You might also like

- G.R. No. 127105. June 25, 1999. Commissioner of Internal Revenue, Petitioner, vs. S.C. Johnson and Son, Inc., and Court of APPEALS, RespondentsDocument5 pagesG.R. No. 127105. June 25, 1999. Commissioner of Internal Revenue, Petitioner, vs. S.C. Johnson and Son, Inc., and Court of APPEALS, RespondentsConcepcion Mallari GarinNo ratings yet

- Republic of The Philippines Quezon City: Court AppealsDocument38 pagesRepublic of The Philippines Quezon City: Court AppealsHerzl Hali V. HermosaNo ratings yet

- International Negotiation-Negotiator's Diary by Siqi LIDocument9 pagesInternational Negotiation-Negotiator's Diary by Siqi LISiqi LINo ratings yet

- ITax Baniqued I and IIDocument25 pagesITax Baniqued I and IIHailin QuintosNo ratings yet

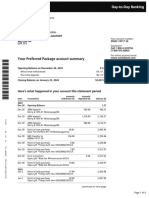

- BSNL Broadband BillDocument2 pagesBSNL Broadband BillSushubh50% (4)

- Philippine Christian University: Graduate School of Business and ManagementDocument6 pagesPhilippine Christian University: Graduate School of Business and ManagementCoreen AndradeNo ratings yet

- Warehouse Unit B Draft ContractDocument6 pagesWarehouse Unit B Draft ContractHR HaimeeNo ratings yet

- Tax Alert (December 2020)Document10 pagesTax Alert (December 2020)Rheneir MoraNo ratings yet

- Psalm Uc Guidelines PDFDocument19 pagesPsalm Uc Guidelines PDFRj FashionhouseNo ratings yet

- Republic of The Philippines National Capital Judicial Region Regional Trial Court Branch 12, Olongapo CityDocument13 pagesRepublic of The Philippines National Capital Judicial Region Regional Trial Court Branch 12, Olongapo CityJustine DagdagNo ratings yet

- Course: Digital Business Innovation Project: Hamley'S Instructions For The SubmissionDocument5 pagesCourse: Digital Business Innovation Project: Hamley'S Instructions For The SubmissionAbhishek SadanandNo ratings yet

- NGCP V Cabataña (SCA No. 049-07-2019) PDFDocument4 pagesNGCP V Cabataña (SCA No. 049-07-2019) PDFjoanna bellezaNo ratings yet

- BIR v. Office of The OmbudsmanDocument14 pagesBIR v. Office of The OmbudsmanJames Evan I. ObnamiaNo ratings yet

- Archbishop Reyes Ave, Cebu City, Cebu, 6000Document5 pagesArchbishop Reyes Ave, Cebu City, Cebu, 6000Ralf Arthur Silverio100% (1)

- Pbcom V CirDocument9 pagesPbcom V CirAbby ParwaniNo ratings yet

- Sample Position PaperDocument6 pagesSample Position PaperMaris Joy BartolomeNo ratings yet

- To The Young Women of MalolosDocument4 pagesTo The Young Women of MalolosGermayne GaluraNo ratings yet

- ITAD BIR RULING NO. 026-18, March 5, 2018Document10 pagesITAD BIR RULING NO. 026-18, March 5, 2018Kriszan ManiponNo ratings yet

- Proposal IncorpDocument2 pagesProposal IncorpConrad BrionesNo ratings yet

- Module 2 CatapusanDocument215 pagesModule 2 CatapusanPau SaulNo ratings yet

- Political Law: Discussion of Political CasesDocument43 pagesPolitical Law: Discussion of Political Casesjanelle_12No ratings yet

- Javier DO - Zuneca Parmaceutical V Natrapharm, Sep. 08 2020Document1 pageJavier DO - Zuneca Parmaceutical V Natrapharm, Sep. 08 2020Vel June De LeonNo ratings yet

- The 1987 ConstitutionDocument4 pagesThe 1987 ConstitutionDaisylen De Guzman AlanoNo ratings yet

- BIR Ruling No. 453-2018 Interest Income On Individual Loans Obtained From Banks That Are Not Securitized, Assigned or Participated OutDocument4 pagesBIR Ruling No. 453-2018 Interest Income On Individual Loans Obtained From Banks That Are Not Securitized, Assigned or Participated Outliz kawiNo ratings yet

- BirDocument15 pagesBirRudolf Christian Oliveras Ugma100% (1)

- Pagong BagalDocument1 pagePagong Bagaljuliet_emelinotmaestroNo ratings yet

- Stat Con DigestsDocument7 pagesStat Con DigestsnoonalawNo ratings yet

- Nature of Legislative PowerDocument5 pagesNature of Legislative PowerChin T. OndongNo ratings yet

- Summary of Significant SC Decisions (April May June 2011)Document2 pagesSummary of Significant SC Decisions (April May June 2011)elmersgluethebombNo ratings yet

- Tax Bulletin by SGV As of Oct 2014Document18 pagesTax Bulletin by SGV As of Oct 2014adobopinikpikanNo ratings yet

- Oblicon-Digests For Defective ContractsDocument5 pagesOblicon-Digests For Defective ContractsSuiNo ratings yet

- Course Outline IPLDocument3 pagesCourse Outline IPLNElle SAn FullNo ratings yet

- Position Paper of The Book Development Association of The Philippines Re: Tax and Duty Free Importation of Books Into The CountryDocument16 pagesPosition Paper of The Book Development Association of The Philippines Re: Tax and Duty Free Importation of Books Into The CountryManuel L. Quezon III100% (1)

- Partcor ReviewerDocument30 pagesPartcor ReviewerNikki AndradeNo ratings yet

- RR No. 9-2016 PDFDocument1 pageRR No. 9-2016 PDFJames SusukiNo ratings yet

- Different Modes of Acquiring OwnershipDocument1 pageDifferent Modes of Acquiring OwnershipAnnamaAnnamaNo ratings yet

- RR 5-2011Document5 pagesRR 5-2011RB BalanayNo ratings yet

- Civil Code Title VII - NuisanceDocument1 pageCivil Code Title VII - NuisanceE.F.FNo ratings yet

- Rmo 22 01Document20 pagesRmo 22 01Maria Leonora Bornales100% (1)

- Non-Receipt of A Written Notice of Dishonour of Checks: The Case of People vs. Manalo For B.P. Blg. 22Document6 pagesNon-Receipt of A Written Notice of Dishonour of Checks: The Case of People vs. Manalo For B.P. Blg. 22Judge Eliza B. Yu100% (4)

- RMC 35-06Document18 pagesRMC 35-06Aris Basco DuroyNo ratings yet

- People v. VeraDocument3 pagesPeople v. VeraJastine Mae DugayoNo ratings yet

- Withholding Tax Remittance Return: Kawanihan NG Rentas InternasDocument4 pagesWithholding Tax Remittance Return: Kawanihan NG Rentas InternasArlyn De Las AlasNo ratings yet

- De La Salle University College of Law: Lasallian Commission On Bar Operations 2018Document55 pagesDe La Salle University College of Law: Lasallian Commission On Bar Operations 2018Elisa Dela FuenteNo ratings yet

- Buy Sale Agreement 123ZDocument5 pagesBuy Sale Agreement 123ZcefuneslpezNo ratings yet

- NPC Drivers and Mechanics Assoc. vs. NAPOCORDocument28 pagesNPC Drivers and Mechanics Assoc. vs. NAPOCORj guevarraNo ratings yet

- Revenue Memorandum Order No. 37-94: March 25, 1994Document8 pagesRevenue Memorandum Order No. 37-94: March 25, 1994Rufino Gerard Moreno IIINo ratings yet

- Cta 2D CV 09224 M 2019feb12 AssDocument17 pagesCta 2D CV 09224 M 2019feb12 AssMelan YapNo ratings yet

- Property Art 440-465Document7 pagesProperty Art 440-465nbalanaNo ratings yet

- Penalties - Expired AtpDocument1 pagePenalties - Expired AtpCherry ChaoNo ratings yet

- Legal Opinion On Naturalization FinalDocument4 pagesLegal Opinion On Naturalization FinalKitem Kadatuan Jr.No ratings yet

- RR 05-99 PDFDocument1 pageRR 05-99 PDFDarrell MagsambolNo ratings yet

- Lecture 2 - ADR ScriptDocument5 pagesLecture 2 - ADR ScriptSteps RolsNo ratings yet

- Prescription, Waiver and Closure - Jamie Lyn HernandezDocument23 pagesPrescription, Waiver and Closure - Jamie Lyn HernandezJamie LynNo ratings yet

- RR 13-1998Document17 pagesRR 13-1998nikkaremullaNo ratings yet

- Commissioner of BIR v. Reyes GR .No. 159694Document11 pagesCommissioner of BIR v. Reyes GR .No. 159694lito77No ratings yet

- (2018) New BIR Income Tax Rates andDocument31 pages(2018) New BIR Income Tax Rates andGlenn Cacho Garce100% (1)

- PBCOM vs. CIRDocument19 pagesPBCOM vs. CIRColeen Navarro-RasmussenNo ratings yet

- An Overview On The Juvenile Justice System in The PhilippinesDocument10 pagesAn Overview On The Juvenile Justice System in The PhilippinesJake CopradeNo ratings yet

- Rmo 9-2000Document2 pagesRmo 9-2000Martin EspinosaNo ratings yet

- BIR RMC No. 62-2005Document15 pagesBIR RMC No. 62-2005dencave1No ratings yet

- Civil CasesDocument102 pagesCivil CasesRiza PerdidoNo ratings yet

- BLGF Opinion To Alsons Consolidated Resources Inc Dated 23 September 2009Document4 pagesBLGF Opinion To Alsons Consolidated Resources Inc Dated 23 September 2009Chasmere MagloyuanNo ratings yet

- 1-10 Tax Sept 9Document11 pages1-10 Tax Sept 9Niña ArmadaNo ratings yet

- DocxDocument16 pagesDocxaksNo ratings yet

- Air India ExpressDocument2 pagesAir India Expresskhozema mannanNo ratings yet

- Abalos - 2019 - Presented at SIBR 2019 (Osaka) Conference On Interdisciplinary Business and Economics Research, 4th - 5th July 2019, Osa PDFDocument42 pagesAbalos - 2019 - Presented at SIBR 2019 (Osaka) Conference On Interdisciplinary Business and Economics Research, 4th - 5th July 2019, Osa PDFLydia KusumadewiNo ratings yet

- Mastercam Training Guide Mill Lesson 2Document2 pagesMastercam Training Guide Mill Lesson 2DIEGO ARMANDO VANEGAS DUQUENo ratings yet

- Job Vacancy - Senior AuditorDocument1 pageJob Vacancy - Senior AuditorIrfan AhmedNo ratings yet

- Community Relations CHAPTER ONEDocument20 pagesCommunity Relations CHAPTER ONEAdewuyi Alani RidwanNo ratings yet

- PEC L6 Unit 3 - ExtensionDocument6 pagesPEC L6 Unit 3 - ExtensionNati MNo ratings yet

- Admiralty Information Overlay User Guide v1 0Document10 pagesAdmiralty Information Overlay User Guide v1 0fml2013100% (1)

- Poster DoveDocument2 pagesPoster Dovejawad nawazNo ratings yet

- Hse Planning and AuditingDocument4 pagesHse Planning and AuditingCaron KarlosNo ratings yet

- De Leon Solman 2014 2 CostDocument95 pagesDe Leon Solman 2014 2 CostJohn Laurence LoplopNo ratings yet

- BS en 00683-3 1997 (En)Document10 pagesBS en 00683-3 1997 (En)Emanuele MastrangeloNo ratings yet

- Inspiration For LawyersDocument4 pagesInspiration For LawyersNyakuni NobertNo ratings yet

- Sales & Distribution Channels in Mahindra & Mahindra LimitedDocument11 pagesSales & Distribution Channels in Mahindra & Mahindra Limitedsrinibas1988No ratings yet

- 2023 Signal Mountain Comparision Fire Study FinalDocument30 pages2023 Signal Mountain Comparision Fire Study FinalWTVC100% (1)

- Harshad Mehta ScamDocument2 pagesHarshad Mehta ScamAshmeet KAur 191398No ratings yet

- ASEFYLS4 Leadership in Action Project Outlines Screen Reader FriendlyDocument18 pagesASEFYLS4 Leadership in Action Project Outlines Screen Reader FriendlyAflaton AffyNo ratings yet

- Bashid 29Document34 pagesBashid 294 SEASONS DISCOUNTNo ratings yet

- India Volume 5 TATA SHAKTEEDocument2 pagesIndia Volume 5 TATA SHAKTEEreuben rodriguesNo ratings yet

- A Study On Consumer Perception Towards Coca-Cola Beverages "Document58 pagesA Study On Consumer Perception Towards Coca-Cola Beverages "Satyanarayana Sirigina74% (19)

- BankDocument6 pagesBankcarlos.me1No ratings yet

- A Study On Customer Satisfaction Towards Yamaha: BikesDocument30 pagesA Study On Customer Satisfaction Towards Yamaha: BikesMani kandanNo ratings yet

- IandE - Session 4 - Entrepreneurship - Deve Cycle and Brand Quiz - 7 FebDocument46 pagesIandE - Session 4 - Entrepreneurship - Deve Cycle and Brand Quiz - 7 Feblabolab344No ratings yet

- Methods of Credit Control Employed by The Central BankDocument4 pagesMethods of Credit Control Employed by The Central BankMD. IBRAHIM KHOLILULLAHNo ratings yet

- Fernando Andres Gimenez Futterknecht English CVDocument2 pagesFernando Andres Gimenez Futterknecht English CVFer GimenezNo ratings yet

- DA Portfolio ProjectDocument16 pagesDA Portfolio Projectabhinavkulkarni997No ratings yet