1Document122 pagesRTP May 2018 New Gr1subhanvts7781No ratings yet

- Application For Margin Money Loan To S.S.I. Units Promoted by Non-Resident Keralites From The Government of Kerala PDFDocument6 pagesApplication For Margin Money Loan To S.S.I. Units Promoted by Non-Resident Keralites From The Government of Kerala PDFdasuyaNo ratings yet

- Sbiepay Sbiepay: Neft Challan (No RTGS) Neft Challan (No RTGS)Document1 pageSbiepay Sbiepay: Neft Challan (No RTGS) Neft Challan (No RTGS)jairaj DTWNo ratings yet

- User List - Pages Sneat - Bootstrap 5 HTML Admin Template - ProDocument4 pagesUser List - Pages Sneat - Bootstrap 5 HTML Admin Template - ProNaga BonarNo ratings yet

- Nanyang Business School AB1201 Financial Management Tutorial 2: Time Value of Money (Common Questions)Document7 pagesNanyang Business School AB1201 Financial Management Tutorial 2: Time Value of Money (Common Questions)asdsadsaNo ratings yet

- ISRS 4400 Case BookDocument6 pagesISRS 4400 Case BookSaadat AkhundNo ratings yet

- Advantage of M-CommerceDocument5 pagesAdvantage of M-CommerceJiju JustinNo ratings yet

- Reading 25 Non-Current (Long-Term) LiabilitiesDocument18 pagesReading 25 Non-Current (Long-Term) LiabilitiesARPIT ARYANo ratings yet

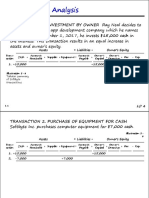

- Transaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToDocument31 pagesTransaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToSophia LocreNo ratings yet

- Updates On HDMF Housing Loan Program: Juanito V. Eje Task Force Head Business Development SectorDocument28 pagesUpdates On HDMF Housing Loan Program: Juanito V. Eje Task Force Head Business Development SectorcehsscehlNo ratings yet

- Universiti Teknologi Mara Final Examination: This Examination Paper Consists of 6 Printed PagesDocument6 pagesUniversiti Teknologi Mara Final Examination: This Examination Paper Consists of 6 Printed PagesAnisah NiesNo ratings yet

- 2nd Year Principles of Accounting Guess Paper 2023 Zahid NotesDocument5 pages2nd Year Principles of Accounting Guess Paper 2023 Zahid Notesashfaq4985No ratings yet

- WestpacDocument3 pagesWestpacJalal UddinNo ratings yet

- Govt. of West Bengal Transport Department Grips Echallan: (Identifiction No)Document1 pageGovt. of West Bengal Transport Department Grips Echallan: (Identifiction No)Monojit MondalNo ratings yet

- ABC - PFRS 3 Final Exam ReviewDocument17 pagesABC - PFRS 3 Final Exam ReviewCristel TannaganNo ratings yet

- FRM Test 03 - Topic - TVM + Mutual FundsDocument20 pagesFRM Test 03 - Topic - TVM + Mutual FundsKamal BhatiaNo ratings yet

- EF3442 Intermediate MicroeconomicsDocument6 pagesEF3442 Intermediate MicroeconomicsAshtar Ali Bangash100% (1)

- Survey QuestionDocument3 pagesSurvey QuestionAngelica Joy Daiz GuceNo ratings yet

- Total Monthly Income and Expenses BreakdownDocument43 pagesTotal Monthly Income and Expenses BreakdownpachukumarNo ratings yet

- Traveleasy LTD Management Accounts Profit and Loss StatementDocument5 pagesTraveleasy LTD Management Accounts Profit and Loss StatementSitakanta AcharyaNo ratings yet

- Solved From The Trial Balance of Girtie Lillis Attorney at Law Given inDocument1 pageSolved From The Trial Balance of Girtie Lillis Attorney at Law Given inAnbu jaromiaNo ratings yet

- Doupnik 6e Chap011 PPT Accessible GM OutputDocument55 pagesDoupnik 6e Chap011 PPT Accessible GM Outputhasan jabrNo ratings yet

- Interest Rates and Currency SwapsDocument24 pagesInterest Rates and Currency SwapsQuoc AnhNo ratings yet

- Prelim Exam-Boticario D. (AST)Document4 pagesPrelim Exam-Boticario D. (AST)Dominic E. BoticarioNo ratings yet