You might also like

- Experience Rating PDF enDocument17 pagesExperience Rating PDF envalerieNo ratings yet

- Build Your Business Build Your Business: Performance Summary Performance SummaryDocument6 pagesBuild Your Business Build Your Business: Performance Summary Performance Summaryarun kumarNo ratings yet

- Discount Rates: III: Relative Risk MeasuresDocument20 pagesDiscount Rates: III: Relative Risk MeasuresElliNo ratings yet

- White Paper Cost To ServeDocument4 pagesWhite Paper Cost To ServeSurfenNo ratings yet

- BHGHGHDocument48 pagesBHGHGHS Praveen Kumar SivakumarNo ratings yet

- 03 Price OptimisationDocument16 pages03 Price OptimisationWmray CheungNo ratings yet

- Loss RatioDocument3 pagesLoss RatiohieutlbkreportNo ratings yet

- Cost of Not Having DRaaSDocument7 pagesCost of Not Having DRaaSQuality SecretNo ratings yet

- Internal Performance Measurement Systems. in Such An IntensiveDocument1 pageInternal Performance Measurement Systems. in Such An IntensiveMihaelaNo ratings yet

- Control: The Management Control Process: Changes From Eleventh EditionDocument25 pagesControl: The Management Control Process: Changes From Eleventh EditionAlka Narayan100% (1)

- Mind MapDocument6 pagesMind MapSyaz Amri100% (1)

- Employee Benefits Quiz Bank Review Flashcards - QuizletDocument1 pageEmployee Benefits Quiz Bank Review Flashcards - QuizletcathNo ratings yet

- Chap 8 - Executive Compensation and IncentivesDocument19 pagesChap 8 - Executive Compensation and IncentivesHM.No ratings yet

- CH 2Document10 pagesCH 2api-421468107No ratings yet

- LossCostWhatitMeans,HowtoCalculate_1710888214280Document5 pagesLossCostWhatitMeans,HowtoCalculate_1710888214280williamseugine2008No ratings yet

- Expenses WP 1988Document48 pagesExpenses WP 1988aditikhanal.135No ratings yet

- Cost DynamicsDocument6 pagesCost DynamicskshamamehtaNo ratings yet

- Workforce Alignment and The Bottom Line: The ROI of Enterprise Compensation ManagementDocument19 pagesWorkforce Alignment and The Bottom Line: The ROI of Enterprise Compensation ManagementGunjan KumariNo ratings yet

- Tl số 1-c7Document16 pagesTl số 1-c7kimkhanh200804No ratings yet

- FandI ST2 200509 ReportDocument15 pagesFandI ST2 200509 ReportHafiz IqbalNo ratings yet

- 01. Compensation, Cost and SystemsDocument20 pages01. Compensation, Cost and Systemsbanerjeechiranjib637No ratings yet

- Warranty Management: Converting Challenges to Market DifferentiatorsDocument15 pagesWarranty Management: Converting Challenges to Market Differentiatorssoleil34No ratings yet

- ECON 004 Module 1 2Document24 pagesECON 004 Module 1 2Majerlie Sigfried PerezNo ratings yet

- Fin - 515 - Smart - Chapter 1 Overview of Corporate Finance - Tute Solutions - 1Document3 pagesFin - 515 - Smart - Chapter 1 Overview of Corporate Finance - Tute Solutions - 1Ray Gworld50% (2)

- Depreciation in Accounting - Meaning, Types & ExamplesDocument20 pagesDepreciation in Accounting - Meaning, Types & Examplesv_u_ingle2003No ratings yet

- Lockouttagout Catalogue Europe EnglishDocument104 pagesLockouttagout Catalogue Europe EnglishMOMEN MHUSENNo ratings yet

- 003 03economicDocument5 pages003 03economiceyoboldairNo ratings yet

- Analyzing Revenue and Expenses TransactionsDocument28 pagesAnalyzing Revenue and Expenses TransactionsKaden Kelly100% (1)

- Answer DashDocument6 pagesAnswer DashJeffrey AmitNo ratings yet

- SCDL Solved Papers & Assignments - Security Analysis and Portfolio Management - Set 3Document13 pagesSCDL Solved Papers & Assignments - Security Analysis and Portfolio Management - Set 3Om PrakashNo ratings yet

- The Return On Investment of Automated Patch Management: White Paper - July 2006Document10 pagesThe Return On Investment of Automated Patch Management: White Paper - July 2006buckwheattbNo ratings yet

- P2 U.8 21 May 12Document24 pagesP2 U.8 21 May 12Khaled YoussefNo ratings yet

- Accounting For Decision Making and Control 8th Edition Zimmerman Solutions Manual Full Chapter PDFDocument68 pagesAccounting For Decision Making and Control 8th Edition Zimmerman Solutions Manual Full Chapter PDFfinnhuynhqvzp2c100% (14)

- Corporate Finance 12Document6 pagesCorporate Finance 12Mujtaba AhmadNo ratings yet

- Original 1489564280 Chapter 6 Quota Share TreatiesDocument12 pagesOriginal 1489564280 Chapter 6 Quota Share TreatiesmakeshwaranNo ratings yet

- 2009 10 Brand Valuation Additional InformationDocument2 pages2009 10 Brand Valuation Additional InformationAnuja BhakuniNo ratings yet

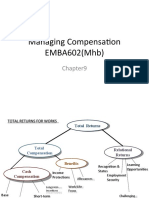

- EMBA602 - Managing CompensationDocument23 pagesEMBA602 - Managing CompensationMd Mostafizur RahamanNo ratings yet

- Policy Administration Systems 1Document4 pagesPolicy Administration Systems 1api-3833945No ratings yet

- Compensation Survey 2021Document14 pagesCompensation Survey 2021Oussama NasriNo ratings yet

- Cbmec 102 ProjectDocument3 pagesCbmec 102 ProjectcyrillejeahdpNo ratings yet

- Notes On End of Chapter QuestionsDocument31 pagesNotes On End of Chapter Questionsduong duongNo ratings yet

- Advanced ClaimsDocument15 pagesAdvanced ClaimsHimanshu SappalNo ratings yet

- Compensation Framework for Analyzing Employment RelationshipsDocument14 pagesCompensation Framework for Analyzing Employment RelationshipsAnonymous 1Rj80jNo ratings yet

- MEASURING RELATIVE RISKDocument19 pagesMEASURING RELATIVE RISKCarlos RojasNo ratings yet

- DGYoung Dentist PresentationDocument103 pagesDGYoung Dentist PresentationD.WorkuNo ratings yet

- MOB PowerpointDocument8 pagesMOB Powerpointreeisha7No ratings yet

- C13 Gitman Leverage and CapitalDocument53 pagesC13 Gitman Leverage and CapitalPhước Nguyễn100% (1)

- Understanding The Cost of Workers Compensation PremiumsDocument2 pagesUnderstanding The Cost of Workers Compensation PremiumseldhobehananNo ratings yet

- Solution Manual For Managerial Economics Applications Strategy and Tactics 11th Edition by McGuiganDocument5 pagesSolution Manual For Managerial Economics Applications Strategy and Tactics 11th Edition by McGuigana366773695No ratings yet

- Maximizing Distributor Margins and ProfitabilityDocument11 pagesMaximizing Distributor Margins and Profitabilitywasif ahmedNo ratings yet

- Midterm: Đỗ Thị Lâm Oanh-18071193Document5 pagesMidterm: Đỗ Thị Lâm Oanh-18071193Diệu QuỳnhNo ratings yet

- Cost AnalysisDocument15 pagesCost AnalysisAman NaNo ratings yet

- PWC Loyalty Analytics ExposedDocument13 pagesPWC Loyalty Analytics ExposedUmang GuptaNo ratings yet

- SC/Tetra: It's Not Like I'm My Boss' Favorite or Something, I Just Know How He ThinksDocument3 pagesSC/Tetra: It's Not Like I'm My Boss' Favorite or Something, I Just Know How He ThinkskglorstadNo ratings yet

- SafteyDocument26 pagesSafteyFortiter FysproNo ratings yet

- Chapter 07 The Costs of ProductionDocument12 pagesChapter 07 The Costs of ProductionShabaz SharierNo ratings yet

- HEAT & Business Travel Guide - For Subcontractor (Expats)Document10 pagesHEAT & Business Travel Guide - For Subcontractor (Expats)Rocky BisNo ratings yet

- Majnoon Oil Field - Remote Location Fitness To Work (00000003)Document9 pagesMajnoon Oil Field - Remote Location Fitness To Work (00000003)Rocky BisNo ratings yet

- Short On Boarding Manual For New Joiners: Prepared by Fadlan ArsllaniDocument3 pagesShort On Boarding Manual For New Joiners: Prepared by Fadlan ArsllaniRocky BisNo ratings yet

- FM Service Request Form-MLC CANTEEN DISHWASH FLOORDocument1 pageFM Service Request Form-MLC CANTEEN DISHWASH FLOORNiraNo ratings yet

- Pack Mean Menu StickersDocument10 pagesPack Mean Menu StickersRocky BisNo ratings yet

- Mohssen Nemah Abud Ali-1Document1 pageMohssen Nemah Abud Ali-1Rocky BisNo ratings yet

- Hazard Observation CardDocument2 pagesHazard Observation CardRocky BisNo ratings yet

- SL# Employer/ Company Full Name Staff Nature : Mandatory MandatoryDocument4 pagesSL# Employer/ Company Full Name Staff Nature : Mandatory MandatoryRocky BisNo ratings yet

- Ali Bassim Abdul-Redah: Address: Mobile: E-Mail: Gender: Date of Births: NationalityDocument2 pagesAli Bassim Abdul-Redah: Address: Mobile: E-Mail: Gender: Date of Births: NationalityRocky BisNo ratings yet

- Pack Mean Menu Stickers - 2Document5 pagesPack Mean Menu Stickers - 2Rocky BisNo ratings yet

- HSE Time Sheet (Document1 pageHSE Time Sheet (Rocky BisNo ratings yet

- Petrofac Laundry MSDS File Index PageDocument1 pagePetrofac Laundry MSDS File Index PageRocky BisNo ratings yet

- Chemical Inventory ListDocument5 pagesChemical Inventory ListRocky BisNo ratings yet

- RPSG-IMS-HS-F - 01 - Hazard Observation CardDocument2 pagesRPSG-IMS-HS-F - 01 - Hazard Observation CardRocky BisNo ratings yet

- MSDS For OIL REMOVER-6104Document5 pagesMSDS For OIL REMOVER-6104Rocky BisNo ratings yet

- Material Safety Data Sheet: Elgisi Glass CleanerDocument2 pagesMaterial Safety Data Sheet: Elgisi Glass CleanerRocky BisNo ratings yet

- Material Safety Data Sheet for NaphthaleneDocument6 pagesMaterial Safety Data Sheet for NaphthaleneRocky BisNo ratings yet

- Jini Dishwashing DetergentDocument5 pagesJini Dishwashing DetergentRocky BisNo ratings yet

- Material Safety Data Sheet Msds JINI Soap: Section 1: Product and Company IdentificationDocument6 pagesMaterial Safety Data Sheet Msds JINI Soap: Section 1: Product and Company IdentificationRocky BisNo ratings yet

- Material Safety Data Sheet Liquid Soap JiniDocument4 pagesMaterial Safety Data Sheet Liquid Soap JiniRocky BisNo ratings yet

- Main Gate House Keeping StoreDocument1 pageMain Gate House Keeping StoreRocky BisNo ratings yet

- MSDS/C.O.S.H.H File Petrofac Laundry: RPSG HseDocument1 pageMSDS/C.O.S.H.H File Petrofac Laundry: RPSG HseRocky BisNo ratings yet

- Material Safety Data Sheet Liquid Soap JiniDocument4 pagesMaterial Safety Data Sheet Liquid Soap JiniRocky BisNo ratings yet

- Material Safety Data Sheet: Bivy Multi - Purpose CleanerDocument2 pagesMaterial Safety Data Sheet: Bivy Multi - Purpose CleanerRocky BisNo ratings yet

- Phase One DFACDocument1 pagePhase One DFACRocky BisNo ratings yet

- Petrofac CampDocument1 pagePetrofac CampRocky BisNo ratings yet

- GCMC Utility AreaDocument1 pageGCMC Utility AreaRocky BisNo ratings yet

- MSDS/C.O.S.H.H File: GCMC DfacDocument1 pageMSDS/C.O.S.H.H File: GCMC DfacRocky BisNo ratings yet

- Petrofac CampDocument1 pagePetrofac CampRocky BisNo ratings yet

- House Keeping StoreDocument1 pageHouse Keeping StoreRocky BisNo ratings yet

- Unit III - Application of Theory of ProductionDocument16 pagesUnit III - Application of Theory of ProductionPushpavalli MohanNo ratings yet

- A Review of Production Planning and ControlDocument32 pagesA Review of Production Planning and ControlengshimaaNo ratings yet

- Level 1: New Century Mathematics (Second Edition) S3 Question Bank 3A Chapter 3 Percentages (II)Document27 pagesLevel 1: New Century Mathematics (Second Edition) S3 Question Bank 3A Chapter 3 Percentages (II)raydio 4No ratings yet

- Mergers and Acquisitions: Mcgraw-Hill/IrwinDocument23 pagesMergers and Acquisitions: Mcgraw-Hill/IrwinHossain BelalNo ratings yet

- A Quick Guide To The Program DPro PDFDocument32 pagesA Quick Guide To The Program DPro PDFstouraNo ratings yet

- Contemporary World GE 113 Module 1 PDFDocument19 pagesContemporary World GE 113 Module 1 PDFbojing mendezNo ratings yet

- Non-Bank Financial InstitutionsDocument11 pagesNon-Bank Financial InstitutionsCristineNo ratings yet

- NCA Rawalpindi-Fee StructureDocument1 pageNCA Rawalpindi-Fee StructureSyed Ali SajjadNo ratings yet

- Chapter No. 1: Micro EconomicsDocument6 pagesChapter No. 1: Micro EconomicsRamesh AgarwalNo ratings yet

- IFRS 1 Technical SummaryDocument2 pagesIFRS 1 Technical SummaryShashank GuptaNo ratings yet

- EPS significance and computationsDocument3 pagesEPS significance and computationsAccounterist ShinangNo ratings yet

- Idea To Launch (Stage Gate) Model: An Overview: by Scott J. EdgettDocument5 pagesIdea To Launch (Stage Gate) Model: An Overview: by Scott J. EdgettanassaleemNo ratings yet

- Capstone Research Paper - Ferrari 2015 Initial Public OfferingDocument9 pagesCapstone Research Paper - Ferrari 2015 Initial Public OfferingJames A. Whitten0% (1)

- Test Bank For Financial Reporting Financial Statement Analysis and Valuation 8th EditionDocument23 pagesTest Bank For Financial Reporting Financial Statement Analysis and Valuation 8th Editionbriansmithmwgrebcstd100% (25)

- SmeDocument68 pagesSmevictorNo ratings yet

- Session 2 - Deductions From Gross Income, Part 1Document10 pagesSession 2 - Deductions From Gross Income, Part 1ABBIE GRACE DELA CRUZNo ratings yet

- Module 1 Engineering EconomicsDocument34 pagesModule 1 Engineering EconomicsSINGIAN, Alcein D.No ratings yet

- Chapter 02 National Differences in Political EconomyDocument38 pagesChapter 02 National Differences in Political EconomyNiladri RaianNo ratings yet

- Amtrak Weighs Acela Financing OptionsDocument32 pagesAmtrak Weighs Acela Financing OptionsAngela Thornton67% (3)

- How communities changed before, during, and after the pandemicDocument3 pagesHow communities changed before, during, and after the pandemicMJ San PedroNo ratings yet

- Analyzing The Role of Public Relations in Building Social Corporate ImageDocument3 pagesAnalyzing The Role of Public Relations in Building Social Corporate ImageOneeba MalikNo ratings yet

- Session 2 - Determinants - of - Demand - For - The - Indian - Textile - IndustryDocument9 pagesSession 2 - Determinants - of - Demand - For - The - Indian - Textile - IndustryvvinaybhardwajNo ratings yet

- Shobha DevelopersDocument212 pagesShobha DevelopersJames TownsendNo ratings yet

- Corporate Social Responsibility &Document13 pagesCorporate Social Responsibility &Sumedh DipakeNo ratings yet

- Day 2 SBL Practice To PassDocument22 pagesDay 2 SBL Practice To PassRaqib MalikNo ratings yet

- Traphaco Reviews Distribution Restructuring and 2019 Business PlanDocument4 pagesTraphaco Reviews Distribution Restructuring and 2019 Business PlanHai YenNo ratings yet

- Corporate Social Responsibility MainDocument2 pagesCorporate Social Responsibility MainhagdincloobleNo ratings yet

- Acetic Acid (Europe) 2013-10-11Document2 pagesAcetic Acid (Europe) 2013-10-11Iván NavarroNo ratings yet

- PHILO - Extra Credit Paper - Jeepney StrikeDocument3 pagesPHILO - Extra Credit Paper - Jeepney StrikeFaith DytianNo ratings yet

- Managerial Economics in A Global Economy Ninth Edition: by Dominick SalvatoreDocument35 pagesManagerial Economics in A Global Economy Ninth Edition: by Dominick SalvatoreRAHUL SINGHNo ratings yet