You might also like

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Compre 2 - Far1Document5 pagesCompre 2 - Far1Mary Alyssa Claire Capate IINo ratings yet

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- CPA - Quizbowl 2008Document10 pagesCPA - Quizbowl 2008frankreedh100% (3)

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

- Assessment Test 2nd Cash&RecDocument6 pagesAssessment Test 2nd Cash&RecMellowNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- 1st Long Exam (Summer 2022) WITHOUT ANSWERDocument10 pages1st Long Exam (Summer 2022) WITHOUT ANSWERDaphnie Kitch CatotalNo ratings yet

- Accounting 101 FinalsDocument16 pagesAccounting 101 FinalsDanilo Diniay Jr100% (1)

- Holy Cross College: B. Cause and EffectDocument12 pagesHoly Cross College: B. Cause and EffectSam VeraNo ratings yet

- Intermediate Accounting 1Document12 pagesIntermediate Accounting 1Walter Peralta100% (1)

- Trade and Other Receivables (IA)Document6 pagesTrade and Other Receivables (IA)pcdesktop.brarNo ratings yet

- Acc05 Take Home Quiz Cash and ReceivablesDocument12 pagesAcc05 Take Home Quiz Cash and ReceivablesJullia BelgicaNo ratings yet

- Accounts ReceivableDocument11 pagesAccounts Receivablesarahbee89% (9)

- Bsa 1201-Financial Accounting and Reporting Preliminary Departmental Exam Reviewer Topic CoverageDocument15 pagesBsa 1201-Financial Accounting and Reporting Preliminary Departmental Exam Reviewer Topic CoverageChjxksjsgskNo ratings yet

- Level Three Theory (Knowledge) ChoiceDocument17 pagesLevel Three Theory (Knowledge) ChoiceYaa Rabbii100% (1)

- Final Exam Fundamentals of AccountingDocument7 pagesFinal Exam Fundamentals of AccountingdumpanonymouslyNo ratings yet

- Pre-Quali - 2016 - Financial - Acctg. - Level - 1 - Answers - Docx Filename UTF-8''Pre-quali 2016 Financial Acctg. (Level 1) - AnswersDocument10 pagesPre-Quali - 2016 - Financial - Acctg. - Level - 1 - Answers - Docx Filename UTF-8''Pre-quali 2016 Financial Acctg. (Level 1) - AnswersReve Joy Eco IsagaNo ratings yet

- Theory (1) 1Document18 pagesTheory (1) 1Debela RegasaNo ratings yet

- ACC 122 General Review - AKDocument11 pagesACC 122 General Review - AKJaselle SanchezNo ratings yet

- Diskusi Mid Test - Meeting 7Document26 pagesDiskusi Mid Test - Meeting 7Jimmy LimNo ratings yet

- Level Three Theory (Knowledge) Choice: C. Journalizing - Posting - Trial Balance - Financial StatementsDocument17 pagesLevel Three Theory (Knowledge) Choice: C. Journalizing - Posting - Trial Balance - Financial Statementseferem0% (1)

- Level 3 TheoryDocument19 pagesLevel 3 TheoryMarta GobenaNo ratings yet

- Choice 1-1Document17 pagesChoice 1-1Dagnachew WeldegebrielNo ratings yet

- AC503 - Finals Reviewer 2Document10 pagesAC503 - Finals Reviewer 2Ashley Levy San PedroNo ratings yet

- Reviewer (Cash-Accounts Receivable)Document5 pagesReviewer (Cash-Accounts Receivable)Camila Mae AlduezaNo ratings yet

- Problem Solving (With Answers)Document12 pagesProblem Solving (With Answers)sunflower100% (1)

- Exercise Receivables 1Document8 pagesExercise Receivables 1Asyraf AzharNo ratings yet

- Pilot TestDocument5 pagesPilot Testkhanhhung1112004No ratings yet

- Financial AccountingDocument5 pagesFinancial Accountingimsana minatozakiNo ratings yet

- Conceptual Framework and Accounting StandardsDocument11 pagesConceptual Framework and Accounting StandardsAngela TalastasNo ratings yet

- Polytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsDocument15 pagesPolytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsYassi CurtisNo ratings yet

- Accounts Receivables: TheoriesDocument5 pagesAccounts Receivables: TheoriesshellacregenciaNo ratings yet

- FAR 2 Answer KeyDocument5 pagesFAR 2 Answer KeyMary Rose VillamorNo ratings yet

- BFAR Qualifying Exam ReviewerDocument18 pagesBFAR Qualifying Exam ReviewerHappy MagdangalNo ratings yet

- Week 2Document6 pagesWeek 2Maryane AngelaNo ratings yet

- Mock Departmental Part 1Document7 pagesMock Departmental Part 1Mikee RizonNo ratings yet

- ACCTG102 MidtermQ1.5 Cash Make Up ExamDocument6 pagesACCTG102 MidtermQ1.5 Cash Make Up ExamBarrylou Manayan100% (1)

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument6 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionAIENNA GABRIELLE FABRO100% (1)

- Accounting Hawk - FAR - Incoming 3rd and 4th YearDocument27 pagesAccounting Hawk - FAR - Incoming 3rd and 4th YearClaire BarbaNo ratings yet

- Quiz On RizalDocument14 pagesQuiz On RizalYorinNo ratings yet

- ACCTG102 Midterm ExaminationDocument9 pagesACCTG102 Midterm ExaminationJimbo Manalastas100% (1)

- 1styr - 1stMT - Intermediate Accounting 1 - 2223Document35 pages1styr - 1stMT - Intermediate Accounting 1 - 2223angelpaulenebeatricemNo ratings yet

- Quiz 2 - Corp Liqui and Installment SalesDocument8 pagesQuiz 2 - Corp Liqui and Installment SalesKenneth Christian WilburNo ratings yet

- Basic Accounting Final ExamDocument7 pagesBasic Accounting Final ExamCharmae Agan Caroro75% (4)

- Pilot TestDocument4 pagesPilot TestTrang Nguyễn QuỳnhNo ratings yet

- Chapter 61Document7 pagesChapter 61Jay PaleroNo ratings yet

- Financial Accounting and ReportingDocument26 pagesFinancial Accounting and ReportingJanaela89% (45)

- CASH TO ACCRUAL SINGLE ENTRY With ANSWERSDocument8 pagesCASH TO ACCRUAL SINGLE ENTRY With ANSWERSRaven SiaNo ratings yet

- Cup 2 (Far)Document8 pagesCup 2 (Far)Chan DagaleNo ratings yet

- Midterm Examination Suggested AnswersDocument9 pagesMidterm Examination Suggested AnswersJoshua CaraldeNo ratings yet

- IA1 - 1st Mock Quiz (With Suggested Answers)Document6 pagesIA1 - 1st Mock Quiz (With Suggested Answers)Rogienel ReyesNo ratings yet

- Midterm Quiz No. 1 - Multiple ChoicesDocument5 pagesMidterm Quiz No. 1 - Multiple ChoicesRonel CaagbayNo ratings yet

- Intermediate Accounting 1 Final Grading ExaminationDocument18 pagesIntermediate Accounting 1 Final Grading ExaminationKrissa Mae LongosNo ratings yet

- Intermediate Accounting 1 Final Grading ExaminationDocument18 pagesIntermediate Accounting 1 Final Grading ExaminationRena Rose Malunes11% (9)

- ACC100.101 Preliminary Examination - For PostingDocument5 pagesACC100.101 Preliminary Examination - For PostingRAMOS, Aliyah Faith P.No ratings yet

- Contest Basic AccountingDocument9 pagesContest Basic AccountingJin Hee MarasiganNo ratings yet

- Acca Fa Trial - Exam - 1 - QuestionsDocument18 pagesAcca Fa Trial - Exam - 1 - QuestionsElshan ShahverdiyevNo ratings yet

- 6th Practice Qs 99.2Document3 pages6th Practice Qs 99.2BromanineNo ratings yet

- Final Round QuestionsDocument8 pagesFinal Round QuestionsShenne MinglanaNo ratings yet

- SHS ModulesDocument13 pagesSHS ModulesJecca JamonNo ratings yet

- Payment of The InvoiceDocument14 pagesPayment of The InvoiceJecca JamonNo ratings yet

- Book of AccountsDocument24 pagesBook of AccountsJecca JamonNo ratings yet

- M M M M: Markup, Markdown, and Gross MarginDocument10 pagesM M M M: Markup, Markdown, and Gross MarginJecca JamonNo ratings yet

- Production and Operations ManagementDocument284 pagesProduction and Operations Managementsnehal.deshmukh89% (28)

- Review of Related LiteratureDocument15 pagesReview of Related LiteratureJecca JamonNo ratings yet

- Death of The ApostlesDocument22 pagesDeath of The ApostlesJecca JamonNo ratings yet

- Module 3: FRISBEE: Intended Learning OutcomesDocument19 pagesModule 3: FRISBEE: Intended Learning OutcomesJecca Jamon100% (1)

- Conflict and NegotiationDocument24 pagesConflict and NegotiationJecca JamonNo ratings yet

- The Life of William CareyDocument14 pagesThe Life of William CareyJecca JamonNo ratings yet

- Module 4. Dances. PE104Document20 pagesModule 4. Dances. PE104Jecca JamonNo ratings yet

- Test Bank Law 1 CparDocument26 pagesTest Bank Law 1 CparJoyce Kay Azucena73% (22)

- Futsal Pe104Document63 pagesFutsal Pe104Jecca JamonNo ratings yet

- INTRO - Your Walk and Your Work For ChristDocument21 pagesINTRO - Your Walk and Your Work For ChristJecca JamonNo ratings yet

- Help MeDocument29 pagesHelp MeJecca JamonNo ratings yet

- AIS - Chapter 1Document41 pagesAIS - Chapter 1Lailing DavidNo ratings yet

- Chapter 01 - Business CombinationsDocument17 pagesChapter 01 - Business CombinationsTina LundstromNo ratings yet

- Standard Costing 2 PDFDocument59 pagesStandard Costing 2 PDFMariver LlorenteNo ratings yet

- BiodiversityDocument17 pagesBiodiversityJecca JamonNo ratings yet

- M-H Chapter 12Document33 pagesM-H Chapter 12Jecca JamonNo ratings yet

- AIS6e ch03Document50 pagesAIS6e ch03Jecca JamonNo ratings yet

- Basic Accounting Financial AnalysisDocument439 pagesBasic Accounting Financial AnalysisBuilding Substance PodNo ratings yet

- DCB Benefit Savings AccountDocument2 pagesDCB Benefit Savings AccountDesikanNo ratings yet

- Chapter 10 Shareholders EquityDocument10 pagesChapter 10 Shareholders EquityMarine De CocquéauNo ratings yet

- ReiceivablesDocument27 pagesReiceivablesrivaceline100% (3)

- ACC106Document7 pagesACC106NajihahSyahiraNo ratings yet

- Accounts PayableDocument102 pagesAccounts PayableAtilaUnorteNo ratings yet

- Long-Term Construction Contracts & FranchiseDocument6 pagesLong-Term Construction Contracts & FranchiseBryan ReyesNo ratings yet

- ACCOUNTING 14-07 - APPLIED AUDITING Departmental With AnswerDocument9 pagesACCOUNTING 14-07 - APPLIED AUDITING Departmental With AnswerkylacerroNo ratings yet

- TOA StarDocument11 pagesTOA StarFaith GuballaNo ratings yet

- CH 2Document4 pagesCH 2ايهاب غزالةNo ratings yet

- Accountancy: Class: XiDocument8 pagesAccountancy: Class: XiSanskarNo ratings yet

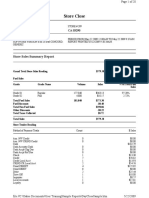

- Store Close: Store Sales Summary ReportDocument20 pagesStore Close: Store Sales Summary ReportJimmyNo ratings yet

- FA1 NotesDocument270 pagesFA1 NotesNida KhanNo ratings yet

- Electronic Cash/Credit Ledgers and Liability Register in GSTDocument2 pagesElectronic Cash/Credit Ledgers and Liability Register in GSTRohit BajpaiNo ratings yet

- CH 19-Answers To Textbook Ques 1025243368Document4 pagesCH 19-Answers To Textbook Ques 1025243368ayten.ayman.eleraky100% (1)

- (EXCEL) Dianita Safitri - 7193220005Document26 pages(EXCEL) Dianita Safitri - 7193220005Jack WilisNo ratings yet

- Acccob 2 Lecture 2 Cash and Cash Equivalents T2ay2021Document7 pagesAcccob 2 Lecture 2 Cash and Cash Equivalents T2ay2021Rey HandumonNo ratings yet

- Ch10 Current Liabilities and PayrollDocument48 pagesCh10 Current Liabilities and PayrollchuchuNo ratings yet

- Qa Ca Zambia Programme December 2019 ExaminationDocument449 pagesQa Ca Zambia Programme December 2019 ExaminationimasikudenisiahNo ratings yet

- Aug2010Document4 pagesAug2010Mohd ShoaibNo ratings yet

- 2.reverse Charge MechanismDocument66 pages2.reverse Charge MechanismchariNo ratings yet

- Adjusting Entries NotesDocument19 pagesAdjusting Entries NotesAnnika TrishaNo ratings yet

- FB60 - InvoiceDocument5 pagesFB60 - Invoiceadit1435No ratings yet

- Bank Reconciliation ReviewerDocument2 pagesBank Reconciliation Reviewerfred ferrera jrNo ratings yet

- Dwnload Full College Accounting A Practical Approach 13th Edition Jeffrey Slater Test Bank PDFDocument36 pagesDwnload Full College Accounting A Practical Approach 13th Edition Jeffrey Slater Test Bank PDFraisable.maugerg07jpg100% (11)

- Albka Lkyltvkc NU8Document4 pagesAlbka Lkyltvkc NU8mfsiNo ratings yet

- Accounting and Book Keeping NotesDocument15 pagesAccounting and Book Keeping NotesWesley SangNo ratings yet

- Study On Foreign Exchange Remittances & Interbank DealingsDocument95 pagesStudy On Foreign Exchange Remittances & Interbank DealingsSachin KajaveNo ratings yet

- Common Accounting SystemDocument23 pagesCommon Accounting SystemNayan DemlaniNo ratings yet

- ENTREP 2020 Financial PlanDocument36 pagesENTREP 2020 Financial PlanAndrea Jane FaustinoNo ratings yet

- Summary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedFrom EverandSummary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedRating: 5 out of 5 stars5/5 (80)

- Summary of 10x Is Easier than 2x: How World-Class Entrepreneurs Achieve More by Doing Less by Dan Sullivan & Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisFrom EverandSummary of 10x Is Easier than 2x: How World-Class Entrepreneurs Achieve More by Doing Less by Dan Sullivan & Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisRating: 4.5 out of 5 stars4.5/5 (23)

- The Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeFrom EverandThe Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeRating: 4.5 out of 5 stars4.5/5 (2)

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeFrom EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeRating: 4.5 out of 5 stars4.5/5 (88)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- Summary: Trading in the Zone: Trading in the Zone: Master the Market with Confidence, Discipline, and a Winning Attitude by Mark Douglas: Key Takeaways, Summary & AnalysisFrom EverandSummary: Trading in the Zone: Trading in the Zone: Master the Market with Confidence, Discipline, and a Winning Attitude by Mark Douglas: Key Takeaways, Summary & AnalysisRating: 5 out of 5 stars5/5 (15)

- Summary: The Gap and the Gain: The High Achievers' Guide to Happiness, Confidence, and Success by Dan Sullivan and Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisFrom EverandSummary: The Gap and the Gain: The High Achievers' Guide to Happiness, Confidence, and Success by Dan Sullivan and Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisRating: 5 out of 5 stars5/5 (4)

- Baby Steps Millionaires: How Ordinary People Built Extraordinary Wealth--and How You Can TooFrom EverandBaby Steps Millionaires: How Ordinary People Built Extraordinary Wealth--and How You Can TooRating: 5 out of 5 stars5/5 (323)

- Broken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterFrom EverandBroken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterRating: 5 out of 5 stars5/5 (1)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Financial Intelligence: How to To Be Smart with Your Money and Your LifeFrom EverandFinancial Intelligence: How to To Be Smart with Your Money and Your LifeRating: 4.5 out of 5 stars4.5/5 (540)

- Sleep And Grow Rich: Guided Sleep Meditation with Affirmations For Wealth & AbundanceFrom EverandSleep And Grow Rich: Guided Sleep Meditation with Affirmations For Wealth & AbundanceRating: 4.5 out of 5 stars4.5/5 (105)

- The 4 Laws of Financial Prosperity: Get Conrtol of Your Money Now!From EverandThe 4 Laws of Financial Prosperity: Get Conrtol of Your Money Now!Rating: 5 out of 5 stars5/5 (388)

- Summary of I Will Teach You to Be Rich: No Guilt. No Excuses. Just a 6-Week Program That Works by Ramit SethiFrom EverandSummary of I Will Teach You to Be Rich: No Guilt. No Excuses. Just a 6-Week Program That Works by Ramit SethiRating: 4.5 out of 5 stars4.5/5 (23)

- Where the Money Is: Value Investing in the Digital AgeFrom EverandWhere the Money Is: Value Investing in the Digital AgeRating: 4.5 out of 5 stars4.5/5 (41)

- Rich Bitch: A Simple 12-Step Plan for Getting Your Financial Life Together . . . FinallyFrom EverandRich Bitch: A Simple 12-Step Plan for Getting Your Financial Life Together . . . FinallyRating: 4 out of 5 stars4/5 (8)

- The Holy Grail of Investing: The World's Greatest Investors Reveal Their Ultimate Strategies for Financial FreedomFrom EverandThe Holy Grail of Investing: The World's Greatest Investors Reveal Their Ultimate Strategies for Financial FreedomRating: 5 out of 5 stars5/5 (7)

- Bitter Brew: The Rise and Fall of Anheuser-Busch and America's Kings of BeerFrom EverandBitter Brew: The Rise and Fall of Anheuser-Busch and America's Kings of BeerRating: 4 out of 5 stars4/5 (52)

- Passive Income Ideas for Beginners: 13 Passive Income Strategies Analyzed, Including Amazon FBA, Dropshipping, Affiliate Marketing, Rental Property Investing and MoreFrom EverandPassive Income Ideas for Beginners: 13 Passive Income Strategies Analyzed, Including Amazon FBA, Dropshipping, Affiliate Marketing, Rental Property Investing and MoreRating: 4.5 out of 5 stars4.5/5 (165)

- Summary: Traction: Get a Grip on Your Business: by Gino Wickman: Key Takeaways, Summary, and AnalysisFrom EverandSummary: Traction: Get a Grip on Your Business: by Gino Wickman: Key Takeaways, Summary, and AnalysisRating: 5 out of 5 stars5/5 (10)

- Rich Dad Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do NotFrom EverandRich Dad Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do NotNo ratings yet

- Fluke: Chance, Chaos, and Why Everything We Do MattersFrom EverandFluke: Chance, Chaos, and Why Everything We Do MattersRating: 4.5 out of 5 stars4.5/5 (19)

- A Happy Pocket Full of Money: Your Quantum Leap Into The Understanding, Having And Enjoying Of Immense Abundance And HappinessFrom EverandA Happy Pocket Full of Money: Your Quantum Leap Into The Understanding, Having And Enjoying Of Immense Abundance And HappinessRating: 5 out of 5 stars5/5 (158)

- The Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeFrom EverandThe Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeRating: 4.5 out of 5 stars4.5/5 (58)

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationFrom EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationRating: 4 out of 5 stars4/5 (11)