You might also like

- Projected Cash Flow Keffi Flour Mills LimitedDocument3 pagesProjected Cash Flow Keffi Flour Mills LimitedHrh SaddiquahNo ratings yet

- 1613233502-InvestorPresentation-February2021 Fermenta BiotechDocument34 pages1613233502-InvestorPresentation-February2021 Fermenta Biotechravi.youNo ratings yet

- Mumbai-400 051Document54 pagesMumbai-400 051Deep ShahNo ratings yet

- Bharat PetroleumDocument25 pagesBharat PetroleumMansi AroraNo ratings yet

- BB 20 Per Discount - Eligibility For BSNL Employees Own Connection - 18-10-10Document1 pageBB 20 Per Discount - Eligibility For BSNL Employees Own Connection - 18-10-10avd csrNo ratings yet

- Marine Electricals Annual Report 2022Document261 pagesMarine Electricals Annual Report 2022Hazem AhmedNo ratings yet

- Bharat San Char Nigam Limited: t$f4 ( MIDocument1 pageBharat San Char Nigam Limited: t$f4 ( MIRAMESHNo ratings yet

- Sundram FasternersDocument223 pagesSundram FasternersReTHINK INDIANo ratings yet

- BSNLDocument1 pageBSNLRaj MasterNo ratings yet

- Ack Amhpd0653k 2022-23 120306800310723Document1 pageAck Amhpd0653k 2022-23 120306800310723Bhavesh JainNo ratings yet

- Statement 932073059 20221025 112115 57Document1 pageStatement 932073059 20221025 112115 57hari tejaNo ratings yet

- IEC CertificateDocument1 pageIEC Certificatekishansahuind1No ratings yet

- Statement 932073059 20221025 112113 56Document1 pageStatement 932073059 20221025 112113 56hari tejaNo ratings yet

- DR Seema ParohaDocument21 pagesDR Seema ParohaTEERATH RAJNo ratings yet

- Form 16 - IT DEPT Part A - 20202021Document2 pagesForm 16 - IT DEPT Part A - 20202021Kritansh BindalNo ratings yet

- ICDRDocument32 pagesICDRrohitjpatel786100% (1)

- Form 16 - IT DEPT Part BDocument4 pagesForm 16 - IT DEPT Part BGauravNo ratings yet

- Authorization & Order Confirmation Letter Format For APOS OrdersDocument1 pageAuthorization & Order Confirmation Letter Format For APOS OrdersArijit GhoshNo ratings yet

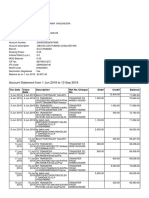

- Statement of Account: State Bank of IndiaDocument10 pagesStatement of Account: State Bank of IndiaSree ValsanNo ratings yet

- Nestle India LTDDocument12 pagesNestle India LTDHimanshu PatelNo ratings yet

- Statement of Account: Product: Ca-Gen-Pub-Metro/Urban-Inr Currency: INRDocument1 pageStatement of Account: Product: Ca-Gen-Pub-Metro/Urban-Inr Currency: INRCHITTA Ranjan pandaNo ratings yet

- BSNL Payslip January 2022Document1 pageBSNL Payslip January 2022saravananbsnlslm3866No ratings yet

- Jahangir 2Document4 pagesJahangir 2mannan41No ratings yet

- Form 16: Wipro LimitedDocument8 pagesForm 16: Wipro LimitedsaisindhuNo ratings yet

- StatementOfAccount 178556930 Sep15 102623Document5 pagesStatementOfAccount 178556930 Sep15 102623microstrategyhydNo ratings yet

- Prism JohnsonDocument294 pagesPrism JohnsonReTHINK INDIANo ratings yet

- Cipla PDFDocument243 pagesCipla PDFSamiksha PatilNo ratings yet

- Sugar Sector & Initiating Coverage Apr'20Document69 pagesSugar Sector & Initiating Coverage Apr'20VINAYAK AGARWALNo ratings yet

- Statement 6590792236 20220613 152347 5Document1 pageStatement 6590792236 20220613 152347 5mohamed arabathNo ratings yet

- ACK - KIIPK2548R - 2021-22 - 110330000060423 ItrDocument1 pageACK - KIIPK2548R - 2021-22 - 110330000060423 Itrkhan sa bnNo ratings yet

- 1 July To 17 Aug 2022Document6 pages1 July To 17 Aug 2022BHASKAR pNo ratings yet

- BTM BhiwaniDocument22 pagesBTM Bhiwaniराजीव गुप्ताNo ratings yet

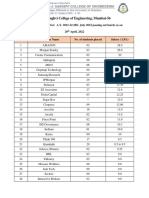

- D. J. Sanghvi College of Engineering, Mumbai-56Document4 pagesD. J. Sanghvi College of Engineering, Mumbai-56shubham nikatNo ratings yet

- AR19Document231 pagesAR19markelonnNo ratings yet

- Revised Paradip Refinery ReportDocument22 pagesRevised Paradip Refinery ReportioeuserNo ratings yet

- A Case Study On Downstream Supply Chain of An Indian Alcoholic Beverage ManufacturerDocument25 pagesA Case Study On Downstream Supply Chain of An Indian Alcoholic Beverage Manufacturertsega-alem berihu100% (1)

- Ref: MVS/MUM388/LKO-2023-3108 Date: 17: Letter of GuaranteeDocument1 pageRef: MVS/MUM388/LKO-2023-3108 Date: 17: Letter of GuaranteeEasyway WorkNo ratings yet

- Networth - Certificate For IDBIDocument4 pagesNetworth - Certificate For IDBISandip DasNo ratings yet

- Hatsun Agro ProductsDocument176 pagesHatsun Agro Productsannie christabel princyNo ratings yet

- Madan PayslipDocument1 pageMadan PayslipBADI APPALARAJUNo ratings yet

- Coal India Limited - Project SynopsisDocument3 pagesCoal India Limited - Project SynopsisTechomaniac 83No ratings yet

- UntitledDocument1 pageUntitledNagesh YadavNo ratings yet

- FORM 16 TAX DEDUCTION CERTIFICATEDocument2 pagesFORM 16 TAX DEDUCTION CERTIFICATEpiyushkumar patelNo ratings yet

- ITR Acknowledgement for AY 2022-23Document1 pageITR Acknowledgement for AY 2022-23QunalNo ratings yet

- Form 16 SummaryDocument7 pagesForm 16 SummaryMithlesh SharmaNo ratings yet

- Black RoseDocument26 pagesBlack RosesidNo ratings yet

- K H EXPORTS INDIA PRIVATE LIMITED TANNERY 'A' DIVISION EFFLUENT TREATMENT UNITDocument26 pagesK H EXPORTS INDIA PRIVATE LIMITED TANNERY 'A' DIVISION EFFLUENT TREATMENT UNITDhinesh Raj K SNo ratings yet

- Congratulations Offer Letter Rahul Gangarekar DealerDocument2 pagesCongratulations Offer Letter Rahul Gangarekar Dealerrahul gangarekarNo ratings yet

- Prabhar Oil CompanyDocument15 pagesPrabhar Oil CompanyKabeer QureshiNo ratings yet

- Soymilk PDFDocument8 pagesSoymilk PDFutkarsh AryaNo ratings yet

- Automobile IndustryDocument7 pagesAutomobile IndustryAniket VermaNo ratings yet

- Company: Name: Serial No: Valid Up To: Unit: Emergency NoDocument1 pageCompany: Name: Serial No: Valid Up To: Unit: Emergency NoediNo ratings yet

- Travel Agency Invoice TemplateDocument2 pagesTravel Agency Invoice Templatesreekanth dasariNo ratings yet

- Organization Study: Mangalore Chemicals and Fertilizers LTDDocument14 pagesOrganization Study: Mangalore Chemicals and Fertilizers LTDHariprasad bhat0% (1)

- s5 PDFDocument5 pagess5 PDFKeshav KumarNo ratings yet

- Certificate of IncorporationDocument1 pageCertificate of IncorporationVivek DixitNo ratings yet

- Salary CalculationDocument1 pageSalary CalculationushasathyaNo ratings yet

- PDF 949279100021221Document1 pagePDF 949279100021221MUTHUMUNEESH WARANNo ratings yet

- 31032022Document115 pages31032022Mohammad ZaidNo ratings yet

- K.P.R, Mill LimitedDocument22 pagesK.P.R, Mill LimitedThomas Anto Nishanth PausterNo ratings yet

- BCOM FA Unit-2Document44 pagesBCOM FA Unit-2Kavitha aradhyaNo ratings yet

- Closing and Worksheet: 20.1 Closing Entries For Revenue AccountsDocument8 pagesClosing and Worksheet: 20.1 Closing Entries For Revenue AccountsZaheer Swati100% (1)

- Project Report Suresh Sonaji Gaikwad 07.07.2023Document12 pagesProject Report Suresh Sonaji Gaikwad 07.07.2023viraj mNo ratings yet

- FR (New) Suggested Ans CA Final Jan 21Document33 pagesFR (New) Suggested Ans CA Final Jan 21ritz meshNo ratings yet

- Payments To MSMEs – Decoding Section 43B (H) Read With MSMED Act - Taxguru - inDocument4 pagesPayments To MSMEs – Decoding Section 43B (H) Read With MSMED Act - Taxguru - insukantabera215No ratings yet

- Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced LevelDocument12 pagesCambridge International Examinations Cambridge International Advanced Subsidiary and Advanced LevelangelineNo ratings yet

- Fabm NotesDocument8 pagesFabm NotesMark Jay Bongolan100% (1)

- Department of commerce 1st semester examDocument9 pagesDepartment of commerce 1st semester examEshal KhanNo ratings yet

- QB Bba Iii 2019Document256 pagesQB Bba Iii 2019Vansh DedhaNo ratings yet

- Chapter 3Document7 pagesChapter 3bartabatoes rerunNo ratings yet

- Terms of Reference (Tor) Post: Vacancies: 1 Post Type: Full Time Reporting To: Finance ManagerDocument2 pagesTerms of Reference (Tor) Post: Vacancies: 1 Post Type: Full Time Reporting To: Finance ManagerMohamed LammahNo ratings yet

- SMO 3 Financial ManagementDocument651 pagesSMO 3 Financial Managementasg10No ratings yet

- LR and Other Receivables Concepts ActivitiesDocument4 pagesLR and Other Receivables Concepts ActivitiesAthena Fatmah AmpuanNo ratings yet

- Completed Sba Form 1919Document13 pagesCompleted Sba Form 1919api-568505563No ratings yet

- Finance PowerpointDocument41 pagesFinance PowerpointAvinash KujurNo ratings yet

- Partnership Acc Scanner by NahtaDocument82 pagesPartnership Acc Scanner by NahtaVivek KoliNo ratings yet

- Ultimate Sample Paper Sol.Document20 pagesUltimate Sample Paper Sol.Tûshar ThakúrNo ratings yet

- Moorad Choudhry Anthology: Reader's Guide: January 2020Document33 pagesMoorad Choudhry Anthology: Reader's Guide: January 2020Mr ThyNo ratings yet

- RPT Math Form 3 DLPDocument17 pagesRPT Math Form 3 DLPkhadijahNo ratings yet

- Letter For Foreclosure: Parth Ramilaben Kapadia KapadiaDocument2 pagesLetter For Foreclosure: Parth Ramilaben Kapadia KapadiaParth KapadiaNo ratings yet

- Financial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Test BankDocument24 pagesFinancial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Test Bankmrsbrianajonesmdkgzxyiatoq100% (26)

- Accounting For Management: Project On Financial Statement Analysis of H U L (HUL)Document34 pagesAccounting For Management: Project On Financial Statement Analysis of H U L (HUL)Aditya ChughNo ratings yet

- GFS 2001 Manual-Basic ConceptsDocument40 pagesGFS 2001 Manual-Basic ConceptsProfessor Tarun DasNo ratings yet

- Business Finance Chapter 3Document42 pagesBusiness Finance Chapter 3chloe frostNo ratings yet

- AccountingDocument3 pagesAccountingAtiya IftikharNo ratings yet

- Audit 2 (T) - Topic2A SasaDocument27 pagesAudit 2 (T) - Topic2A SasaEleonora VinessaNo ratings yet

- Off Balance SheetDocument15 pagesOff Balance SheetWan RuschdeyNo ratings yet

- Law On Obligation Contracts REVIEWERDocument8 pagesLaw On Obligation Contracts REVIEWERroselyn cortezNo ratings yet

- Summary of Voting Requirements (RCC)Document3 pagesSummary of Voting Requirements (RCC)だみNo ratings yet

- ACC304-Review Questions Fin InstrumentsDocument2 pagesACC304-Review Questions Fin InstrumentsGeorge AdjeiNo ratings yet