You might also like

- CV 2023062810202090Document3 pagesCV 2023062810202090Kumar SinghNo ratings yet

- Capstone Projectpratim Roy Pgdm18381Document30 pagesCapstone Projectpratim Roy Pgdm18381mayankNo ratings yet

- Proposal On Stolen Mobile Finder SystemDocument59 pagesProposal On Stolen Mobile Finder SystemVijay Vardhan KudariNo ratings yet

- SIP - Anaida PaulDocument40 pagesSIP - Anaida PaulOmkar PadaveNo ratings yet

- Internship ReportDocument85 pagesInternship ReportAlen AugustineNo ratings yet

- Project Report On EquityDocument77 pagesProject Report On Equityaashish vermaNo ratings yet

- Summer Training Report On: Working Capital & ProcessesDocument82 pagesSummer Training Report On: Working Capital & ProcessesAnonymous 0ITLyi958JNo ratings yet

- Mayank Talesara ResumeDocument3 pagesMayank Talesara ResumeKumar SinghNo ratings yet

- Sample Report DCFDocument0 pagesSample Report DCFagarwalandyNo ratings yet

- ReportDocument86 pagesReportSwati ChoudharyNo ratings yet

- Finance ProjectDocument14 pagesFinance ProjectASUTOSH MUDULINo ratings yet

- Annual Report of ITC 2021 UDocument33 pagesAnnual Report of ITC 2021 UAkash Tewari Student, Jaipuria LucknowNo ratings yet

- Isha - Synopsis - Icici Fundamental RatioDocument12 pagesIsha - Synopsis - Icici Fundamental RatioPramod ShawNo ratings yet

- Annual Report of ITC 2021Document34 pagesAnnual Report of ITC 2021Akash Tewari Student, Jaipuria LucknowNo ratings yet

- Sl. No. Topics Pg. No. 1. Chapter - I 2-5: Session 2012-13Document25 pagesSl. No. Topics Pg. No. 1. Chapter - I 2-5: Session 2012-13Subhendu GhoshNo ratings yet

- Final Internship ReportDocument10 pagesFinal Internship ReportMaryam NisarNo ratings yet

- Finance Case StudyDocument22 pagesFinance Case StudykrishnaNo ratings yet

- Ratio AnalysisDocument79 pagesRatio Analysisanjali dhadde100% (1)

- Final Report - Neeraj Kumar BhagatDocument51 pagesFinal Report - Neeraj Kumar BhagatBharatNo ratings yet

- Transcritption - Financials and Credit RatingsDocument6 pagesTranscritption - Financials and Credit Ratingsmanoj reddyNo ratings yet

- Internship ReportDocument30 pagesInternship ReportYash BatraNo ratings yet

- Project Report On Outsourcing IT Operations v1Document25 pagesProject Report On Outsourcing IT Operations v1Piyush JaainNo ratings yet

- Module-1 - BAV For Students ReferenceDocument54 pagesModule-1 - BAV For Students ReferenceYash LataNo ratings yet

- Solar IndustriesDocument313 pagesSolar IndustriesReTHINK INDIANo ratings yet

- Summer Project Report Ratio Analysis of Kotak Mahindra Bank LTDDocument31 pagesSummer Project Report Ratio Analysis of Kotak Mahindra Bank LTDsurendraNo ratings yet

- Ratio Analysis 1Document66 pagesRatio Analysis 1Radha ChoudhariNo ratings yet

- Zaraz1 - Group Audit and Others 2Document8 pagesZaraz1 - Group Audit and Others 2Nur Izzah IlyanaNo ratings yet

- Chapter 1Document20 pagesChapter 1aishahNo ratings yet

- Master of Business Administration 2020-2022: Financial Analysis of Infosys Ltd. For THE YEAR 2016-20Document36 pagesMaster of Business Administration 2020-2022: Financial Analysis of Infosys Ltd. For THE YEAR 2016-20Prachi RaiNo ratings yet

- Zomato - Detailed IPODocument11 pagesZomato - Detailed IPOsaurabhNo ratings yet

- Chetana's R. K. Institute of Management & Research: Bandra (East), MumbaiDocument47 pagesChetana's R. K. Institute of Management & Research: Bandra (East), MumbaiVijitashva AcharyaNo ratings yet

- Project Report India Infoline.Document20 pagesProject Report India Infoline.avneeshpimr143100% (4)

- Final E-Journal.95-105Document11 pagesFinal E-Journal.95-105Harish N. ChaudhariNo ratings yet

- IIF SecuritiesDocument296 pagesIIF SecuritiesReTHINK INDIANo ratings yet

- A Project Report ON 'Audit of Financial Statement': Management Education & Research InstituteDocument14 pagesA Project Report ON 'Audit of Financial Statement': Management Education & Research InstituteAakasH TivariNo ratings yet

- Company Analysis#Document22 pagesCompany Analysis#ritikraj569No ratings yet

- As 15 - Gratuity - Harmony Motors - 31032018Document15 pagesAs 15 - Gratuity - Harmony Motors - 31032018prasad and company limitedNo ratings yet

- Finance Project 147Document68 pagesFinance Project 147Himanshu ParakhNo ratings yet

- Report SagarDocument89 pagesReport Sagarnabeelmdkhan6888100% (1)

- Sip ReportDocument57 pagesSip Reportvijay soniNo ratings yet

- Stock Pitch InformationDocument30 pagesStock Pitch InformationBudhil KonankiNo ratings yet

- Aadrish Bashir, ACA: Career ObjectiveDocument2 pagesAadrish Bashir, ACA: Career ObjectiveRukhshindaNo ratings yet

- 02 & 12 - Anup & Hitesh - Jubilant FoodWorks LTDDocument10 pages02 & 12 - Anup & Hitesh - Jubilant FoodWorks LTDasitbhatiaNo ratings yet

- Comparative Analysis of Mutual Fund Schemes and Major Investment AvenuesDocument52 pagesComparative Analysis of Mutual Fund Schemes and Major Investment AvenuesPrithvi Raj SinghNo ratings yet

- A Report ON A Study On The Plans&Fund Ivestements of Unit Link Products in Shiiram Life Insurance Co - Ltd. By: Veera Hanuman 19BSP3190Document60 pagesA Report ON A Study On The Plans&Fund Ivestements of Unit Link Products in Shiiram Life Insurance Co - Ltd. By: Veera Hanuman 19BSP3190bathula veerahanumanNo ratings yet

- Chap 7Document9 pagesChap 7samadritapramanik3No ratings yet

- "Fundamental Analysis of Selected Automobile Sector Companies For DSIJPL" - MBA Internship Report by Sameer SawantDocument75 pages"Fundamental Analysis of Selected Automobile Sector Companies For DSIJPL" - MBA Internship Report by Sameer SawantSawant Sameer67% (3)

- Black Book Bhavik.1Document80 pagesBlack Book Bhavik.1Prashant MalpekarNo ratings yet

- Project Report BBA MOSLDocument14 pagesProject Report BBA MOSLdimpyNo ratings yet

- Fundamental Analysis On The Top Four Private Banks of IndiaDocument38 pagesFundamental Analysis On The Top Four Private Banks of IndiaMiral PatelNo ratings yet

- Practice Questions Valuations & Business Modelling PDFDocument103 pagesPractice Questions Valuations & Business Modelling PDFRam Iyer0% (1)

- 703 - Finance For Managers - Azizul Hakem - Sub On 18 JulyDocument10 pages703 - Finance For Managers - Azizul Hakem - Sub On 18 JulyAzeezulNo ratings yet

- Financial Statement Analysis Sip.... BhagyashreeDocument61 pagesFinancial Statement Analysis Sip.... BhagyashreeShubham PrasadNo ratings yet

- A Project Report On Competitive AnalysisDocument115 pagesA Project Report On Competitive AnalysisMallesh ArjaNo ratings yet

- A Study of the Supply Chain and Financial Parameters of a Small BusinessFrom EverandA Study of the Supply Chain and Financial Parameters of a Small BusinessNo ratings yet

- Curing Corporate Short-Termism: Future Growth vs. Current EarningsFrom EverandCuring Corporate Short-Termism: Future Growth vs. Current EarningsNo ratings yet

- Achieving Fair Value: How Companies Can Better Manage Their Relationships with InvestorsFrom EverandAchieving Fair Value: How Companies Can Better Manage Their Relationships with InvestorsNo ratings yet

- Qtrly - Reportq1 FY 2008 2009Document2 pagesQtrly - Reportq1 FY 2008 2009Bhavin SagarNo ratings yet

- Bse Sme Ipo IndexDocument4 pagesBse Sme Ipo IndexBhavin SagarNo ratings yet

- Nebbia Mutual NDADocument3 pagesNebbia Mutual NDABhavin SagarNo ratings yet

- Yap 31 1 19Document345 pagesYap 31 1 19Bhavin SagarNo ratings yet

- Capital Reduction - Escorts LTD - GalacticoDocument10 pagesCapital Reduction - Escorts LTD - GalacticoBhavin SagarNo ratings yet

- August 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsDocument10 pagesAugust 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsBhavin SagarNo ratings yet

- Amalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDDocument10 pagesAmalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDBhavin SagarNo ratings yet

- Revised Underwriting Agreement 31.03Document14 pagesRevised Underwriting Agreement 31.03Bhavin SagarNo ratings yet

- Revised Market Making Agreement 31.03Document13 pagesRevised Market Making Agreement 31.03Bhavin SagarNo ratings yet

- Statement of Transactions: Sundaram Finance LimitedDocument1 pageStatement of Transactions: Sundaram Finance LimitedBhavin SagarNo ratings yet

- Underwriters AgreementDocument15 pagesUnderwriters AgreementBhavin SagarNo ratings yet

- List of Valuation ReportsDocument18 pagesList of Valuation ReportsBhavin SagarNo ratings yet

- Amalgamation - Share India Securities - Turnaround Corporate AdvisorsDocument5 pagesAmalgamation - Share India Securities - Turnaround Corporate AdvisorsBhavin SagarNo ratings yet

- Demerger May 2021 - Tips Industries LTD by Inga Advisors MumbaiDocument4 pagesDemerger May 2021 - Tips Industries LTD by Inga Advisors MumbaiBhavin SagarNo ratings yet

- MCA FinanicialsDocument50 pagesMCA FinanicialsBhavin SagarNo ratings yet

- 02 Corporate Orange Powerpoint Presentations 16x9 1Document13 pages02 Corporate Orange Powerpoint Presentations 16x9 1Bhavin SagarNo ratings yet

- Revised RV - Draft Valuation Report - Hakuna MatataDocument11 pagesRevised RV - Draft Valuation Report - Hakuna MatataBhavin SagarNo ratings yet

- Bulk DealsDocument63 pagesBulk DealsBhavin SagarNo ratings yet

- Corporate Deck - InternationalDocument16 pagesCorporate Deck - InternationalBhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- EKI Energy Services Limited: Payments MadeDocument2 pagesEKI Energy Services Limited: Payments MadeBhavin SagarNo ratings yet

- Valuation Assignement - WIPDocument2 pagesValuation Assignement - WIPBhavin SagarNo ratings yet

- EKI Energy Services Limited: Payments MadeDocument2 pagesEKI Energy Services Limited: Payments MadeBhavin SagarNo ratings yet

- Bhavin Valuation Cases For FY21Document17 pagesBhavin Valuation Cases For FY21Bhavin SagarNo ratings yet

- Bhavin - Valuation Cases - May 2021Document3 pagesBhavin - Valuation Cases - May 2021Bhavin SagarNo ratings yet

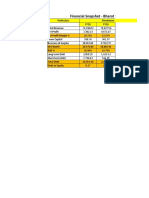

- Bharat Serums & Vaccines LTD - Financial SnapshotDocument2 pagesBharat Serums & Vaccines LTD - Financial SnapshotBhavin SagarNo ratings yet

- Appsee SDK Guide - Appsee EbookDocument45 pagesAppsee SDK Guide - Appsee EbookPeladitoNo ratings yet

- Interview Questions For QA Tester-1Document31 pagesInterview Questions For QA Tester-1namrata kokateNo ratings yet

- The Unreasonable Effectiveness of Data by Halevy, NorvigDocument5 pagesThe Unreasonable Effectiveness of Data by Halevy, NorvigFlaboosNo ratings yet

- Sai Srujana Resume 2019Document2 pagesSai Srujana Resume 2019Sai srujanaNo ratings yet

- IllustratorDocument27 pagesIllustratorVinti MalikNo ratings yet

- Runge-Kutta 2nd Order Method For Ordinary Differential EquationsDocument10 pagesRunge-Kutta 2nd Order Method For Ordinary Differential EquationsalbarNo ratings yet

- A Cloud Based Intrusion DetectionDocument5 pagesA Cloud Based Intrusion DetectionRamsen ShivNo ratings yet

- BSE CaseDocument2 pagesBSE CaseSwadesh -No ratings yet

- CSPC 104 - Algorithms and Complexity 2nd Semester, School Year 2020-2021Document3 pagesCSPC 104 - Algorithms and Complexity 2nd Semester, School Year 2020-2021cil dacaymatNo ratings yet

- BottDocument328 pagesBottafaqweefNo ratings yet

- Pitch Deck Pi Code Club NewDocument13 pagesPitch Deck Pi Code Club NewKannan JojodeNo ratings yet

- Capacitors: BY: Janaki G. Nair Abhishek GautamDocument14 pagesCapacitors: BY: Janaki G. Nair Abhishek GautamAbhishek GautamNo ratings yet

- Tsegaye Mekuria Checkol - ResumeDocument4 pagesTsegaye Mekuria Checkol - Resumetsecosby100% (1)

- An E-Readiness Assessment of ICT Integration in Public Primary Schools in Kenya Case of Nyeri CountyDocument5 pagesAn E-Readiness Assessment of ICT Integration in Public Primary Schools in Kenya Case of Nyeri CountyATSNo ratings yet

- PeopleTools 8.54 Installation For OracleDocument956 pagesPeopleTools 8.54 Installation For OraclehimanshumaheshwariNo ratings yet

- The TWAIN Working Group March 29, 1999: White Paper: Capability OrderingDocument4 pagesThe TWAIN Working Group March 29, 1999: White Paper: Capability Orderingbcrra orlandoNo ratings yet

- Parameters For IVG-85X50PYA-SDocument3 pagesParameters For IVG-85X50PYA-SpiolNo ratings yet

- Annex A-CSB-Foodpanda MOADocument9 pagesAnnex A-CSB-Foodpanda MOAJhon Rainier TanNo ratings yet

- Cmos Design Objective QuestionsDocument18 pagesCmos Design Objective QuestionsdycsteiznNo ratings yet

- Qualification Specification For Level 4 Certificate Bilingual SkillsDocument26 pagesQualification Specification For Level 4 Certificate Bilingual SkillsBSLcourses.co.ukNo ratings yet

- Technological Institute of The PhilippinesDocument36 pagesTechnological Institute of The PhilippinesRahp RellyNo ratings yet

- Hiperwall: Videowall Content and Source Management SolutionDocument3 pagesHiperwall: Videowall Content and Source Management Solutionmario maldonadoNo ratings yet

- 1783-Um007 - En-P - Statrix 5700Document528 pages1783-Um007 - En-P - Statrix 5700Nguyễn SangNo ratings yet

- Nuvoton N76E003AT20 Minimum System Board Nu-Link Programming Development BoardDocument10 pagesNuvoton N76E003AT20 Minimum System Board Nu-Link Programming Development BoardKokhito BlackHoleNo ratings yet

- 10 Gautier Humbert LegrandDocument41 pages10 Gautier Humbert LegrandGodyNo ratings yet

- Service Manual of FUS-3000Plus Urinalysis Hybrid REV.2020-10Document238 pagesService Manual of FUS-3000Plus Urinalysis Hybrid REV.2020-10Albeiro PiraquiveNo ratings yet

- FDocument1 pageFurang awak bana sumarak dalam kampuanngNo ratings yet

- To56 2.5g DFB Laser Diode 1310nm Data Sheet 602001Document3 pagesTo56 2.5g DFB Laser Diode 1310nm Data Sheet 602001GLsun MallNo ratings yet

- Allied - Global Hyperloop Technology Market, 2022-2026Document169 pagesAllied - Global Hyperloop Technology Market, 2022-2026riccardo cilentoNo ratings yet

- PBL GroupingDocument20 pagesPBL GroupingJihah RazakNo ratings yet