You might also like

- Ch7 - Dealings in PropertyDocument16 pagesCh7 - Dealings in PropertyJuan Frivaldo100% (1)

- Black BookDocument77 pagesBlack BookKanya Nagure100% (2)

- Forensic Accounting Chapter 1-3Document32 pagesForensic Accounting Chapter 1-3victor wizvik100% (2)

- ESIC BenefitsDocument12 pagesESIC Benefitsraktim100No ratings yet

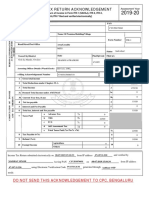

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruVikas MahorNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument101 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeNabilah FarahNo ratings yet

- Inpact of Taxation in Nigeria EconomyDocument34 pagesInpact of Taxation in Nigeria EconomyAjayi Oluwatobiloba TessyNo ratings yet

- Form16 Fiserv 2018-19Document8 pagesForm16 Fiserv 2018-19SiddharthNo ratings yet

- Impact of Treasury Single Account On The Liquidity: Clementina KanuDocument10 pagesImpact of Treasury Single Account On The Liquidity: Clementina KanuRamona GrantNo ratings yet

- Faith IJIFER-J-8-2020 1334Document10 pagesFaith IJIFER-J-8-2020 1334Ezekiel FavourNo ratings yet

- Treasury Single Account (Tsa) in Nigeria: A Theoretical PerspectiveDocument19 pagesTreasury Single Account (Tsa) in Nigeria: A Theoretical Perspectivechavala allen kadamsNo ratings yet

- % of Contribution SignatureDocument21 pages% of Contribution SignatureKehinde OjoNo ratings yet

- Ogbonna and Ojeaburu On Impact GIFMIS On Economic DevDocument20 pagesOgbonna and Ojeaburu On Impact GIFMIS On Economic DevAnonymous HcyEQ1Py100% (1)

- Effect of Treasury Single Account TSA On Selected Tertiary Institutions in NigeriaDocument5 pagesEffect of Treasury Single Account TSA On Selected Tertiary Institutions in NigeriaEditor IJTSRDNo ratings yet

- Effects of Financial Controls On FinanciDocument16 pagesEffects of Financial Controls On FinanciPromono AmortaNo ratings yet

- Treasury Single Account Concept, Design, and Implementation - AruwaDocument11 pagesTreasury Single Account Concept, Design, and Implementation - AruwaAdedapo AdegokeNo ratings yet

- Effects of Financial Management Reforms On Financial Corruption in Nigeria Public SectorDocument14 pagesEffects of Financial Management Reforms On Financial Corruption in Nigeria Public SectorEditor IJTSRDNo ratings yet

- Cash Management and Public Sector PerforDocument37 pagesCash Management and Public Sector Performutiariska100% (1)

- The Effect of International Public Sector Accounting Standard (IPSAS) Implementation and Public Financial Management in NigeriaDocument10 pagesThe Effect of International Public Sector Accounting Standard (IPSAS) Implementation and Public Financial Management in NigeriaaijbmNo ratings yet

- Before You Read The Chapter One of The Project Topic Below, Please Read The Information Below - Thank You!Document11 pagesBefore You Read The Chapter One of The Project Topic Below, Please Read The Information Below - Thank You!Adeola StephenNo ratings yet

- Treasury Single Account: A Viable Tool For Repositioning Government Ministries, Departments and Agencies (Mdas) For Sustainable Development in NigeriaDocument8 pagesTreasury Single Account: A Viable Tool For Repositioning Government Ministries, Departments and Agencies (Mdas) For Sustainable Development in NigeriaAhmedinNo ratings yet

- Analysis of The Relationship Between The New Treasury Single Account and Federal Government Ministries, Departments and Agencies' Performance in Northwest, NigeriaDocument10 pagesAnalysis of The Relationship Between The New Treasury Single Account and Federal Government Ministries, Departments and Agencies' Performance in Northwest, NigeriaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- The Role of Financial Control in The SocDocument18 pagesThe Role of Financial Control in The SocSUSAN PETER TERUNo ratings yet

- Audit Revenue and Public Expenditure in NigeriaDocument19 pagesAudit Revenue and Public Expenditure in NigeriaMoses UmohNo ratings yet

- 1 (1) Sani YusufDocument17 pages1 (1) Sani YusufSani Yusuf MohdNo ratings yet

- AIDC Submission To The Zondo Commission of InquiryDocument20 pagesAIDC Submission To The Zondo Commission of InquirySizweNo ratings yet

- Lwanda Jobs FundDocument3 pagesLwanda Jobs FundGeorge LwandaNo ratings yet

- International Journals of Academics & Research: (IJARKE Business & Management Journal)Document15 pagesInternational Journals of Academics & Research: (IJARKE Business & Management Journal)Abu DadiNo ratings yet

- International Journals of Academics & Research: (IJARKE Business & Management Journal)Document15 pagesInternational Journals of Academics & Research: (IJARKE Business & Management Journal)Abu DadiNo ratings yet

- Genzeb On PublicDocument15 pagesGenzeb On PublicAbu DadiNo ratings yet

- Accounting As A Basis For Managing Public Expenditure - ProjectDocument67 pagesAccounting As A Basis For Managing Public Expenditure - ProjectChidi EmmanuelNo ratings yet

- Project On Forensic AccountantsDocument65 pagesProject On Forensic AccountantsChidi EmmanuelNo ratings yet

- 25449-Strong Accountability Matters - EditedDocument6 pages25449-Strong Accountability Matters - Editedronald wafulaNo ratings yet

- The Auditor-General For Local Governments' and Accountability in Local Government Administration in Rivers State, 2007-2018Document8 pagesThe Auditor-General For Local Governments' and Accountability in Local Government Administration in Rivers State, 2007-2018abdulrazaq bibinuNo ratings yet

- 7th Annual International Academic Conference-2Document14 pages7th Annual International Academic Conference-2Mustapha AbdullahiNo ratings yet

- Financial InclusionDocument90 pagesFinancial InclusionRohan Mehra0% (1)

- Salamatu Chapter 1 3Document33 pagesSalamatu Chapter 1 3Ishmael FofanahNo ratings yet

- Chapter One 1.1 Background of The StudyDocument34 pagesChapter One 1.1 Background of The StudyChidi EmmanuelNo ratings yet

- Public Sector Accounting and Developing EconomiesDocument12 pagesPublic Sector Accounting and Developing EconomiesEze GodwinNo ratings yet

- Public Sector Accounting Aberration To Looting of Funds 1Document6 pagesPublic Sector Accounting Aberration To Looting of Funds 1James UgbesNo ratings yet

- Finance Development KwaneleDocument7 pagesFinance Development KwaneleLeeroy ButauNo ratings yet

- ProposalDocument23 pagesProposalPhumudzo NetshiavhaNo ratings yet

- Journal of Arts, Management, Science & Technology (JAMST)Document10 pagesJournal of Arts, Management, Science & Technology (JAMST)Akin DolapoNo ratings yet

- Pub Ad Seminar PaperDocument10 pagesPub Ad Seminar PaperKYLE CULLANTESNo ratings yet

- Catada PM231 FinalexamDocument4 pagesCatada PM231 FinalexamAldwinNo ratings yet

- Impact of Budgetary Control Usage On ManDocument23 pagesImpact of Budgetary Control Usage On Manarianne LorqueNo ratings yet

- Account Research 2Document46 pagesAccount Research 2Michael MololuwaNo ratings yet

- Assesment of Impact of Taxation On Revenue Generation in Local GovernmentDocument72 pagesAssesment of Impact of Taxation On Revenue Generation in Local GovernmentAFOLABI AZEEZ OLUWASEGUNNo ratings yet

- Tax 4 5Document43 pagesTax 4 5MubeenNo ratings yet

- Tax 4 5Document43 pagesTax 4 5MubeenNo ratings yet

- Forensic Accounting and Fraud ManagementDocument64 pagesForensic Accounting and Fraud ManagementProgress OmeruNo ratings yet

- 1.2 Statement of The ProblemDocument19 pages1.2 Statement of The ProblemJohnson JohnNo ratings yet

- Topic 10 PsaDocument63 pagesTopic 10 PsaOctavius MuyungiNo ratings yet

- International Public Sector Accounting Standards and Financial Reporting in Nigeria: Answers To Implementation QuestionsDocument5 pagesInternational Public Sector Accounting Standards and Financial Reporting in Nigeria: Answers To Implementation QuestionsIOSRjournalNo ratings yet

- Accounting Regulatory Frameworks and Public Institutions' Compliance in NigeriaDocument10 pagesAccounting Regulatory Frameworks and Public Institutions' Compliance in NigeriaNwogboji EmmanuelNo ratings yet

- Principles and Importance of Taxation To The Nigerians EconomyDocument11 pagesPrinciples and Importance of Taxation To The Nigerians Economyfatima aliNo ratings yet

- APSAF TERM PAPER CompleteDocument15 pagesAPSAF TERM PAPER CompleteOyeleye TofunmiNo ratings yet

- 6 Full TextDocument22 pages6 Full TextnigeNo ratings yet

- Peran Akuntansi Dalam Meningkatkan Kesadaran Permasalahan Keuangan Negara Indonesia (Autorecovered)Document7 pagesPeran Akuntansi Dalam Meningkatkan Kesadaran Permasalahan Keuangan Negara Indonesia (Autorecovered)dewaedison0No ratings yet

- Enspecial Series On Covid19budget Execution Controls To Mitigate Corruption Risk in Pandemic SpendinDocument9 pagesEnspecial Series On Covid19budget Execution Controls To Mitigate Corruption Risk in Pandemic SpendinamitanshuNo ratings yet

- Financial Inclusion & RiskDocument26 pagesFinancial Inclusion & Riskanoog aliNo ratings yet

- Proposal of Deposit MobilizationDocument37 pagesProposal of Deposit MobilizationBereket RegassaNo ratings yet

- ተመሰገን (1)Document18 pagesተመሰገን (1)yusuf kesoNo ratings yet

- Impact of Tax Policies On Small and Medium-Sized Enterprises (Smes) in Nigeria (A Case Study of Smes in Gwagwalada, Fct-Abuja)Document15 pagesImpact of Tax Policies On Small and Medium-Sized Enterprises (Smes) in Nigeria (A Case Study of Smes in Gwagwalada, Fct-Abuja)Osilama Vincent OmosimuaNo ratings yet

- 2.Ijbgm-A Cointegration Analysis of The Relationship Between Money Supply and Financial Inclusion in Nigeria - 1981-2016 - RewrittenDocument14 pages2.Ijbgm-A Cointegration Analysis of The Relationship Between Money Supply and Financial Inclusion in Nigeria - 1981-2016 - Rewritteniaset123No ratings yet

- EIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptFrom EverandEIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptNo ratings yet

- BIR - Remittance of CWT (Form 1606) Should Be in The Name of The Buyer - JUAN PATAG REAL ESTATEDocument2 pagesBIR - Remittance of CWT (Form 1606) Should Be in The Name of The Buyer - JUAN PATAG REAL ESTATERoy RitagaNo ratings yet

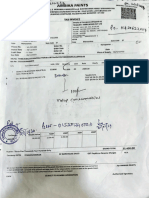

- Ambika Paint GRN CorrectionDocument1 pageAmbika Paint GRN Correctiontanmaychoudhari6767No ratings yet

- Factura - FV - 2024 - 0650Document2 pagesFactura - FV - 2024 - 0650cristina.perezNo ratings yet

- TaxDocument4 pagesTaxCielito AlvarezNo ratings yet

- Monthly Remittance Return of Creditable Income Taxes Withheld (Expanded)Document2 pagesMonthly Remittance Return of Creditable Income Taxes Withheld (Expanded)Games NathanNo ratings yet

- UntitledDocument21 pagesUntitleddhirajpironNo ratings yet

- Lab2 1Document3 pagesLab2 1Quân TrầnNo ratings yet

- Introduction To Income TaxDocument80 pagesIntroduction To Income Taxkana lahotiNo ratings yet

- Invoice For Portable Toilets - Nuggets ParadeDocument1 pageInvoice For Portable Toilets - Nuggets Parade9newsNo ratings yet

- Personal Monthly BudgetDocument1 pagePersonal Monthly BudgetmanojNo ratings yet

- Income Tax - Chap 06Document2 pagesIncome Tax - Chap 06ZainioNo ratings yet

- Group 2 - Subgroup 3Document16 pagesGroup 2 - Subgroup 3Maricel RaguindinNo ratings yet

- Aspiration - Link Clsisnew PrintGst - JSP Rid NRHSOfGX XRRRVDKDV CRg3DDocument1 pageAspiration - Link Clsisnew PrintGst - JSP Rid NRHSOfGX XRRRVDKDV CRg3DSwetha IyerNo ratings yet

- FabHotels Invoice WVHGJCDocument1 pageFabHotels Invoice WVHGJCSimran MehrotraNo ratings yet

- Lease Rent Satguru 01.01.23-31.12.23Document1 pageLease Rent Satguru 01.01.23-31.12.23sourabh nawaniNo ratings yet

- LHDocument4 pagesLHAbhinay SinhaNo ratings yet

- Tax and Regulatory: Epc Contracts - Fiscal ScenarioDocument30 pagesTax and Regulatory: Epc Contracts - Fiscal Scenariopranjal92pandeyNo ratings yet

- Invoice Sai Durga Traders Ct281 OriginalDocument1 pageInvoice Sai Durga Traders Ct281 Originalmadhav dNo ratings yet

- Exercise 2-Chapter 3-Intro To Business TaxationDocument3 pagesExercise 2-Chapter 3-Intro To Business TaxationQuenie De la CruzNo ratings yet

- 05 Activity 1 BALADocument3 pages05 Activity 1 BALAPola PolzNo ratings yet

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 pageBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountRahul Giri (Logistics)No ratings yet

- 20210213231717D4402 - FINC 7007-Week 1-AssignmentDocument3 pages20210213231717D4402 - FINC 7007-Week 1-AssignmentSugata SNo ratings yet

- Specialty Packages To Super Bowl XLVDocument4 pagesSpecialty Packages To Super Bowl XLVsblaskovichNo ratings yet

- Position Paper Tax PartDocument3 pagesPosition Paper Tax PartHahns Anthony GenatoNo ratings yet